Recent Search

Popular Searches

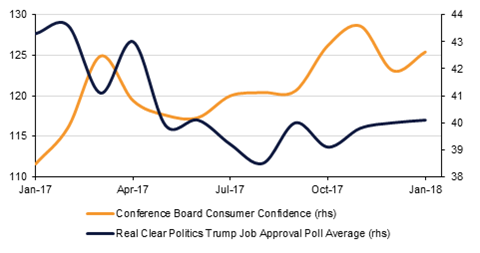

Donald Trump’s State of the Union address declared a ‘new American moment’ of wealth and opportunity emphasizing the progress that has been made on the economy in the first year of the Trump White House. He cited the creation of 2.4 million new jobs in the past year, highlighted the passage of tax reform and the strength of the equity markets and called for USD1.5 trillion to be spent on new infrastructure while reaching out for bipartisan support. On trade he pledged to fix ‘bad trade deals’ and to negotiate new ones. The upbeat tone chimed with optimism captured by consumer confidence data yesterday, with the Conference Board index rising to 125.4 in January up from 123.1 in December, but it contrasts with Trump’s own popularity which lies in the low 30 percentile. Whether or not the speech can turn his political fortunes around by an appeal to bipartisanship is unclear as Trump remains highly divisive within Congress and across the United States as a whole. The next big focus today will be on the outcome of the Fed’s FOMC meeting this evening, the last under Janet Yellen’s Chairmanship.

Elsewhere, data released overnight showed China’s January manufacturing PMI dipping fractionally in January to 51.3 from 51.6 in December, although the non-manufacturing index firmed slightly to 55.3 from 55.0.

Meanwhile the Eurozone continued to show resilient growth at the end of 2017. Advance reports showed that the aggregate GDP for the Eurozone grew 0.6% q/q and 2.7% y/y in Q4, accompanied with an upward revision in Q3 growth from 2.6% y/y to 2.8% y/y. While the data does not highlight the various component contributions to GDP, timelier data from France shows that growth was broad based and benefited multiple sectors.

In addition to Q4 2017 GDP data, the European Commission Economic sentiment indicator continues to suggest a healthy pace of growth. While the reading fell to 114.7 in January, compared with 116.0 in December, for the first slowdown in eight months, it still suggests that strong growth is being maintained in Q118.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

UST yield curve shifted slightly downwards ahead of FOMC meeting today. Government bonds generally gained in the developed world after Bank of Japan reaffirmed its commitment to ultra loose monetary policy and offered to buy more bonds at a regular operation for the first time since July last year. Yields on 2yr and 10yr UST fell by a bp each to 2.11% and 2.70% respectively and those on 10yr Bunds and JGBs were also down by a bp each to 0.68% and 0.07% respectively.

Regionally GCC credit +HY bond index was range bound with yield at 3.90% (+1bp) and credit spreads at 145bps (unchanged) amid unsurprising result announcements and some M&A related news. CDS levels on GCC sovereign were also largely unchanged with Qatar, Abu Dhabi and KSA closing at 89bps, 51bps and 77bps (-1bp) respectively.

In the primary market, A3 rated, Dubai Islamic Bank raised $1.0bn via 5yr sukuk that priced at MS+115, 115bps tighter than the initial guidance of MS+130bps, against order book of over $1.6 billion. Looking ahead, Emirates NBD has hired banks for a possible 10yr tenured A$ transaction.

Despite starting Tuesday on a softer note, the Euro recovered in the aftermath of supportive economic data (see macro), to pare earlier losses and finish the day on firmer footing. Having traded as low as 1.2335, EURUSD found support near the 200 hour moving average (1.2336) and was able to overcome the original resistance at the 50 hour MA (1.2399) which now acts as a support. While the price remains above this level, the risk is that the “Shooting Star” identified earlier in the week has failed to be confirmed and we could see the EURUSD cross climb higher as we head into the outcome of FOMC meeting. While investors expect the Federal Reserve to hold the Fed Funds Target Rate at 1.50%, they will be scrutinizing the monetary policy statement for any changes in language during Janet Yellen’s last meeting as FOMC Chair.

AUD underperforms this morning following softer than expected economic data. Consumer prices rose 1.9% y/y in Q4 2017, up from 1.8% in Q3 but missing expectations for a gain of 2.0%. As we go to print, AUDUSD trades 0.10% lower at 0.80753.

Developed market equities closed lower amid rising bond yields and mixed corporate earnings. The S&P 500 index dropped -1.1% and the Euro Stoxx 600 index lost -0.9%.Regional equities closed mixed amid a slew of corporate news flow. The Qatar Exchange lost -1.3% while the Tadawul added +0.8%.

Dubai Islamic Bank (-4.6%) dragged the DFM index lower after the bank decided to seek shareholder’s approval to raise AED 1.65bn from rights share offering. The shareholders will have right to buy 1 share for every 3 share held. Emirates NBD gained +6.5% after the bank confirmed that it is in early stage talks with Sberbank regarding buying a stake in Turkey’s Denizbank.

Oil declined for a third consecutive trading session after industry data showed US crude stockpiles rose for the first time since November 2017. WTI prices dropped -1.6% to close at USD 64.5/bbl and Brent prices dropped -0.6% to close marginally above the USD 60/bbl level.

Gold prices continue to remain in a tight range around the USD 1340 per ounce level since the start of this week even as volatility in finance markets picks up.

Click here to Download Full article