Recent Search

Popular Searches

With US Thanksgiving holidays over the markets now have to think about the burning issues that remain between now and the end of the year, including the passage of tax reform in the U.S., a probable rate hike by the Fed, the formation of a new government in Germany, and more meaningful progress in the Brexit talks. An important OPEC meeting also looms in the coming week which will set the tone for oil prices in 2018, with OPEC leaders looking to decide whether to extend production cuts that currently end next March.

The verdict on Thanksgiving holiday retail activity in the US has been broadly a positive one with online sales climbing to a record high, and some department stores also claiming record transactions. The picture completes a broadly positive one for the US economy in November and sets the stage well for December. Q3 GDP in the US is likely to get revised up later this week from the previous 3.0% estimate, but more importantly upward revisions are also being seen to some forecasts for Q4 GDP growth. Both the incoming and outgoing Fed Chairs will be speaking in the coming week, but their comments will be looked at more for guidance about 2018 tightening prospects, with a December hike being increasingly seen as a given.

Attention will also turn to Congress this week, which returns from the Thanksgiving recess and will start work on the tax bill where a version passed the House a fortnight ago, and will be taken up by the Senate this week. The issue of the debt limit which expires on December 8 will also begin being discussed. Elsewhere, the threat of fresh German elections appears to have been lifted by the willingness of the opposition SPD to have talks about the possibility of another Grand Coalition, and with Chancellor Merkel’s CDU also seeing such talks as the best way forward.

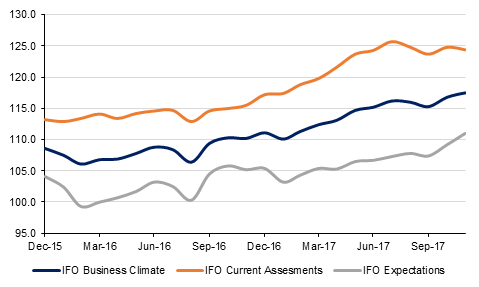

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries drifted lower towards the end of the week amid renewed risk-on activity. Yields on the 2y USTs ended the week at 1.74% (+2 bps w/w), on 5y USTs at 2.06% (+1 bps w/w) and on 10y USTs at 2.34% (flat w/w).

There was renewed interest in regional bonds as noise over geopolitics quietened and oil prices continued their positive run. The YTW on the Bloomberg Barcalys GCC Credit and High Yield index declined to 3.68% (-3 bps w/w) and credit spreads tightened by 4 bps to 159 bps.

With sentiment seemingly looking relatively positive, there is renewed action in primary markets. Emirates REIT has mandated banks for a potential 5 year dollar-sukuk sale of up to USD 425mn.

Abu Dhabi National Energy Co (Taqa) is talking to banks to obtain loan facilities of up to USD 1.3bn to refinance maturing debt. This after reports that the government did not approve a planned bond sale. The company has a USD 750mn bond maturing in January 2018.

The dollar posted declines for a third consecutive week, the Dollar Index falling 0.97% to close at 92.756. Of technical significance is that this close takes the index below several key levels as well as annulling the daily candle patterns of higher highs and higher lows that had been in effect since September. With consideration to key technical levels, the index ended the week below the 200 week moving average (93.345), the price closed below the 50 and 100 day moving averages (93.647 and 93.514 respectively) for three consecutive days. These observations lead us to conclude that from a technical perspective the dollar looks vulnerable to further losses.

EURUSD posed a 1.21% gain last week to close at 1.1933. In the process of doing so, it broke through the 50 and 100 day moving averages and posted a fourth consecutive week of gains. From a technical perspective the firm close above these levels as well as the break out of the former downtrend that had been in effect since September indicates that there could be further upside beyond 1.20 in the week ahead.

It was a sluggish start to the week for regional equities with the exception of the Tadawul (+0.8%). Investor sentiment in Saudi Arabia received a boost from steps taken by CMA to further ease QFI rules and indications that probe into corruption could wind down sooner than expected.

It was no surprise to see stocks which had dropped post the start of the probe rebound. Al Tayyar Travel gained +6.4%. Emaar Development gained +0.5% to start its second week of trading. The stocks still remains below the IPO price.

Oil prices moved higher last week in anticipation of the OPEC meeting at the end of this week. An extension of the current production cuts appears largely priced into markets at the moment but there is some disagreement apparent between major producers over how long the cuts need to remain in place. Brent futures gained 1.8% on the week and WTI futures narrowed the gap with the international benchmark by rising more than 4% on the week.

Markets will likely be twitchy ahead of the OPEC meeting, moving off headlines in volatile trading. We still anticipate that production from OPEC members will increase next year as the current level of oil prices offers attractive export values to support domestic economies. Markets will also be playing close attention to how OPEC and its partners arrange to unwind the deal. Without a clear plan on how they return to pre-agreement production levels, OPEC risks swamping markets with oil even if inventories have narrowed considerably.