Recent Search

Popular Searches

Conditions for metals markets are improving as the global economy steps moves out of its Covid-19 induced lockdown but the recovery in prices are likely to be uneven. Idiosyncratic supply dynamics in particular will set the tone for prices going forward with some major producers enduring the most significant Covid-19 outbreaks, resulting in production disruptions. Demand conditions are trending higher but most government support plans have focused on soft infrastructure or social spending, not capital-intensive infrastructure. Precious metals have received support as investors flood into safe havens amid an uncertain outlook for riskier assets. Gold prices are nearing in on all-time highs with factors to limit the upward move.

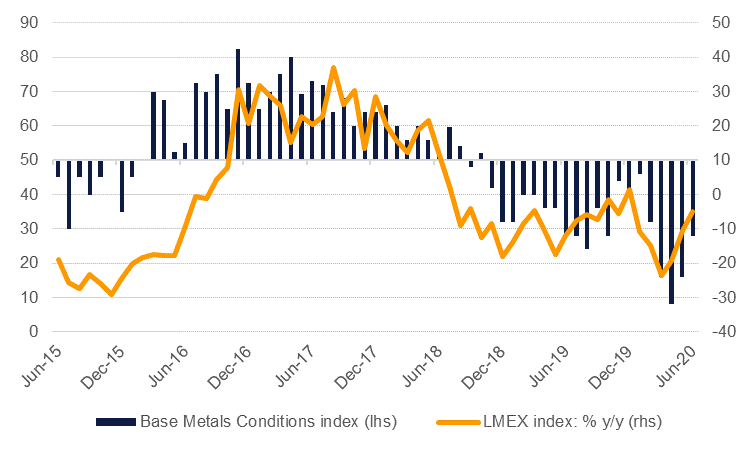

We estimate that conditions for base metals hit an absolute bottom in April this year as global PMIs sank, industrial activity collapsed and inventories near across the board of the six major non-ferrous metals increased. Since then conditions have been trending higher but still correlate with the LMEX index declining year/year.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

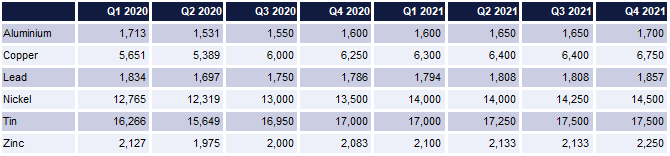

The standout performer has been copper. LME 3mth copper forwards have pushed back above USD 6,000/tonne in recent weeks, gaining almost 35% from the bottom of USD 4,630/tonne, and have managed to post a very modest gain year-to-date. Across the rest of the LME complex prices have all recovered from the troughs but none have yet to record year-to-date gains.

Source: Bloomberg, Emirates NBD Research. Note: USD/metric tonne.

Copper has gained thanks for substantial rates of Covid-19 infections in both Chile and Peru, two major sources of copper ore. Mines have had to reduce staff to try and keep case numbers under control while unions have been pressing for safer conditions. Time spreads for cash-3mth forwards on the LME have seen their contango narrow considerably from as wide as USD 35/tonne in May to closer to neutral now—and actually did flip briefly into backwardation in early July. Investors have also begun extending speculative long positions on the red metal after having spent most of 2019 and early 2020 as a net short.

Copper inventories are the one missing piece for a strongly bullish signal as there a conspicuous draw has been absent—hardly surprising given the lockdowns that curtailed industrial demand for much of Q2 2020. Nevertheless we believe copper has a strongly supply constrained picture and expect prices to extend their gains over the rest of 2020 and into 2021. We expect prices to record an average of USD 6,125/tonne for H2 2020 before building momentum and averaging around USD 6,500/tonne in 2021.

Aluminium markets haven’t displayed the same level of production restrictions as copper but have still had to bear the brunt of substantial demand decline. Aluminium production in China—the world’s dominant producer—has continued to run relatively steady even as Covid-19 first emerged in the country. Production in higher-cost locations has yet to respond meaningfully to lower prices although company announcements over the past few months have indicated the smelters will start to be closed.

Meanwhile aluminium premiums have been trending lower as consumers take advantage of low underlying prices and a relatively stable inventory picture. LME stocks have actually been moving higher since the start of the year with the share of cancelled warrant metal declining to just 15% of total stocks compared with closer to 40% at the start of the year. Aluminium prices should benefit from the broad recovery in risk sentiment but we expect it will underperform copper and may be at risk of downside if supply reaction ex-China remains slow.

Source: Bloomberg, Emirates NBD Research. Note: USD/metric tonne.

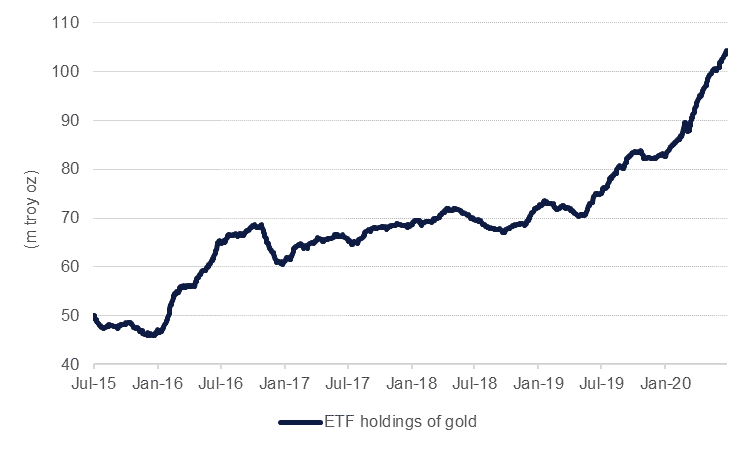

Precious metals prices have shown a split performance in the wake of the coronavirus pandemic. Investors have flocked toward gold as a safe haven bin, particularly as central banks have slashed interest rates and adopted increasingly unorthodox monetary policies. ETF holdings of gold are up 39% y/y as of mid-July and a recent push toward and above USD 1,800/troy oz may prompt the last gold sceptics to throw in the towel and buy into the metal. Gold prices are not far off their peak level of USD 1,900/troy hit in September 2011 and we expect that prices can be sustained around their current levels or higher at least until the end of the year.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The upward push in gold will pull the rest of the precious metals prices higher but the relative gains will be limited by their much higher industrial demand profiles. We expect silver and platinum to underperform gold this year while supply constraints continue to support the palladium outlook.

Source: Bloomberg, Emirates NBD Research. Note: USD/troy oz.

Edward Bell

Edward Bell