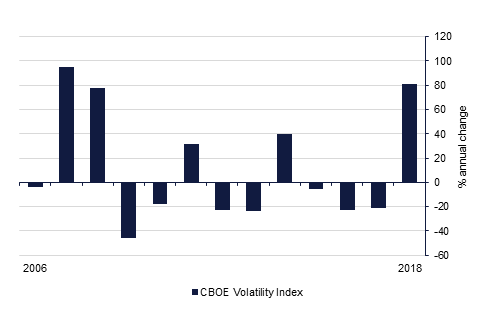

As the year end comes into view the outlook for 2019 is becoming increasingly hazy and volatility is rising. Trade tensions, monetary policy normalization and geopolitical risks are all themes that will carry over from 2018 into next year, and perhaps intensify, adding to questions about whether current growth rates can be sustained and whether financial markets can continue to hold up.

The next Monthly Insights will be released in January 2019.

- Global macro: We recently visited the US where we met with a number of market participants and a surprising degree of unanimity about the outlook for the US economy.

- GCC macro: As we head into the final stretch of the year, the downside risks to growth in the GCC appear to be increasing.

- MENA macro: Although the US announced just prior to the reimposition of stringent sanctions on Iran on November 5 that it would in fact grant waivers on imports of Iranian crude to eight countries, we see this more as a stay of execution for the Iranian economy rather than any significant lifeline.

- Interest Rates: The UST yield curve continued to move higher though sovereign yields in other developed economies softened in anticipation of slower global growth ahead.

- Credit Markets: Credit spreads on GCC bonds increased in response to falling oil prices and rising geopolitical risks in the region.

- Currencies: Approaching the midpoint of the final quarter of 2018, the dollar has continued to appreciate, reaching an 18-month high.

- Equities: Global equities remained weak as investors began to position themselves for greater political and monetary policy unpredictability and uneven economic growth heading into 2019.

- Commodities: Middle East oil exporters face a challenging year in 2019 as weaker demand projections, moderating supply risks and fuel quality regulations bite into the market.

Volatility turning sharply higher heading into 2019

Source: Bloomberg,Emirates NBD Research

Source: Bloomberg,Emirates NBD Research

Click here to Download Full article