Recent Search

Popular Searches

The last week has seen a sharp adjustment in U.S. interest rate expectations, especially after May’s job data dramatically undershot expectations. Trade tensions also remain a prominent factor in causing markets to bring forward expected rate cuts, with U.S.-China trade frictions being added to by U.S.-Mexico trade uncertainty over the last week. A deal to avert U.S. tariffs on Mexico was apparently struck on Friday, but there is still some uncertainty as to what this deal actually represents as it conflates a number of different issues. However, it is not only the U.S. that is contemplating easier monetary policy. Globally too expectations for more monetary policy stimulus are building with Australia’s RBA and India’s RBI cutting interest rates last week and the ECB also signaling that it is open to re-opening QE. So while the USD has lost ground against a range of currencies, its losses have been tempered by the dovishness of others.

With regional markets largely closed last week, they are reopening this week with a more dovish policy tone globally, amidst ongoing concerns about growth. The G20 finance ministers meeting in Japan concluded with a communique warning that escalating trade and geopolitical tensions represent a significant downside risk to growth, while U.S. jobs data appeared to underscore this risk. The report showed a weaker than expected 75,000 gain in non-farm payrolls, and downward revisions to previous months’ data. While the unemployment rate stayed at 3.6%, and wage growth was steady at 3.1%, the release supported the notion that the US economy is losing momentum, with the 3-month rolling average for payrolls dropping to 151k from over 200k in late 2018. In the wake of recent comments from Fed officials that a rate cut could be warranted ‘soon’, the markets are thinking this could mean the summer. We doubt this will occur at the next FOMC meeting on June 18 and 19th, or even that the one after that in July, but it seems clear that the Fed will adjust its language and probably also take away the rate hike that is included in its dot-plot for next year. Most likely the Fed will want to see how the trade dispute with China plays out in the data over the summer, with a continued loss of economic momentum probably needed to justify a rate cut before the end of the year.

The USD does not just have US fundamentals to consider as the other central banks have been even faster than the Fed at adjusting their policy frameworks. Geopolitical issues are also an ongoing concern that affect more than just U.S. growth and sentiment. U.S. data will be important in the coming week especially key numbers on inflation, retail sales, and production. Economic data out of Europe is unlikely to change the market's negative outlook on Eurozone growth, while in Asia, Chinese exports and imports data will be watched closely as will industrial production, fixed investment and retail sales.

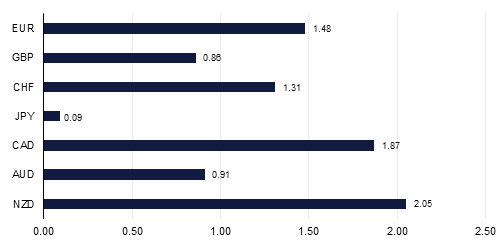

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg