Recent Search

Popular Searches

FOMC minutes of the Fed’s September meeting said policymaker’s debate around long run inflationary pressures intensified. Participants reflected concerns that the low inflation readings this year might reflect more persistent trends and that patience in removing policy accommodation while assessing trends in inflation was warranted. However, many still felt that another rate increase this year "was likely to be warranted". Furthermore several fed officials noted inflation readings over the next few months would likely be complicated by a temporary increase in energy costs and prices of other items due to the impacts of hurricanes and storms.

Japan’s core machinery orders rose 3.4% m/m in August against a 1.1% rise in July, signalling an improvement in capital investments. The value of core orders was the highest since July 2016, at 882.4 billion yen. Core machinery orders, is a highly volatile data series which excludes ships and utilities' electrical power equipment, is regarded as an indicator of capital spending in the coming six to nine months. The positive figures come ahead of general elections this month, where Prime Minister Shinzo Abe plans to convince voters his “Abenomics” policies are driving a sustainable recovery.

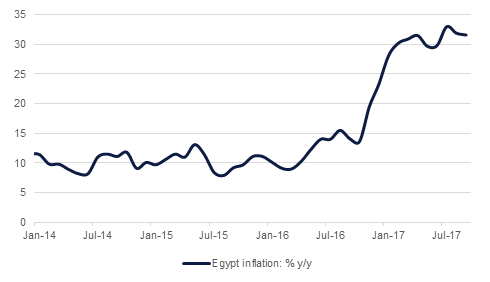

Egypt’s inflation dipped from 31.9% in August to 31.6% in September, as the impact of fuel and energy price hikes fade, largely due to being absorbed earlier in the year. The figures released by the Central Bank of Egypt on Tuesday also showed core inflation, which strips out volatile items like food, decreased to 33.26% from 34.86%. Inflation in Egypt is running at its highest level since 1986, as the government cut energy and fuels subsidies, as a condition of a $12 billion, three-year loan programme agreed with the IMF last November. Having raised its key interest rates by 200 basis points in July, seeking to ease the inflationary pressures, the Central Bank recently raised banks' reserve requirements, signalling a rate cut may come soon.

Source: Bloomberg, Emirates NBD Research

US Treasuries held onto their gains as minutes from the last Federal Reserve meeting showed that officials debated over the transitory nature of the current low inflation. Additionally reports that Treasury Secretary Mnuchin is pushing Jerome Powell, considered dovish, for the Fed Chair also helped the gains in Treasuries. The yield on the 2y USTs and 5y USTs remained flat at 1.51% and 1.95% respectively while it dropped 2 bps on the 10y USTs to 2.34%.

Regional bond markets continued to trade in a tight range with yield on the Bloomberg Barclays GCC Credit and High Yield index remaining flat at 3.54% and so did credit spreads at 154 bps.

In terms of rating action. Fitch affirmed Etihad Airways rating at A with stable outlook.

On the primary market front, ADCB is expected to issue a benchmark AUD denominated bond sometime later this week.

The dollar weakened against all peers as the FOMC minutes released overnight showed that inflation was still a concern for some Fed officials. The DXY index is trading at its lowest level this month after yesterday’s drop. EUR and GBP were among the best gainers against the greenback; despite the uncertainty over Catalonia’s referendum, economic data out of Germany continues to beat expectations.

Developed market equities closed higher as minutes of the Federal Reserve meeting showed no major surprises. The S&P 500 index added +0.2% while the Euro Stoxx 600 index closed flat.

Regionally, it was all about Saudi equities. The Tadawul closed lower for a fifth consecutive trading session to lose -2.2% and close below the 7,000 level. It has also broken through the key technical levels of 100d and 200d moving average.

Elsewhere, DIB added +0.7% after the bank reported Q3 2017 net profit of AED 1.11bn (+27.5% y/y), beating analysts’ estimates of AED 1.04bn by 6.7%.

Oil prices nudged higher yesterday as OPEC revised up its forecast for demand in 2018. The bloc expects global markets will need 230k b/d more of its oil in 2018 compared with a previous forecast as OPEC cuts its forecast for growth from other suppliers. Overall demand growth will be 1.38m b/d in 2018, an upward revision but still set to be slower than in 2017. WTI future settled up 0.75% and Brent nearly 0.6% to close the day.

Private sector assessment of US crude balances reported a build of 3m bbl last week and an improvement in refinery runs. Official EIA data will be released tonight, delayed by one day owing to a public holiday in the US at the start of the week.