Recent Search

Popular Searches

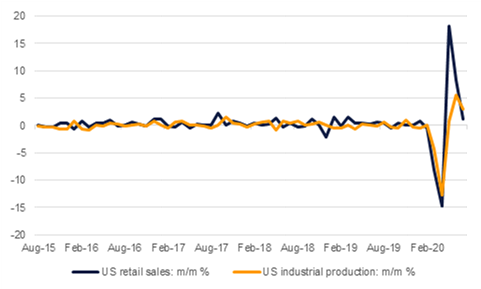

Political divisions in the US are hardening in the run-up to November’s presidential election as the Democratic Party is blaming the Trump administration for actively disrupting the US postal service, ahead of when many voters in the US would likely make use of mail-in ballots given concerns over Covid-19. The widening political gulf in the US will make it all the more challenging for Republicans and Democrats to agree on new round of fiscal stimulus, threatening the recovery underway in the economy and the turnaround in financial markets, particularly treasury markets. US data for July affirmed that the recovery is still underway but is now on a more muted pace. Retail sales were up by 1.2% m/m in July, after an 8.4% gain in June, while industrial output rose by 3% compared with 5.7% a month earlier. Industrial output is still below its pre-coronavirus levels with the mining sector (which includes oil and gas activity) well below pre-pandemic activity.

China’s economy continues its path to recovery although it is largely being helped along by industry. Industrial output was up by 4.8% y/y in July, affirming an improving trend since March. However, retail sales still remain down in annual terms: for July, retail sales were down by 1.1%, better than the results of the last five months but nevertheless highlighting that China too still has a long way to go to return to pre-coronavirus levels of activity. Beyond the recovery from the pandemic China’s economy will still remain at risk of aggressive trade policies from the US. President Trump ordered the Chinese company that owns TikTok, a popular social media app, to sell their US assets in the latest salvo in the trade war. Chinese and US officials postponed a review of the current Phase 1 trade deal that was meant to take place over the weekend.

Inflation in Saudi Arabia spiked to 6.1% y/y in July, compared with just 0.5% a month earlier. July represents the first month when new higher levels of VAT took effect—Saudi Arabia raised its VAT rate to 15% from 5% from July 1st—so the sharp move higher in prices reflects the bump in VAT. Firms in the Kingdom have been keeping output costs low to try and encourage some consumption at a time when demand is low but company profitability will be hit if they choose to absorb more of the higher costs on an ongoing basis.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

US treausries sold off last week as the market eagerly watches for signs that a new fiscal stimulus plan could be reached and economic data confirms that the recovery in the economy is underway, if at a more subdued pace. While yields across the curve moved higher, most of the gains were concentrated in the back end. Yields on 2yr USTs added a bit less than 2bps last week to settle just shy of 0.13% while 10yr yields added almost 15bps over the week to close at 0.7094%, having hit 0.72% mid week. Whether the sustained sell-off can persist as political disputes rage in the US remains to be seen.

The sell-off wasn’t limited to US assets as European bond markets also closed lower last week. Yields on 10yr gilts closed at 0.24%, having hit less than 0.1% in early August while 10yr bund yields moved up to -0.42%, their highest level since mid July.

Emerging market USD bonds finally put the brakes on their continuous rally from late April, declining by 0.4% last week. Spreads over treasuries, however, did manage to compress further, moving to 355bps last week. That represents their narrowest level since mid-February.

Fitch cut Bahrain’s sovereign rating to ‘B+’, saying the country would require additional assistance from other GCC nations. Fitch placed the rating on a stable outlook and estimated that Bahrain’s debt/GDP ratio would rise to 130% in 2020 and decline only marginally over the next few years. Yields on Bahrain 2024 bond closed last week at 3.9% as the market absorbed the downgrade by Ftich.

The dollar recorded modest losses last week. The DXY index closed at 93.096 on Friday even as UST yields moved sharply higher. This marks a weekly decrease of -0.36%. USDJPY advanced by 0.64% for the week and settled at 106.60. The pairing briefly breached the 107 handle but failed to hold onto these gains. The 50-day moving average (106.79) is within touching distance and will be the next major indicator to look out for.

The euro closed at 1.1842 on Friday, an increase of 0.47% w/w after the dollar faltered in the later portion of the week. This comes in spite of the Eurozone reporting its steepest drop in employment on record in the second quarter. Sterling experienced some choppy movement as new quarantine restrictions were imposed in the UK for travelers coming from France, Malta and the Netherlands. The currency settled at 1.3085. A golden cross is a nigh-on certainty for the pound, with the 50-day moving average (1.2705) sitting just below the 200-day moving average (1.2715). The AUD earned modest gains to close at 0.7171 whilst the NZD fell by -0.96% to settle at 0.6542.

Last week was a positive one almost across the board for major equity indices, with stocks closing lower in very few markets barring India and Brazil. The S&P 500 was one of the other underperformers of the week, adding only 0.6% over the period, and failing to close above the all-time high of 3,386 it hit in pre-lockdown February. Nevertheless, at 3,372 it is now up 4.4% ytd, and a positive resolution of the fiscal support impasse could serve to nudge it back to record levels.

In Europe, stocks managed to close higher over the period despite a poor performance at the week’s close as the markets were roiled by renewed restrictions on travel. The FTSE 100, the CAC and the DAX closed up 1.0%, 1.5% and 1.8% w/w respectively, despite losses of 1.6%, 1.6% and 0.7% on Friday.

Within the region, the DFM and the Tadawul gained 4.0% and 2.7% w/w, with the DFM in particular bolstered by a strong close to the week, gaining 1.1% on Friday.

Brent futures rallied 0.9% in a choppy week for oil markets. Assessmetns from OPEC and the IEA cast a downbeat tone to the near-term outlook for demand as countries grapple with resurgences of Covid-19 cases. WTI managed to outperform, gaining 1.9% last week.

Gold prices recorded their first weekly decline since June last week, closing down 4.44% at USD 1,945/troy oz. Gold will move in reflection to USTs in the short-run with political dispute on the election and fiscal support likely front of mind for markets.

Edward Bell

Edward Bell