Recent Search

Popular Searches

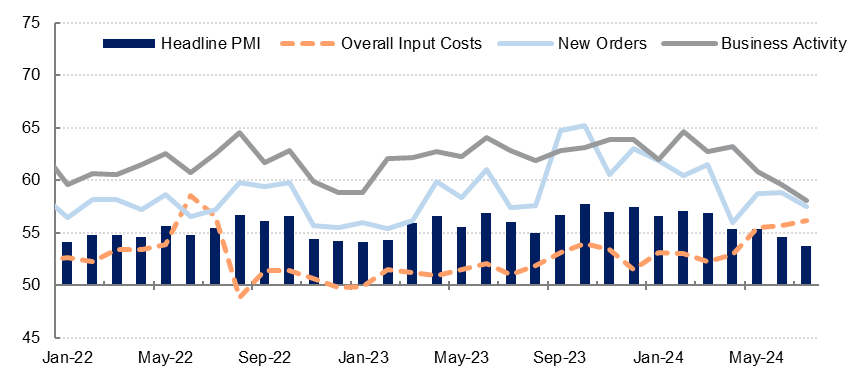

The S&P Global PMI for the UAE fell to 53.7 in July from 54.6 in June and was the lowest reading since September 2021. While business activity and new orders increased sharply last month, both rose at a slower pace than in recent months. Price pressures continue to build with input costs rising at the fastest pace in a year. Firms raised their selling prices for the third consecutive month as they sought to partially offset higher input costs but margins remain under pressure.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

The backlogs of work continued to rise in July even as supplier delivery times improved. Despite the rising backlogs of work, firms increased hiring only modestly last month with the employment sub-index slipping to a six-month low of 51.2.

Overall, the UAE PMI data suggests that the pace of non-oil sector growth continues to moderate as we expected this year. We retain our forecast of 5.0% non-oil growth in the UAE in 2024, down from 6.2% in 2023.

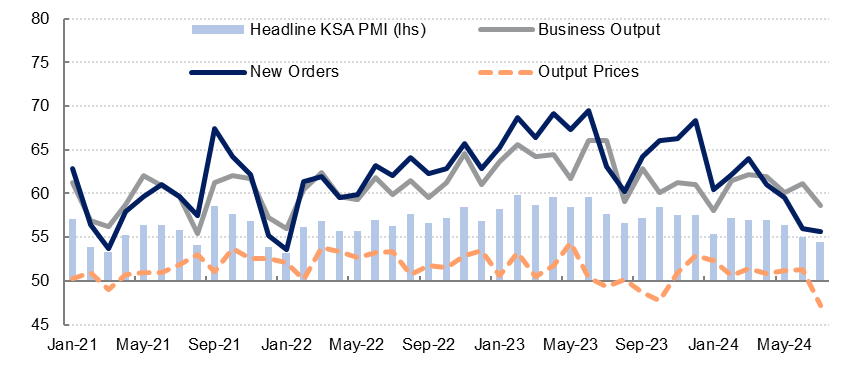

The Riyad Bank Saudi Arabia PMI fell to 54.4 in July from 55.0 in June and was the lowest reading since January 2022. Both business activity and new orders increased at a slower pace in July, with new export orders slowing sharply. Firms added to headcount last month but employment growth was the softest in three months.

Price pressures remain contained in the kingdom with overall input costs rising at a slower pace last month. Firms reduced selling prices at the fastest rate on record as they sought to maintain market share in a competitive environment.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

The S&P Global PMI for Egypt slipped to 49.7 in July from 49.9 in June with business activity and new work slightly weaker than the previous month. New export orders remained the bright spot in the survey, with the sub-index at 54.3 in July indicating solid new export order growth. Backlogs of work declined slightly as firms increased headcount last month.

Input costs rose at a faster pace in July as purchase costs increased, but the rate of price growth was modest relative to the last couple of years. Firms passed on some of these higher costs to buyers with output prices rising at the fastest pace since March. Price increases were led by the manufacturing sector.