Recent Search

Popular Searches

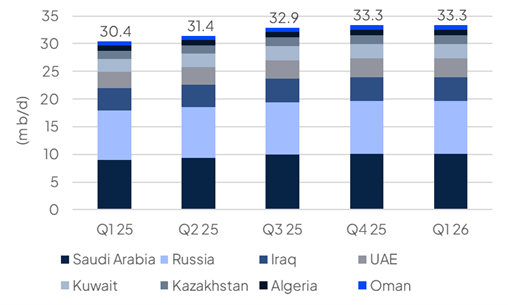

For the first time this year OPEC+ set out production targets for longer than a month ahead. At its early November meeting the eight members of the producers’ alliance that have been phasing output back into the market agreed to increase production by 137k b/d for December and then hold targets at those levels until the end of Q1 2026. The decision to hold output targets unchanged was “due to seasonality” according to a statement accompanying the decision.

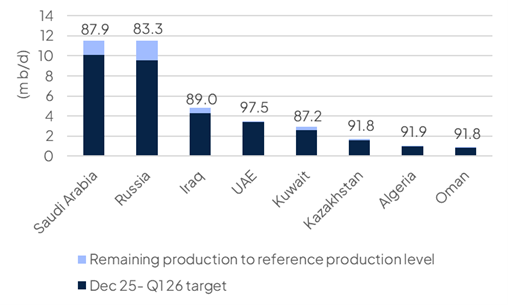

In line with the decisions for October and November, Saudi Arabia will increase production by 41k b/d in December, the UAE by 12k b/d, Iraq by 18k b/d and Kuwait by 10k b/d. Saudi Arabia will now hold output at 10.1m b/d for the next four months, its highest level since the first four months of 2023, while the UAE’s target level at 3.4m b/d represents more than 97% of the country’s reference production level.

Source: OPEC, Emirates NBD Research.

Source: OPEC, Emirates NBD Research.

The decision from OPEC+ to keep output steady until the end of Q1 2026 has been taken positively by the market. There is a broad consensus in oil markets, though seemingly not held by OPEC itself, that oil market balances will shift into a substantial surplus by Q4 2025 and widen into 2026. The decision to hold output steady may be an acknowledgement of those risks by OPEC+, which has otherwise sounded consistently confident in their demand outlook.

The near-term outlook for oil market balances may be substantially disrupted by US sanctions that have been imposed on Rosneft and Lukoil, two major Russian oil producers that account for more than 50% of the country’s production. The sanctions specifically prohibit US entities from engaging with the sanctioned firms but there is a risk that other countries importing oil from either Rosneft of Lukoil could also face sanctions from the US. Further disruption to Russian oil exports could mean that members of OPEC+ with free capacity—such as the UAE or Saudi Arabia—could increase output to keep flows steady.

Source: OPEC, Emirates NBD Research.

Source: OPEC, Emirates NBD Research.Click here to download the report

Edward Bell

Edward Bell