Recent Search

Popular Searches

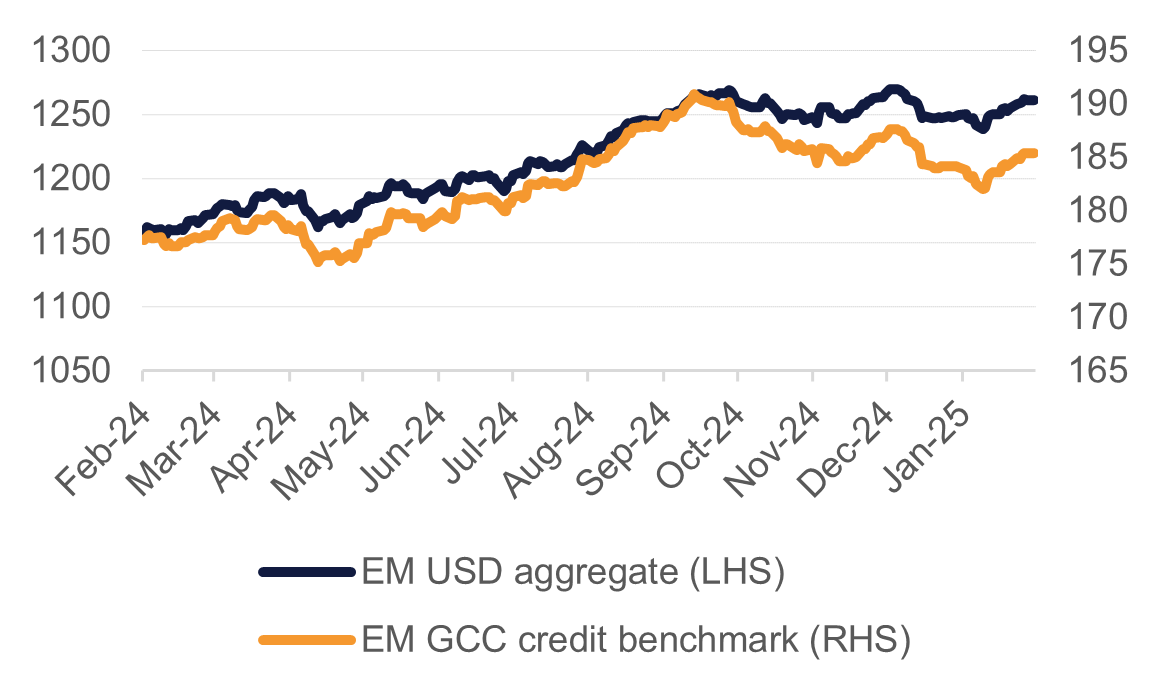

Emerging market bonds remained on an upswing last week with Bloomberg’s USD-denominated index up 0.5%, taking the rally in EM bonds to four weeks out of the last five. Market focus this week will be on the fallout from tariffs announced by US President Donald Trump on Canada, Mexico and China and the potential for disruptions to global trade to spread further. Mexican bonds account for more than 8% of the EM USD-bond index we track and selling pressure there may flatten the near-term price outlook for EM bonds.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

GCC bonds had a positive session last week with a broad index of GCC USD-bonds up 0.5% though spread tightening was relatively limited. By sector, IG bonds rallied 0.6% last week with sovereigns up around the same amount. High-yield regional bonds gained 0.3% with spreads wider by almost 3bps. Sukuk rallied 0.9% last week.

