Recent Search

Popular Searches

UAE

The S&P Global PMI survey for the UAE fell to 56.6 in January, down from 57.4 the previous month. This marked a five-month low for the headline index, although it remains a strongly expansionary reading for the non-oil private sector. Output was also at a five-month low, but over a fifth of firms still saw an expansion in activity, with government projects cited as one driver of growth. The pipeline for the coming months remains positive as new orders growth was strong even as it slowed slightly from the December level. The domestic market continues to drive new order growth as new export orders expanded at a far slower pace with only a marginal expansion for the second month running.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

Firms continued to hire, but at a slower pace than seen over the preceding year and there was only a marginal expansion in staffing levels. This may have contributed to the sharpest rise in backlogs of work for five months. On the price front, input prices rose at a much sharper pace in January than was the case in December, with higher purchase costs driving the increase. Respondents to the survey noted higher costs for raw materials and also observed that shipping costs and supply chain issues had increased due to disruptions in the Red Sea. Staff costs rose at a more modest pace, with salary revisions driving what increases there were. Despite the higher cost pressures, firms continued to offer discounts in order to remain competitive, with output prices falling at the fastest pace since May 2023.

Business optimism remained robust, but slipped from December’s level, with 18% of firms expecting output to be higher in 12 months’ time compared with only 1% expecting a decline. We forecast non-oil growth of 4.5% in the UAE this year.

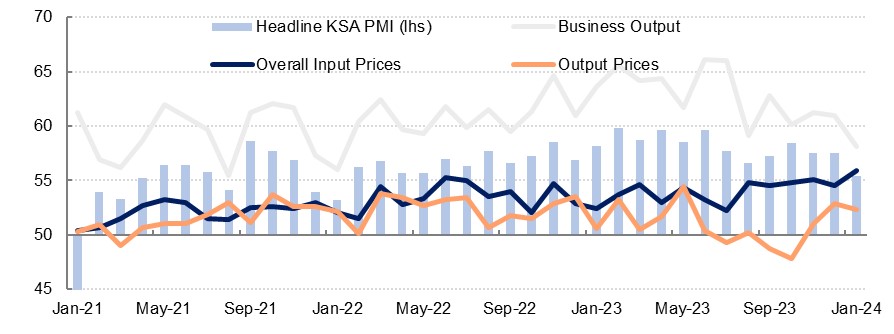

Saudi Arabia

There was also a slowdown in Saudi Arabia’s non-oil private sector at the start of the year as the Riyad Bank PMI survey fell to a two-year low, dropping to 55.4, from 57.5 the previous month. This is still indicative of strong growth, and output continued to expand quickly, but this was also at the slowest pace since January 2021. Firms noted ongoing projects and a rise in tourism as helping to boost activity. However, there was a sharp drop in new orders compared with the previous month with firms noting increased competition in particular as having weighed on growth. As with the UAE, it is domestic orders that are driving the expansion and in Saudi Arabia, as new export orders contracted in January.

Source: S&P Global, Emirates NBD Research

Price pressures were more acute in January as input prices rose at the fastest pace since August 2020. The bulk of this was driven by higher purchases costs which rose at the fastest pace recorded by the survey since 2012, and firms noted that transport costs contributed to this. Staff costs also accelerated on the previous month though and while this was at a less acute pace than purchase costs, it was still at the fastest pace since 2014. Cost of living pressures have forced businesses to increase salaries. In contrast to the UAE, firms in Saudi Arabia continue to pass on these higher prices to customers despite frequent reference to increasing competition and output prices rose for the third month in a row.

Egypt

Egypt’s ongoing economic issues continue to weigh on the country’s S&P Global PMI survey, with the headline reading falling to 48.1 in January, from 48.5 in December. While intensified discussions over the past week suggest that a new IMF deal is imminent, in January an ongoing shortage of dollars and heightened regional tensions weighed on output, with respondents to the survey highlighting a fall in tourism activity. The outlook for the coming months remains weak, with new orders contracting at the fastest pace since May 2023 and 15% of businesses seeing a decline. This was driven largely by domestic orders, with new export orders declining by only a marginal amount.

Price pressures remained to the fore as businesses struggled with a shortage of dollars through official channels and a declining parallel market rate, and 30% of businesses saw higher purchase prices compared with December. The higher cost of living forced some businesses to raise salaries, which contributed to higher staff costs also, although this rose at a far softer pace than purchase costs. Firms are passing these costs on to consumers, with output prices rising at the fastest pace since last January. This will keep pressure on CPI inflation, which has been falling on the annual measure but the CBE noted ongoing pressures on a monthly basis as it hiked the overnight deposit rate by 200bps last week.

Daniel Richards

Daniel Richards