Recent Search

Popular Searches

The next OPEC+ ministerial meeting takes place on June 1 and is likely to include three main themes for its agenda:

The production levels for 2024 have already been substantially revised thanks to the voluntary cuts from some members of the producers’ alliance as well as revisions made at the November 30 2023 OPEC+ ministerial meeting. OPEC+ may officially endorse them for the rest of the year but the targets set mid-way through 2023 are far off from where production actually lies at the moment. For those countries that have not committed to voluntary cuts, there seems to be little need to adjust them. Nigeria has been missing its required production level so far in 2024—output has been at an average of 1.475m b/d for the first four months of the year compared with a target level of 1.5m b/d. Angola rejected its assigned production level after the November meeting and quit OPEC while the other members who have not committed to additional voluntary cuts—Congo, Gabon and Equatorial Guinea—are relatively small producers.

For those producers that committed to additional voluntary cuts, a rollover - either in full or to a high degree - seems to be a forgone conclusion. The cuts were already extended by an additional quarter at the start of March which should help to keep global crude oil balances in deficit for Q2. Extending the cuts in full for an additional quarter and, importantly, complying with them in full would push oil markets into a sizeable deficit for Q3 of nearly 1.4m b/d, a substantial draw. At current estimates for demand growth, we do see space for OPEC+ countries to ease some barrels back into the market in the second half of the year and avoid generating a substantial surplus. Our forecast has been that the cuts would be gradually unwound but with compliance remaining an issue.

An extension of the currently-in-place voluntary cuts would send a signal to oil markets that OPEC+ wants to keep inventory levels under control and avoid blowing out stockpiles amid healthy projections for non-OPEC+ supply growth and trend-level demand growth. Further, it would help to keep oil prices supported at a time when we project Saudi Arabia will be running a fiscal deficit close to 4% of GDP.

Source: IEA, Emirates NBD Research.

Source: IEA, Emirates NBD Research.

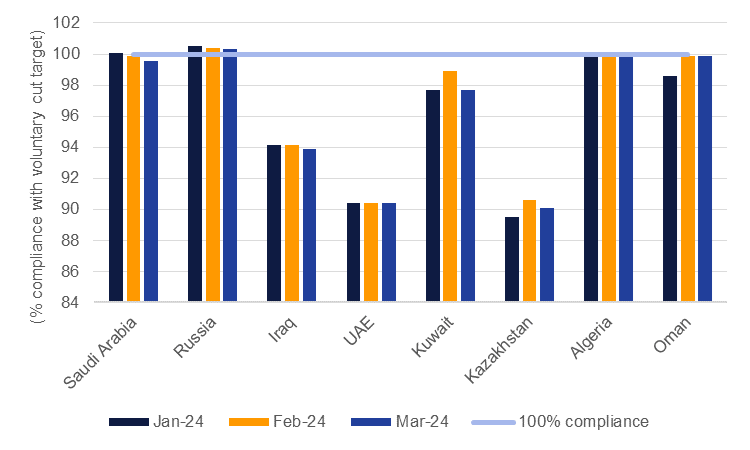

But as ever with production targets, compliance is key. Adherence to target levels has been generally good over the last six months although it has started to slip since the start of 2024. Among large producers in OPEC+, Kazakhstan, Iraq and the UAE have missed their targets this year. OPEC has indicated that it has received compensation plans from both Iraq and Kazakhstan to adjust their production levels over the rest of 2024 to “make up” for over-production relative to target levels. An extension of the voluntary cuts would be a supportive message for oil markets but low compliance to those cuts risks underwhelming the impact.

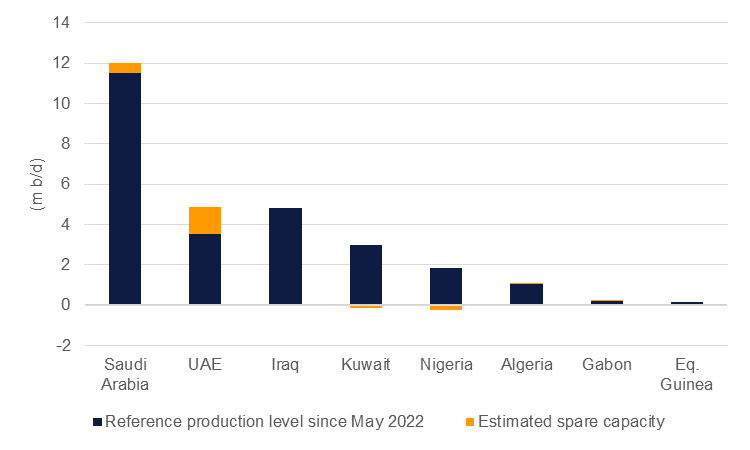

On baseline adjustments, OPEC+ noted at the June 2023 ministerial meeting that by the end of June 2024 all producers would have had an assessment of their production capacity by third-party analysts to be used in setting 2025 reference production levels. Debate around baseline levels has created discord within OPEC+ in the past, including as recently as November last year when target levels for Angola, Congo and Nigeria were revised lower. The UAE has also pushed back against using historic baseline levels that don’t account for substantial capacity upgrades the country has made in recent years. ADNOC has a published production capacity of 4.85m b/d compared with a reference production level set by OPEC of 3.5m b/d. If OPEC+ outlines required production levels for 2025 at the June meeting it may allocate some of the targeted production “missed” by some producers to those that have the capacity to increase production, including the UAE.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

We expect market reaction to OPEC+ announcements from the ministerial meeting to be relatively modest as the options available to the producers’ alliance are limited. Announcing an extension of the voluntary cuts would help to keep oil prices supported in the USD 80-90/b range but this outcome seems to be widely expected by the market and thus upside risks look to be already priced in. A downside risk from the meeting could result from more discord on reference production levels and targets for 2025 that appear “too low” by the expectations of some members. That could raise the risk of more countries leaving the OPEC+ framework and lead toward another battle for market share, similar to that seen in Q2 2020.

Edward Bell

Edward Bell