Central banks globally have taken substantial steps to offset the negative economic impact of the Covid-19 pandemic. We outline below some of the major initiatives that central banks in developed markets have undertaken in response to the crisis.

US

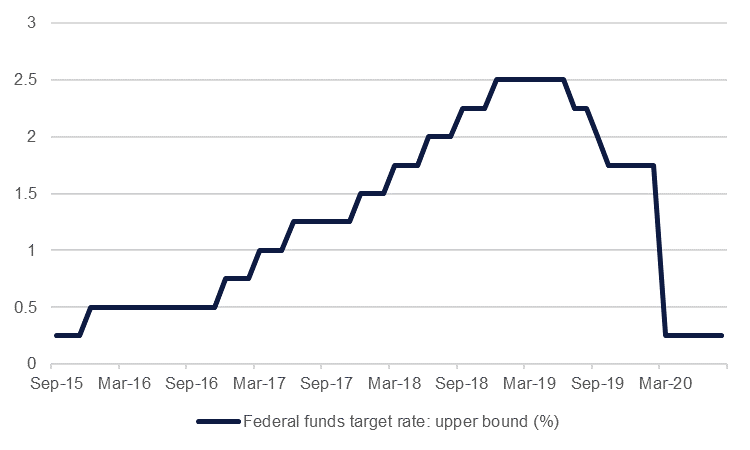

- The US Federal Reserve cut its Fed funds target range by a cumulative 150bps in March, taking it back to the lows of the Global Financial Crisis and subsequent period of slow growth.

- Speculation regarding the possibility of negative rates being implemented in the US has died down, but Fed chair Jerome Powell has indicated that there is little chance of any hikes through 2022.

Fed funds rate

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- Minutes from recent FOMC meetings have indicated that there is little support amongst board members for yield curve control policies.

- The Fed unveiled the outcome of its policy review at the 2020 Jackson Hole central bank summit and has outlined a greater focus on inflation. The Fed will now target inflation that reaches an “average of 2% over time”, allowing for prices to run higher than targeted to make up for periods of underperformance. Given the structural factors in the US economy that lean toward long-term deflationary pressures—an aging population for instance—and the cyclical damage to the economy from Covid-19—excess physical and human capital in a depressed economy—the Fed may still struggle to reach an average level of 2% inflation.

- The central bank has indicated that it will continue with its QE programme, and could even accelerate asset purchases if it deems it necessary. As of August 10, the bank’s balance sheet stood at USD 6.95tn. Down modestly from the USD 7.17tn seen in June, but still huge compared to the USD 4.24tn at the start of March.

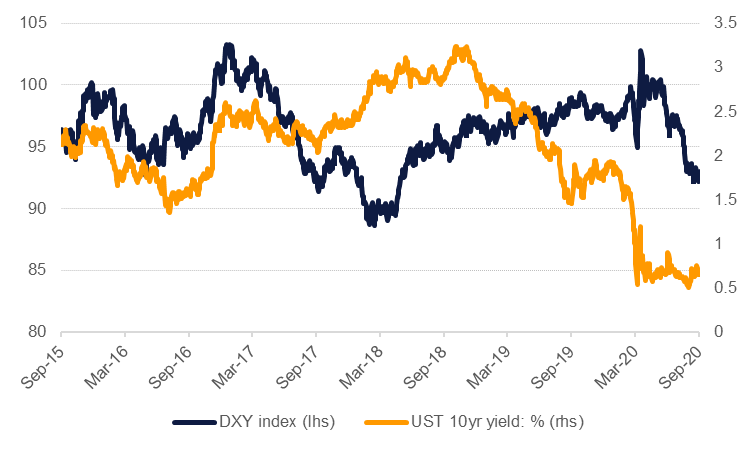

US dollar index and 10yr UST yield

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- At the height of the crisis and facing a dollar soaring to three-year highs, the Fed moved to broaden existing swap lines with other central banks, and implemented new ones. These now look set to run until March 2 and the dollar has subsequently weakened to a two-year low as of mid-August.

- The next FOMC meeting is scheduled for September 15-16 2020.

Eurozone

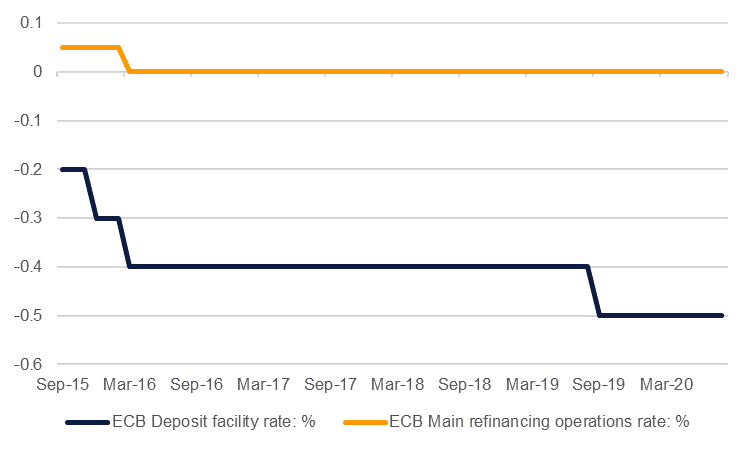

- The ECB has thus far left its deposit rate on hold since the start of the pandemic crisis. The benchmark interest rate for the currency bloc was already at -0.5% following a 0.1bps cut in September 2019, and has been in negative territory since 2014.

