Recent Search

Popular Searches

Fed Chair Jerome Powell again laid out his case for more fiscal support in his testimony to Congress overnight, repeating that support from “all levels of government” was needed to help the US get back to pre-pandemic levels of activity. Treasury Secretary Steve Mnuchin told Congress that the administration and both parties were working to get another fiscal support package passed but given the political divisions in the country at the moment we see little chance of a significant deal being reached before the presidential election in November.

Japan was the first major economy to report PMI figures this week and they came in disappointing. Manufacturing data for September showed the PMI at 47.3, barely rising from the 47.2 a month earlier and remaining in contraction territory. Factory operators were at least reporting to be more optimistic and may give new Prime Minister Yoshihide Suga time to introduce expansionary policies to get Japan’s economy growing again. Services data also remains in contraction at 45.6 for September compared with 45 a month earlier.

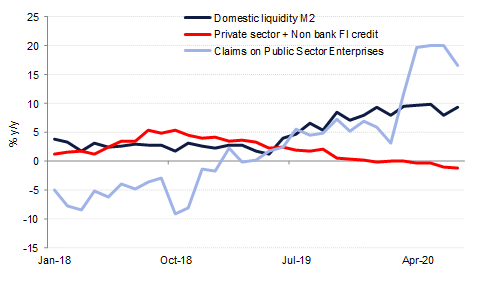

UAE broad money supply (M2) grew 2.3% m/m and 9.4% y/y in July from 7.9% y/y in June on the back of faster growth of currency in circulation and FX deposits. Credit to both public and private sectors contracted m/m in July, although public sector credit growth was still up 16.6% y/y. Private sector credit declined -1.2% y/y, the fourth consecutive month of contraction. Bank deposits grew 1.1% m/m and 6.2% y/y, while gross lending by banks slowed to 5.6% y/y in July from 5.8% y/y in May and June.

Bank al Maghrib, Morocco’s central bank, kept policy rates unchanged at 1.5% at its latest meeting, noting an uptick in inflation in August to its highest level since 2011 at 1.4% m/m. The central bank also lowered their projections for economic activity this year, expecting a contraction of 6.3% in 2020 compared with 5.2% previously.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Treasury markets showed little reaction either to testimony from Fed Chair Jerome Powell or Steve Mnuchin as their views were largely expected by the market. Chicago Fed president seemed to give a more hawkish view, saying that the Fed’s new inflation targeting strategy means they could raise rates before hitting their average inflation target. Evans is not a voting member on the FOMC but his commentary does highlight some of the vagueness surrounding the Fed’s new policy and led to some dissents in their vote on rates last week.

Moody’s cuts its sovereign rating on Kuwait to ‘A1’ and revised its outlook to stable. The agency noted liquidity risks and a “weaker assessment” of institutions and governance. Kuwait’s government has warned of payment risks to public sector workers as the country grabbles with a sizeable fiscal deficit this year and has been hampered in efforts to raise funds in debt markets.

Oman has mandated several banks for a new Eurobond issue that could hit markets soon. Oman had secured a USD 2bn bridging loan earlier in the summer which it will use the funds raised from a bond issuance. Press reports also indicated Morocco would be seeking to tap markets for around USD 2bn in a Eurobond issuance, potentially by the end of the month.

The USD's rally continued on Tuesday and early this morning. The DXY index advanced by 0.35% overnight and has pushed above 94 this morning, its highest level in over a month and exceeding the 50-day moving average of 93.445. Similarly USDJPY is pushing higher, moving back above 105 this morning.

The EUR extended its slump, dropping by -0.54% to trade overnight and is pushing to 1.1682 today, marking a break below the one-year Fibonacci retracement of 1.1687. GBP experienced heavy losses as well, declining by -0.66% and is now just below both the 100-day (1.2726) and 200-day moving averages (1.2724). The AUD fell by -0.73% overnight and is extending its losses today while the NZD has pushed to 0.6622. Both antipodean currencies have fallen below their respective 50-day moving averages of 0.7202 and 0.6641.

Equity markets enjoyed some respite from the selling pressure seen at the start of the week yesterday, with the bulk of major indices closing up – although for the most part they didn’t stage a significant enough recovery to recoup the losses seen on Monday. France’s CAC was the notable outlier, falling 0.4% on the day, while in the rest of Europe, the DAX and the FTSE 100 managed modest gains of 0.4% each. That being said, concerns over renewed lockdowns in Europe amidst rising coronavirus cases remain to the fore, and it was pound sterling falling back to levels last seen in July that largely boosted the index, with multinational firms being amongst the bigger risers.

In the US, the NASDAQ was the biggest rise again, climbing 1.7% compared to the Dow’s 0.5% and the S&P 500’s 1.1%. This is something of a turnaround from the previous two weeks, as those tech assets which had begun to look somewhat expensive have become something of a haven as concerns over a renewed lockdown mounts.

Oil prices are wavering with no specific fundamentals to push them firmly one way or the other. Both Brent and WTI closed higher overnight (by around 0.7% each) but are both losing ground in early trade this morning. The resurgence of Covid-19 cases in Europe is weighing on demand expectations, particularly as there is still visible uncertainty as to how governments will respond and how effective those responses will be.

Edward Bell

Edward Bell