Recent Search

Popular Searches

Oil markets are set to loosen in the coming months as OPEC+ looks likely to accelerate a return of production. On May 5 those members of the exporters’ alliance that have been providing additional cuts will set output levels for June after having announced on April 3 that May target levels would be higher than originally planned. The May levels, which represented three months’ worth of increases in a single month, were meant to act as a production discipline measure to curb over-production from several OPEC+ members.

It appears likely that June will also see another large boost to output as over-production has still not stopped and the messaging from Saudi Arabia appears to favour higher output. Press reports have suggested that Saudi Arabia is prepared to accept lower prices for a longer period to secure market share for their own exports and to try and enforce some discipline among countries that are producing above target levels.

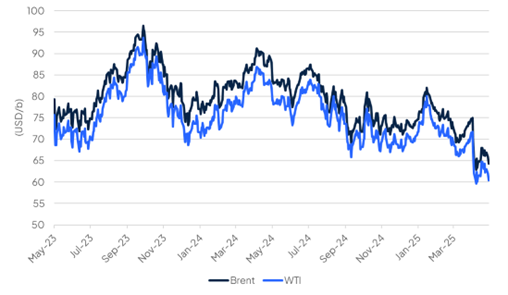

Oil markets tanked on the expectation that June production targets will be set at higher levels. July Brent, the current front month, dropped 3.5% on April 30 to USD 61.06/b while front month WTI has pushed again below USD 60/b, falling 3.7% at the end of April to USD 58.21/b.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

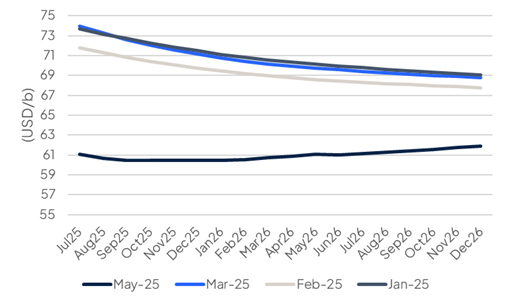

The shape of the oil futures curve has also shifted considerably over the last several months. After having been in a steady, if shallow, backwardation to the end of 2026 for most of this year, the Brent futures curve is now in contango from December 2025 onward, creating an uncommon swoosh shape.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

That shift into contango further out in the curve reflects, in our view, the expectation that markets won’t be short on supply thanks to higher output from OPEC+ as well as other producers but also growing anxiety that the world economy will slow materially this year and next and lead to much slower oil demand growth. The IEA had already incorporated a lower global GDP growth outlook in its April oil market report, ahead of the publication of the IMF’s downgraded WEO published in April. But as more signs of fragility emerge in major economies—the US economy shrank in Q1 2025 and Chinese manufacturing has contracted again as of March—then demand growth expectations will likely be shaved further.

For now, OPEC+ looks set to accept oil prices at a lower level than the past several years and we expect it won’t backtrack on plans to increase output, even if it opens up more downside to markets. Our expectation remains for Brent at an average of USD 68/b on average this year, trending lower towards the end of 2025.

Edward Bell

Edward Bell