Recent Search

Popular Searches

UAE

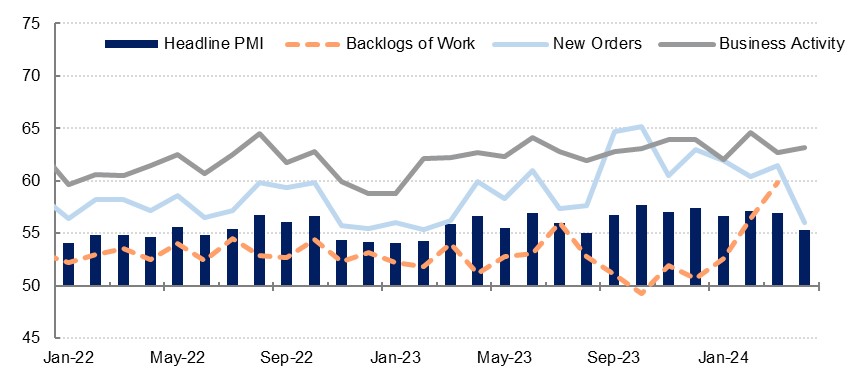

The S&P Global PMI survey for the UAE fell to 55.3 in April, down from 56.9 the previous month. While this remains well above the neutral 50.0 line that delineates expansion and contraction in the non-oil private sector, it is nevertheless the softest reading since last August. That being said, the score was affected by the extraordinary weather event experienced in the UAE in the week starting April 15 when unprecedented rainfall disrupted businesses and activity for several days. While there has been further rain in May this has not been to the same severity, and the impact of the weather should dissipate in the next PMI survey.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

Some of the index’s components actually saw a faster expansion in April than in March, with output in particular picking up again after March’s dip even as some respondents remarked on disruption from the rain. Firms noted that discounting helped boost activity, and output costs continued to fall, albeit at the softest pace in four months. However, new orders saw a fairly sharp slowdown, and while they continued to expand at a robust rate, this was the slowest pace since February 2023. New export orders turned contractionary after a 13-month run of growth, as domestic orders continued to drive the overall expansion.

Backlogs of work continued to expand rapidly, even if at a slightly softer pace than seen in March. Strong order growth has explained part of the uptick, but businesses also cited the storms as disrupting work in April, following on from the disruption to Red Sea shipping noted as a cause in recent months. Purchase costs rose again after dipping in March, with higher raw materials prices driving the increase. Staff costs also ticked higher as businesses compensated workers’ higher costs of living.

Firms continued to expand headcount, and business optimism remained buoyant even as it slipped moderately from the preceding months, with some respondents noting growing competition as new firms entered the market.

KSA

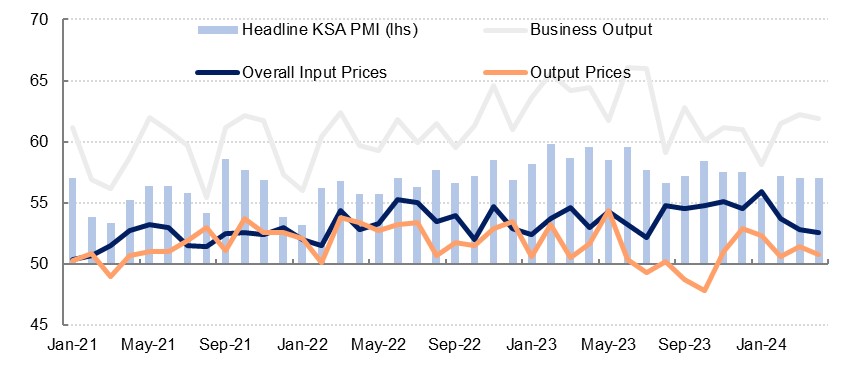

The Riyad Bank PMI survey for Saudi Arabia was unchanged at 57.0 in April, still indicative of strong growth in the non-oil private sector. Business output saw a modest slowdown from March but was still robust, with firms noting that marketing was one of the factors driving growth. The wholesale & retail sector was the primary driver of growth last month. The pipeline for the coming months also looks positive, as although new order growth slowed to a three-month low it remained strong, with firms noting strong local demand. This was borne out by the new export orders component which slowed in April and remained well below the level of total new orders, albeit still expansionary.

Source: Riyad Bank, Emirates NBD Research

Source: Riyad Bank, Emirates NBD Research

Notably, the employment subcomponent turned contractionary in April for the first time since March 2022, albeit only marginally and driven entirely by the construction sector. Firms cutting headcount noted cashflow considerations. Business optimism dipped to an eight-month low in April, although still only less than 2% of responding firms expected that output would fall over the next 12 months and sentiment was largely positive as businesses cited strong economic growth.

Price pressures eased in April after having risen at the start of the year, and input costs slowed to the lowest level since August. Staff costs rose moderately as firms noted cost-of-living pressures, but purchase price pressures softened and rose at the softest pace since July. Firms continued to pass on some of these price rises to customers, but output prices rose at a slower pace than in March, and some firms cut prices as they looked to remain competitive. CPI inflation in Saudi Arabia was at 1.7% y/y in March, down from 1.8% in February.

Daniel Richards

Daniel Richards