Recent Search

Popular Searches

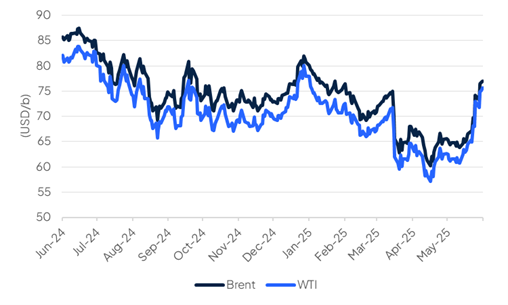

Oil prices have been the primary market expression of the dynamics of the current Israel-Iran war. Oil assets, whether production sites or export infrastructure or ships, have not been directly targeted in the exchange of fire between the two countries but markets are nevertheless pricing in security of supply concerns.

In an immediate reaction to the news of the initial attacks on June 13 oil prices jumped sharply higher. Brent futures spiked to as high as USD 78.50/b and have since been responding to headlines, selling on market indications of a potential diplomatic solution and rising on anticipation that the conflict could deepen or spread.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Volatility in oil prices has surged as markets price in a range of scenarios, all of which seemingly tilt toward the upside, such as attacks on oil infrastructure or the closure of the Strait of Hormuz. Options markets are positioned to the upside by the strongest degree since the start of the Russia-Ukraine war.

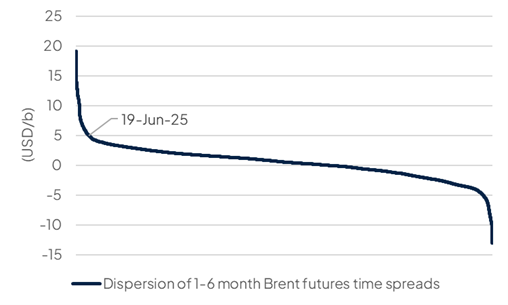

Time spreads have also widened sharply into backwardation, reversing what had been an equivocal stance on the near-term outlook for oil market tightness over the rest of this year. At just shy of USD 5/bbl in backwardation, the current 1-6 month time spread for Brent futures are above the 95th percentile of spreads dating back to 1990.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

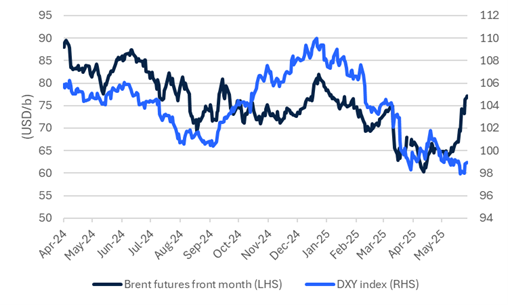

Oil markets have also generally ignored downbeat economic data this week—a drop in US retail sales and a downgrade to growth from the Federal Reserve. Correlation with the US dollar has turned negative in the last several days after oil and the greenback had generally been moving in tandem for much of 2025.

Source: Bloomberg Emirates NBD Research.

Source: Bloomberg Emirates NBD Research.

Our ex-ante assumptions for oil were that prices would decline this year relative to 2024 as supply additions from OPEC+ and other producers overwhelm demand growth and lead to stock-builds. The plans from several OPEC+ countries to accelerate their production increases helped to reinforce that view.

We hold to our fundamentals-based view of the market rather than base our forecast on scenarios that may have a low chance of realization. Geopolitical anxiety, if it does not result in actual supply disruption, tends to burn hot in oil markets but also burn fast. Even the attacks on the Abqaiq oil processing facilities in 2019 saw a spike in oil from USD 60/b to almost USD 70/b in a single day but gains then faded over the subsequent weeks.

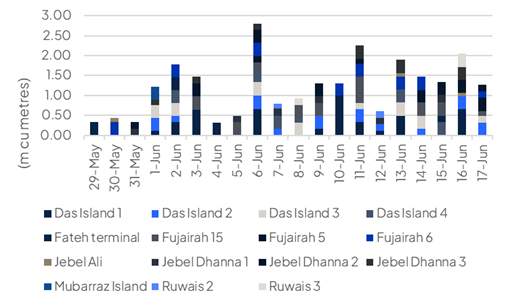

Oil markets are accustomed to geopolitical risk and there is slack available in the market to absorb at least some of the anxiety over supply security. Spare capacity within OPEC+ is estimated at around 5m b/d, though with the caveat that much of that capacity is reliant on access to the Strait of Hormuz to make it out to seaborne markets. For now there has been no material interruption to shipping in the Gulf region. Since June 13 there has been a steady stream of departures from UAE oil export terminals.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

If there is a material change in the fundamental picture for oil markets caused by the conflict we will adjust our price assumptions accordingly.

Edward Bell

Edward Bell