ECB policy rates

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- The bank has indicated that rates will remain at present or lower levels until inflation nears 2%.

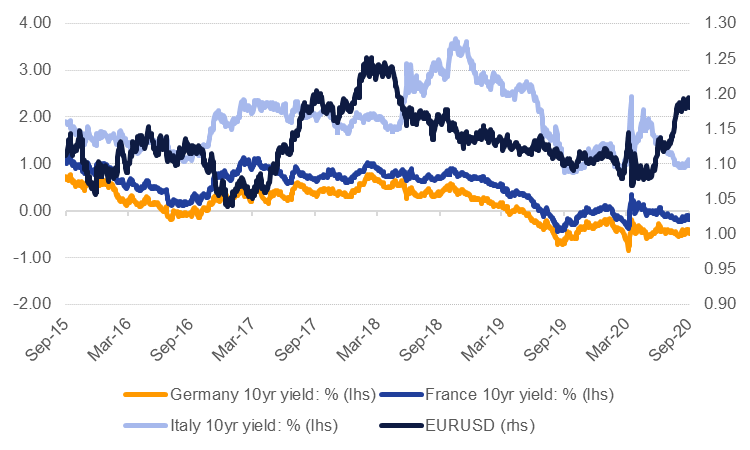

- The ECB has embarked on a massive stimulus package, with an additional EUR 600bn announced at its June meeting taking the total to EUR 1.35tn, the so-called PEPP expansion. The programme will be maintained until June 2021 at least.

Eurozone bonds and EURUSD

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- Other moves have included more favourable rates applied to TLTROs until June 2021, which aims to ensure that banks continue to lend to SMEs that might be struggling owing to the pandemic crisis.

- The next ECB meeting is scheduled for September 10 2020.

Japan

- The Bank of Japan has generally enhanced policy measures that it already had in place (quantitative easing, special funds-supplying measures) to offset the economic impact of Covid-19.

- Policy rates have been maintained at -0.1% where they have been since February 2016 and there are no signs of any pending change higher (or lower) for rates.

- That has left quantitative easing and other financial support as the BoJ’s main policy tools to support the economy. At its April meeting the BoJ removed its JPY 80trn annual target for purchases of JGBs and was more explicit in following meetings, indicating there was no “upper limit” to its purchases aiming to keep 10yr JGB yields at 0% (yield curve control).

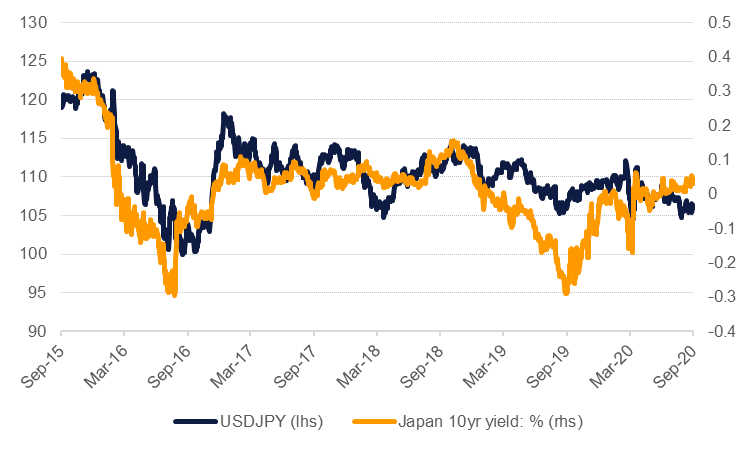

USDJPY and JGB yields

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- The BoJ has also provided support by increasing its targets for purchases of commercial paper and corporate debt (around JPY 20trn in total out to March 2021). Purchases of ETFs and Japanese REITS has also increased to JPY 12tn and JPY 180bn respectively.

- BoJ will also provide liquidity to banks (special funds-supplying operations) covered initially by corporate debt but now rolled out to more sectors of the economy (total liquidity will be around JPY 75tn and include SME and household debt).

- In early August Governor Haruhiko Kuroda indicated that CP/corporate debt purchases could be extended beyond March 2021 if warranted and BoJ would consider increasing ETF purchases or lowering rates.

