Recent Search

Popular Searches

The Turkish central bank held its benchmark interest rate at 17.75% yesterday, despite expectations that there would be a 100bps hike as the TCMB looked to shore up investor confidence. The bank highlighted that cost factors had been the primary driver of the recent spike in inflation, though acknowledged that there had been a milder effect from demand pressures, which would mean that ‘it might be necessary to maintain a tight monetary policy stance for an extended period.’ The lira resumed its sell-off following the announcement.

The composite Eurozone PMI fell to 54.3 in July, compared to 54.9 in June and consensus expectations of 54.8. The manufacturing PMI beat expectations, coming in at 55.1 compared to consensus of 54.7 but the services PMI fell short of expectations, at 54.3 compared to consensus projection of 54.8. Both the new orders and future output subcomponents of the composite index fell to near two-year lows, boding poorly for future performance.

There were also PMI numbers out of the US yesterday, where the composite number dipped slightly, coming in at 55.9 compared to 56.3 in June. Services came in just slightly under expectations of 56.3, at 56.2, but manufacturing exceeded them, recording 55.5 compared to consensus of 55.1. This is a positive sign for Q3, following what looks set to be extraordinary growth of over 4% in Q2, with figures due for release at the end of the week. Strong domestic demand supported the strong growth in manufacturing, taking up the slack from a slight dip in export sales. There was anecdotal evidence returned by the survey that the tariffs introduced by the Trump administration have pushed up input costs. President of the European Commission, Jean-Claude Juncker, arrives in Washington today, for a series of talks on trade. President Trump tweeted yesterday that he has ‘an idea for them. Both the US and the EU drop all Tariffs, Barriers and Subsides!’, but EU officials have said previously that they do not want to negotiate these issues with a ‘gun to their heads.’

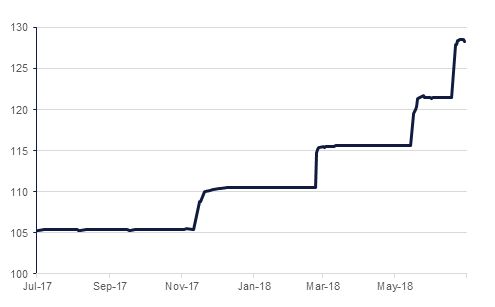

Pakistani elections are being held today, in the midst of a balance of payments crisis and currency sell-off which has seen the rupee fall to new all-time lows of over PKR 128/USD. Long-time challenger Imran Khan is up against the party of recently jailed former PM, Nawaz Sharif.

Treasuries closed mixed as the recent trend of steepening of yield curve snapped. Yields on the 2y UST, 5y UST and 10y UST closed at 2.63% (flat), 2.81% (flat) and 2.94% (-1 bp).

Regional bonds closed higher as it remained in a tight range with the YTW on the Bloomberg Barclays GCC Credit and High Yield index dropping -1 bp to 4.47% even as credit spreads remained flat at 170 bps.

The Turkish lira continued its decline after the surprise decision by the central bank to hold rates yesterday. The currency closed at a record low of TRY 4.8853/USD, and at one point was trading at TRY 4.9384/USD.

Amongst the majors, the Australian dollar was one of the bigger movers. Inflation data of 2.1% y/y missed expectations of 2.2%, confirming the Reserve Bank’s outlook that there would only be a gradual pickup to the midpoint of its 2-3% target range, thereby diminishing the likelihood of a rate hike any time soon. The currency fell 0.2% to AUD 0.7405/USD.

Developed market equities closed higher as strong earnings helped revive risk appetite. The S&P 500 index and the Euro Stoxx 600 index added +0.5% and +0.9% respectively.

Regional markets traded mixed with the DFM index losing -0.2% and the Qatar Exchange adding +1.9%. The rally in Qatari stocks were driven by inflows from foreign investors. Qatar National Bank (+2.0%) and Industries Qatar (+2.4%) were notable gains.

Both oil contracts edged higher yesterday; Brent futures closed up 0.5% overnight at USD 73.44/b, while WTI closed up 0.9% at USD 68.52/b. According to figures reported by Bloomberg, crude stockpiles in the US fell 3.16mn b last week, contributing to the rise in prices

Click here to Download Full article

Daniel Richards

Daniel Richards