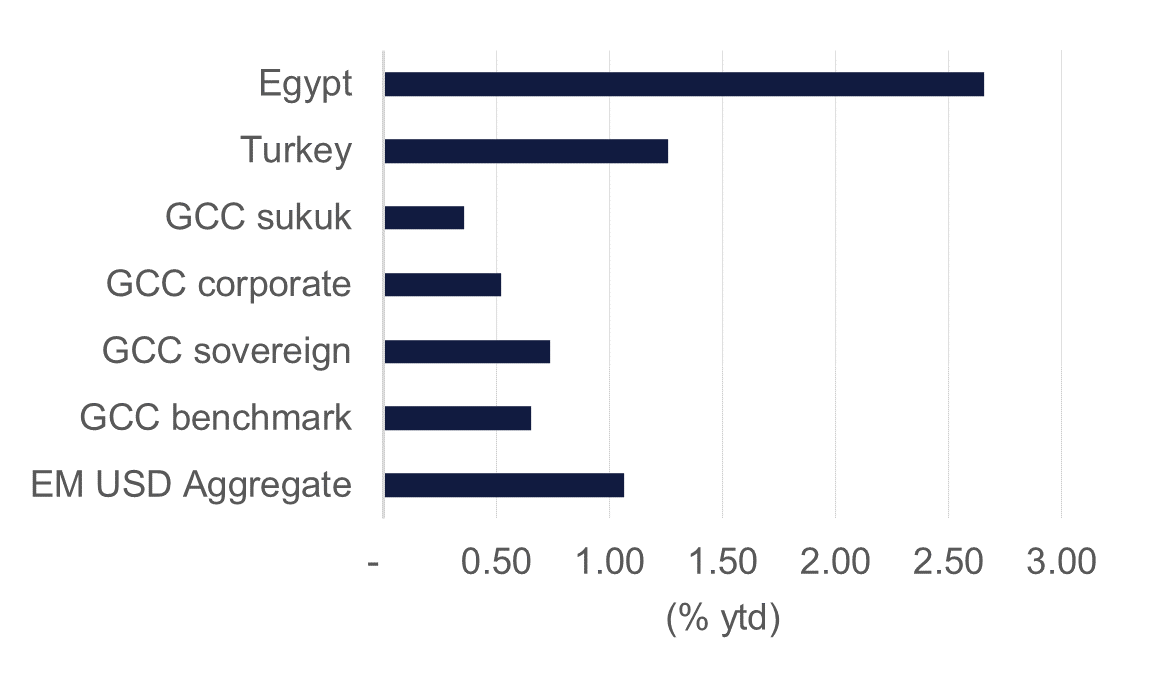

Since the start of the year emerging market bonds have rallied about 1.1% while GCC bonds have pushed higher by about 0.7%. Both have outpaced global aggregate bond indices, outperforming US, European and Asian markets.

By geography Saudi Arabia was the main winner last week with bonds up 0.7% (spreads tighter by 2bps) while UAE-wide USD-bonds gained 0.5% (spreads marginally tighter). GCC markets are indirectly exposed to the impact of the trade disruptions and with all GCC economies running trade deficits with the US (they import more than they export), they are unlikely to be directly targeted for tariff actions.

Turkish bonds gained 1.1% last week with spreads tighter by more than 4bps while Egyptian bonds closed lower by 0.9% and spreads pushed up by 33bps.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

In local data, Saudi Arabia printed GDP growth of 1.3% in 2024 thanks to a strong performance in Q4. The non-oil economy increased by 4.3% in 2024 while the oil sector contracted by 4.5%. In Q4 the non-oil economy rose by 4.6% y/y. This week PMI data compiled by S&P Global will set the macro theme for the GCC economies.

Fitch affirmed Saudi Arabia’s sovereign rating at ‘A+’ with a stable outlook. The rating agency noted Saudi Arabia’s “strong fiscal and external balance sheets” and a debt/GDP level much lower than comparable peers.

Fitch also affirmed their ‘BB-’ sovereign rating on Turkey, with a stable outlook.

Kuwait announced a budget for its fiscal year starting April 1 2025, estimating a deficit at USD 20.5bn with expenditure just 0.1% lower year/year while revenue is projected to drop nearly 4%. Kuwait’s estimated break-even oil price is USD 90.50/b, roughly 18% higher than current prices. Market reports suggest Kuwait will pass a new law allowing the sovereign to borrow up to KWD 20bn (USD 65bn) over a period of 50 years. Kuwait last tapped international markets in 2017, raising USD 8bn in a dual tranche issue (a USD 3.5bn 5yr matured in 2022 while a UDS 4.5bn 10yr matures in 2027).

Last week was the first since the start of the year when there was no benchmark borrowing from regional corporates or sovereigns. Since the start of the year total USD bond and sukuk borrowing has hit USD 26bn, slightly more than the USD 24bn raised in the same time last year.

Edward Bell

Edward Bell