- Next meeting September 17 2020.

UK

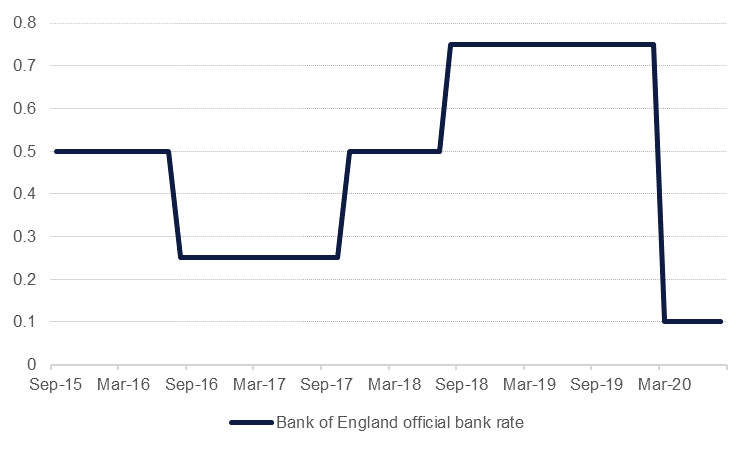

- The Bank of England cut by a cumulative 65bps in March, taking the benchmark bank rate to 0.1%. While Governor Andrew Bailey has said that negative rates are ‘in the toolbox’, it does not appear that they are likely anytime soon. At the bank’s August meeting the vote to maintain rates at their existing levels was unanimous.

Bank of England bank rate

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- The central bank also maintained its asset purchase target of GBP 745bn at its August meeting. This implies an additional GBP 300bn from where the bank’s balance sheet stood prior to the crisis.

- Board members have indicated that they will do more if necessary, but judge the current measures sufficient for the time being.

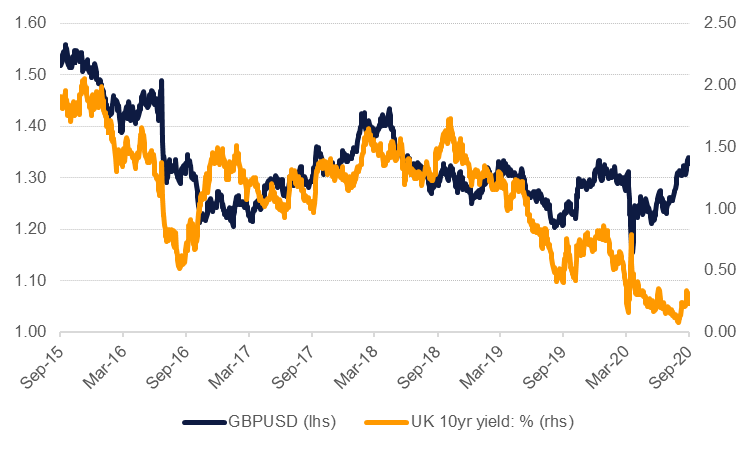

GBP and gilts

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- The bank’s forward guidance is clear that it will not look to tighten policy until inflation nears the 2% target.

- The next BoE meeting is scheduled for September 17 2020.

Canada

- The Bank of Canada cut rates by 150bps in March in an immediate response to the Covid-19 pandemic and has since kept rates on hold. Futures markets are implying no change to rates until possibly Q3 2021.

- Like other developed markets central banks, the BoC has expanded its balance sheet by buying federal government debt along with provincial bonds. The bank will also buy corporate debt and commercial paper. The Bank of Canada did not adopt quantitative easing during the 2008-09 financial crisis and the new governor, Tiff Macklem, has expressly described the programme as stimulatory, rather than just serving to ease financial conditions.

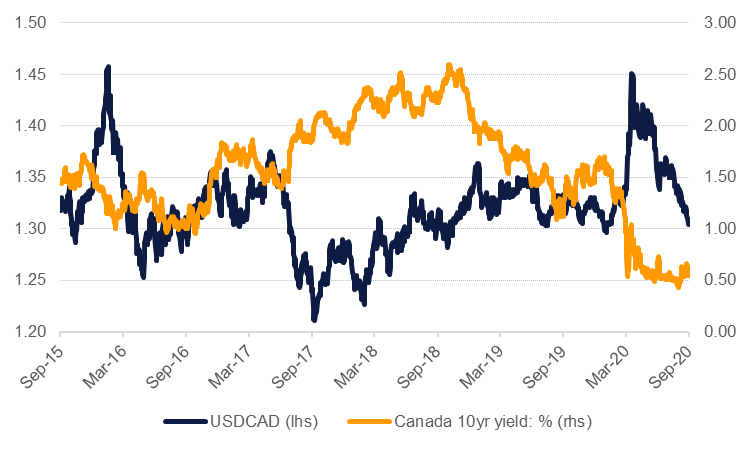

USDCAD and Canada government bond yields

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- The BoC indicated at its July meeting that rates will be low until inflation hits a target of 2% on a sustained basis. However, the bank’s own forecasts anticipate that is unlikely until at least 2022. Recent inflation prints in Canada have moved close to 0%.

