Recent Search

Popular Searches

UAE

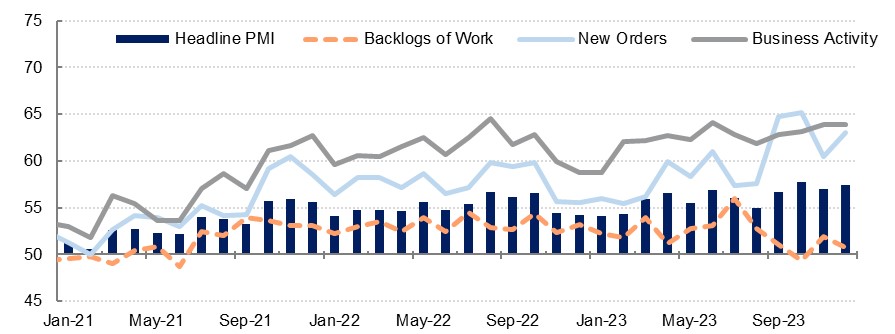

The S&P Global PMI survey for the UAE rose to 57.4 in December, up from 57.0 the previous month. This makes the average for the year 56.1, well above the neutral 50.0 level that delineates contraction and expansion in the non-oil private sector economy, and far stronger than the global trend where many major economies struggled with weak or contractionary PMI readings throughout 2023. The year ended with a higher average for Q4 than was seen in the third quarter, with the survey supporting our estimate of robust non-oil GDP growth of 5.0% in 2023.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

Looking at the December survey, growth in output was unchanged from the five-month high recorded in November, with over a quarter of respondents noting an increase in activity while only 1% saw a decline. The coming months also appear to have a healthy pipeline of new work as new orders growth accelerated in December with promotional offers helping to drive increased sales. These orders were driven primarily by domestic demand, as new export order momentum slowed sharply in November and December from Q3.

Price pressures eased in the UAE in the final month of the year, with purchase prices rising at the softest pace since July. A slowdown in purchase price rises was the key factor in this and the majority of respondents found no change in their prices paid, helped by a moderation in raw materials prices. Staff costs ticked up at broadly the same marginal level as seen in November, with firms noting that they needed to raise salaries in order to keep hold of experienced staff in a tight labour market. Despite higher input prices, firms continued to discount in order to remain competitive, with output prices falling at the fastest pace since July.

UAE businesses remain confident for the coming year, with business optimism picking up in December to the third-highest level since early 2020, just as the Covid-19 pandemic began. Just over a fifth of businesses anticipate increased business in 12 months’ time and firms increased their hiring at a faster rate in December, citing expansion efforts. We forecast non-oil GDP growth in the UAE of 4.5% in 2024.

Saudi Arabia

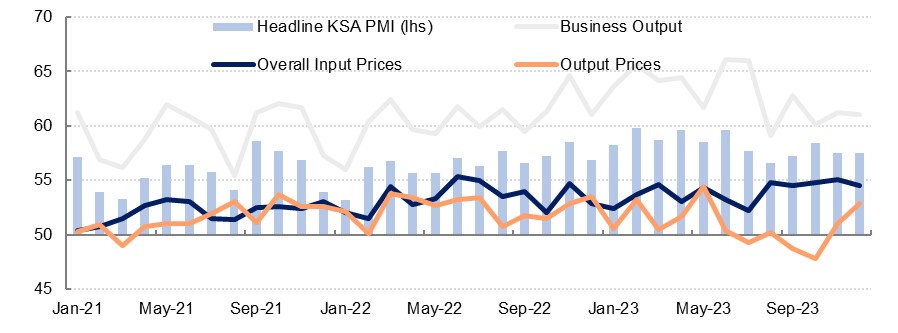

The Riyad Bank PMI survey for Saudi Arabia was unchanged at 57.5 in December, resulting in a strong end to the year and a higher average for Q4 than seen in Q3. The average over the year as a whole was 58.3, well above the neutral 50.0 level and underscoring our estimate of a robust 4.0% expansion in non-oil GDP in 2023. Output grew at a slightly softer pace in December as compared with average over the year but it remained strong and respondents mentioned improved demand conditions.

Source: Riyad Bank, Emirates NBD Research

Source: Riyad Bank, Emirates NBD Research

Looking ahead, with new orders expanding at one of the fastest paces in nine years of the survey as they accelerated for the fourth month running in December, we maintain our expectation that 2024 will be another year of healthy growth in the non-oil private sector. The strongest gains in new orders came from the manufacturing sector and domestic orders continue to drive growth; new export orders expanded in December but at a much softer pace than total orders, and this was only the second 50-plus expansionary reading since August.

Businesses remained optimistic with regards the year to come in this strong order environment, although this confidence did soften from the multi-month high recorded in November. Employment continued to expand, albeit at the slowest pace since July.

Input price inflation softened modestly in December, with purchase costs rising at a slower pace than in November. Raw materials costs were pushed higher by global inflationary pressures. By contrast, staff costs accelerated in December as firms had to raise salaries in order to compensate for the rising cost of living, and to keep hold of experienced workers. Businesses passed some of these price rises on to their customers, with output prices rising for the second month running in December after two months of declines prior to that.

Egypt

The S&P Global PMI survey for Egypt rose marginally for the final reading of the year, picking up to 48.5, from 48.4 in November. The survey remained in contractionary sub-50.0 territory however, as it has done for the past several years as the Egyptian economy continues to deal with substantial pressures amid elevated inflation and a weakening currency. Output contracted at a slightly faster pace in December than seen the previous month, with respondents citing inflationary pressures.

Looking at prices, the pace of gains in input prices slowed in December but remained fast overall. This was driven predominantly by purchase costs which slowed but remained sharp on the back of currency pressures. Staff costs slowed compared to the previous month and were at the lowest level since July. Businesses are passing on these costs to customers, and output prices continued to climb, albeit at a slightly slower pace than seen in the preceding months. This could be a positive for CPI inflation in Egypt, which we anticipate will continue to slow this year after softening to 34.6% y/y in November.

New orders suggest that output will remain under pressure in the coming months, as they fell at the sharpest pace since May in December, with higher prices weighing on demand. Within that, new export orders declined at a slower pace than total orders. Business optimism improved in December to the second-highest reading of the year, although this remains below the long-run average.

Daniel Richards

Daniel Richards