Recent Search

Popular Searches

Oil prices remain firm this morning having jumped to 6-month highs yesterday following the announcement from U.S. Secretary of State Pompeo that the U.S. was going to end waivers to major oil importers exempting them from Iran sanctions reintroduced last year. The news came with oil markets already in a bullish mood, with global growth picking up, disruptions to oil output from countries like Venezuela, Libya and Nigeria, and amidst continued OPEC-led production cuts. The U.S. administration said it was working with top oil exporters Saudi Arabia and the UAE to ensure the oil market was ‘adequately supplied’ and Saudi Arabia has also said it will coordinate with other crude producers to ensure that adequate supplies are available.

OPEC and its allies including Russia had agreed to limit their production until the end of June to support crude prices and are due to meet next month to assess the market and again in June to decide whether to extend the cuts. The US is now officially targeting zero Iranian exports which would imply a production response of around 1.3m b/d from average Iranian export levels.

U.S economic data was on the soft side overnight with Chicago Fed’s National Activity Index standing at -0.15 in March, while U.S. existing home sales fell 4.9% m/m to 5.210mn also in March. However, apart from oil markets the long holiday weekend was relatively quiet with the USD steady and 10-year bond yields hovering just below 2.60%. Equity markets are braced for more earnigs results this week while the main economic news will be U.S. Q1 GDP data due on Friday, with markets expectations for growth being revised up.

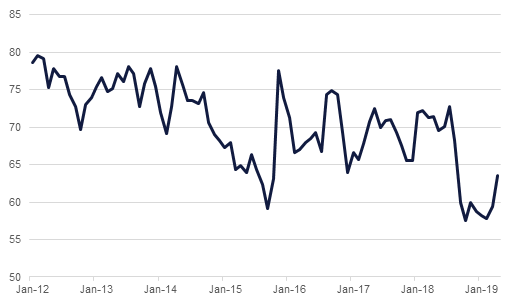

Turkish consumer confidence picked up to 63.5 in April, compared to 59.4 the previous month. This marked the strongest reading since August last year, when the Turkish lira’s sell-off and subsequent economic repercussions led the confidence index to fall from 68.2 to just 59.9 in September. Financial and economic expectations saw similar improvements in the latest survey.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

US treasuries were slightly slippery as many markets remained closed for Easter break. Yields on 2yr, 5yr, 10yr and 30yrs USTs closed marginally higher at 2.39% (+1bp), 2.39% (+2bps), 2.59% (+3bps) and 2.99% (+3bps) respectively. In the Europe, markets were closed for Easter, leaving sovereign bonds unchanged with yields on 10yr Gilts and Bunds staying at 1.20% and 0.02% respectively. Credit spreads were range-bound with US IG and Euro Mian closing at 58bps each respectively.

Regional GCC markets had an uneventful day. Bond prices showed little reaction to better-than-expected quarterly result announcements from the banking sector. Average yield on Barclays GCC index was mostly unchanged at 4.05% though credit spreads were down a bp to 158bps as oil prices reached six month high.

In the primary market, Burgan Bank is likely to tap the market soon after receiving Central Bank’s approval for $ 500million in dollar denominated bonds.

The JPY has recovered overnight as Japanese investors squared short positions ahead of Golden week holidays in Japan. The tightening of U.S. sanctions on Iran has also reduced risk appetite a little helping the JPY to recover. As we go to print, USD is trading 0.10% lower at 111.82. We expect initial support at the 200-day moving average of 111.51, which is likely to restrain further losses. However, it is note worthy that for a third day of trading, the 200-week moving average 111.92 put a cap on further gains for the cross. In order to realize further gains, USDJPY needs to realize a weekly close above this key level, an outcome that has not occurred since December 2018.

Global equity markets had a mixed performance with gains of 0.10% on S&P 500 being offset by loss of 0.15% registered by Dow Jones. In Europe, Euro Stoxx was up 0.62% though FTSE 100 continued to be in the red, closing down by -0.15% yesterday. Equities are fluctuated In Japan and Korea, opened lower in Hong Kong while Australia is gaining in early morning trades in Asia today.

Regionally markets were also mixed yesterday. Abu Dhabi exchange gained another 0.75% on the back of continuing banking shares but Dubai Exchange was largely unchanged amid rising real estate sector. Emaar Development has announced that it plans to distribution up to AED1.04 billion (US$283.15 million) in dividend to its shareholders. In Saudi, the Tadawul index closed down by 0.4% despite rising oil prices.

Oil prices jumped on news that the US would not be offering any more waivers to sanctions for importers of Iranian crude oil. Brent added 2.9% to close the day at USD 74.34/b, its highest level since October 2018, while WTI gained 2.7% to close at 64.70/b. The US will not be providing any ‘grace period’ for importers to adjust and purchases will need to end by May 1.

A production response from countries like Saudi Arabia or the UAE may be forthcoming to offset the drop in Iranian exports but so far there has been no official word on how large an increase markets can expect.