- The next BoC meeting is September 9 2020.

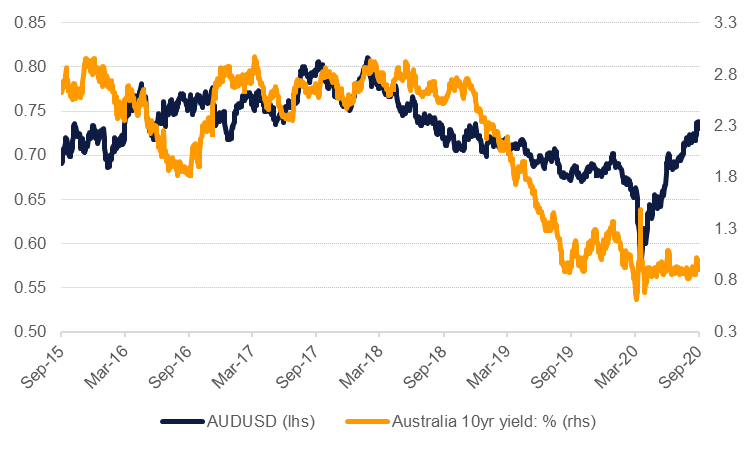

Australia

- The RBA cut the cash rate target by 25bps twice in March as its initial response to the coronavirus pandemic. Rates have been on hold at 0.25% since then.

- Apart from the Bank of Japan, the RBA is the only other developed market central bank to adopt yield curve control. The RBA is targeting a 3yr government bond yield of around 0.25%.

- On top of these measures, the RBA has introduced a term funding facility charged at 0.25% and available for three years. The total amount was raised at the RBA’s September meeting to around AUD 200bn with a priority for banks to lend to the SME sector.

AUDUSD and Australian government bond yields

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- Australia had some initial success in implementing a public health response to Covid-19 but there have been flare-ups of the disease in some states (Victoria in particular). However, the RBA has been reluctant to enhance monetary policy further and has pushed for fiscal stimulus to carry the burden. Governor Philip Lowe has indicated that adopting a negative rate policy is “unlikely” but wouldn’t rule it out completely in testimony to parliament.

- The RBA’s next policy decision is October 6 2020.

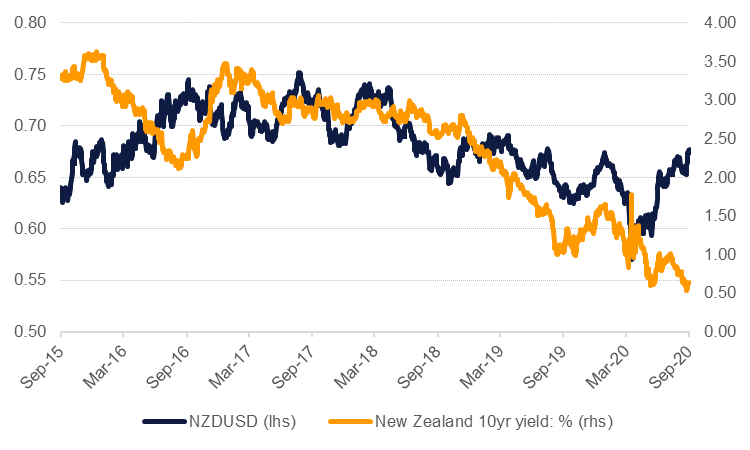

New Zealand

- The RBNZ cut the official cash rate by 75bps in March to 25bps and has held it at that level since. Since then policymakers have mooted the idea of taking the OCR negative with and futures markets expect rates to move negative as of Q2 2021.

- The RBNZ also introduced large scale asset purchases (QE) with an initial target of NZD 30bn. However, that has been raised incrementally at subsequent meetings and as of the bank’s August meeting, the RBNZ will buy up to NZD 100bn of NZ government bonds out until June 2022. The RBNZ doesn’t have an explicit target yield but lowering long-term borrowing costs and weakening the NZD are part of its expectations when using LSAP.

NZD and New Zealand government bond yields

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

- The RBNZ has deployed term lending for the banking sector at maturities up to three years. A next step would be direct ‘funding for lending’ to the banking sector to transmit lower borrowing costs directly to the retail sector. The RBNZ indicated at its August meeting that it would be a preferred option along with further LSAP or a negative policy rate. Funding would likely be at close to the level of the official cash rate.

- Officials from the bank have also been outspoken in wanting a lower NZD level to help support the economy.

- Next meeting is September 23 2020.

Daniel Richards

Daniel Richards