Recent Search

Popular Searches

UAE

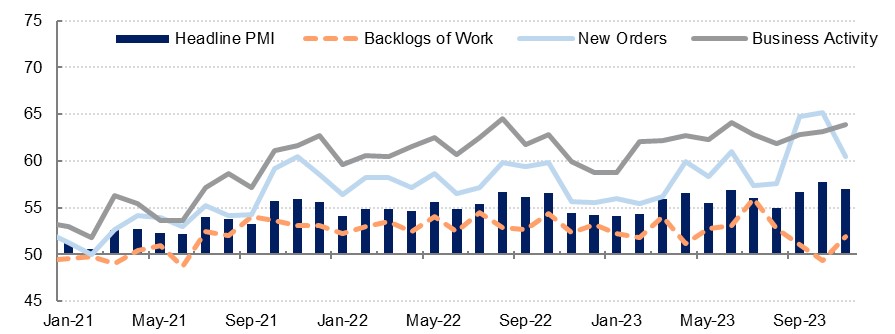

The S&P Global PMI survey for the UAE stood at 57.0 in November, down from the multi-year high of 57.7 logged in October but still indicating a robust expansion in the non-oil private sector. Output accelerated at the fastest pace in five months as fewer than 1% of responding firms noted a decline in activity. While new orders growth slowed compared to the previous month it was still representative of a robust pipeline of ongoing new work. New export orders slowed sharply from October to a four-month low, however, suggesting that the bulk of the new orders remain domestic-led, with firms noting that marketing efforts helped drive the sales.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

In this environment of strong demand and new work growth, firms ramped up their buying and the quantity of purchases measure rose to a multi-year high. Inventories also rose sharply as a result, with the stocks of purchases at the highest level since January 2018. However, despite this positive buying action, firms are less optimistic with regards future output than they had been in recent months. The broad outlook remains positive, but firms are wary of increasing competition in the market.

Looking at prices, input costs rose at a slower pace in November compared with the 15-month high seen in October. Purchase costs were rising more slowly but higher raw materials prices continued to feed through to firms’ budgets. Staff costs also rose, albeit marginally, as firms were forced to pay more in order to retain talent. Despite ongoing input price rises, firms continue to absorb these costs and output prices turned negative again in November after rising marginally the previous month for the first time in a year and a half.

Saudi Arabia

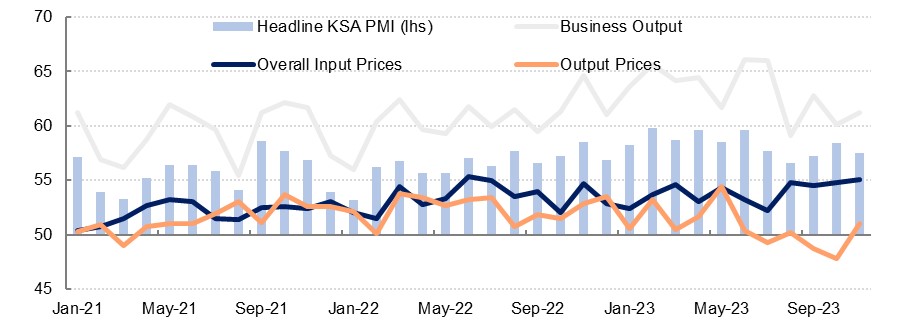

The Riyad Bank PMI survey for Saudi Arabia slipped slightly in November as the headline reading fell to 57.5, from 58.4 the previous month. Nevertheless, this remains a strongly expansionary reading, and the index remains well above the neutral 50.0 level as it has done all year, indicative of robust growth in the non-oil private sector. Business activity and new orders were both still at elevated levels and came in higher than the previous month. What dragged the headline figure down was a slower pace of growth in hiring and inventory growth, alongside a marked reduction in delivery times. The slowdown in the employment subcomponent was from the nine-year high recorded in October, however, and firms continue to expand their workforces at a higher-than-average pace.

Source: Riyad Bank, Emirates NBD Research

Source: Riyad Bank, Emirates NBD Research

Input prices rose at the fastest pace since mid-2022 in November, coming in well above the long-run average. This was driven by higher purchase costs which accelerated in November on the back of higher raw material prices for the construction sector in particular. Staff costs rose at a slower pace in November than October’s seven-year high but are still rising at a faster pace than usual.

Egypt

The S&P Global PMI survey for Egypt rose to 48.4 in November, from 47.9 in December, but remains in sub-50.0 contractionary territory. Both output and new orders contracted at a slower pace in November but issues around the high cost of raw materials, weak demand, and ongoing currency issues all dampened activity still. Meanwhile, new export orders contracted more quickly in November as compared with October.

Price pressures remain to the fore in Egypt even as headline annual CPI inflation slowed marginally to 35.8% in October, and this was apparent in the PMI survey’s subcomponents. The purchase costs subcomponent of the PMI survey accelerated once more in November with both purchase costs and staff costs heading higher. In this environment, firms continued to raise their output prices which increased at the fastest pace since March.

With ongoing uncertainty around Egypt’s economic reform programme, and persistent external economic pressures, business optimism fell once more in November, dropping to a new record low for the series. According to the survey, only a small number of respondents held a positive outlook on the next 12 months, with inflation the primary reason for pessimism. IMF chief Kristalina Georgieva has said recently that tackling inflation should be the priority for Egypt at present rather than FX regime adjustment, raising speculation that an IMF deal that releases some of the scheduled funds for Egypt could be reached even without any near-term move in the exchange rate.

Daniel Richards

Daniel Richards