Recent Search

Popular Searches

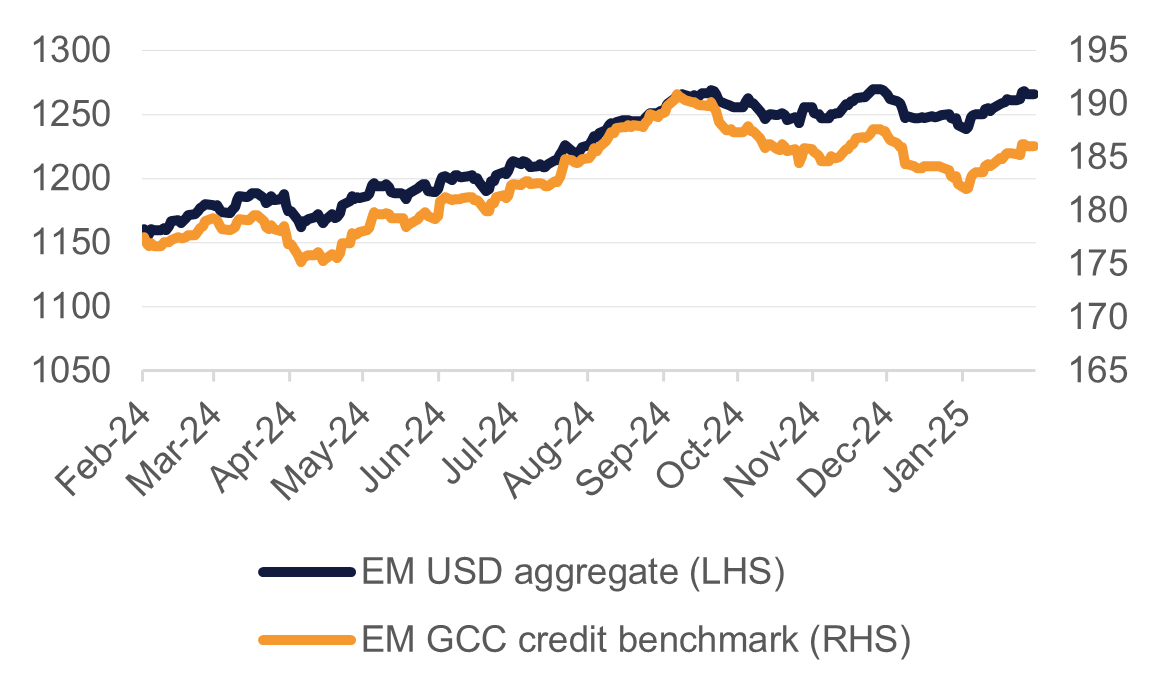

Emerging market hard currency bonds extended their year-to-date gains last week even amid the uncertainty around global trade as the administration of US President Donald Trump imposes or threatens tariffs. EM USD bonds rallied 0.4% last week, taking their year-to-date gains to 1.5% as of February 7. Many mid- to large emerging economies have a high dependency on trade for their economies, as exporters of raw materials or value-added goods, and the threat of a global trade war could be an outright negative for economic performance this year.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

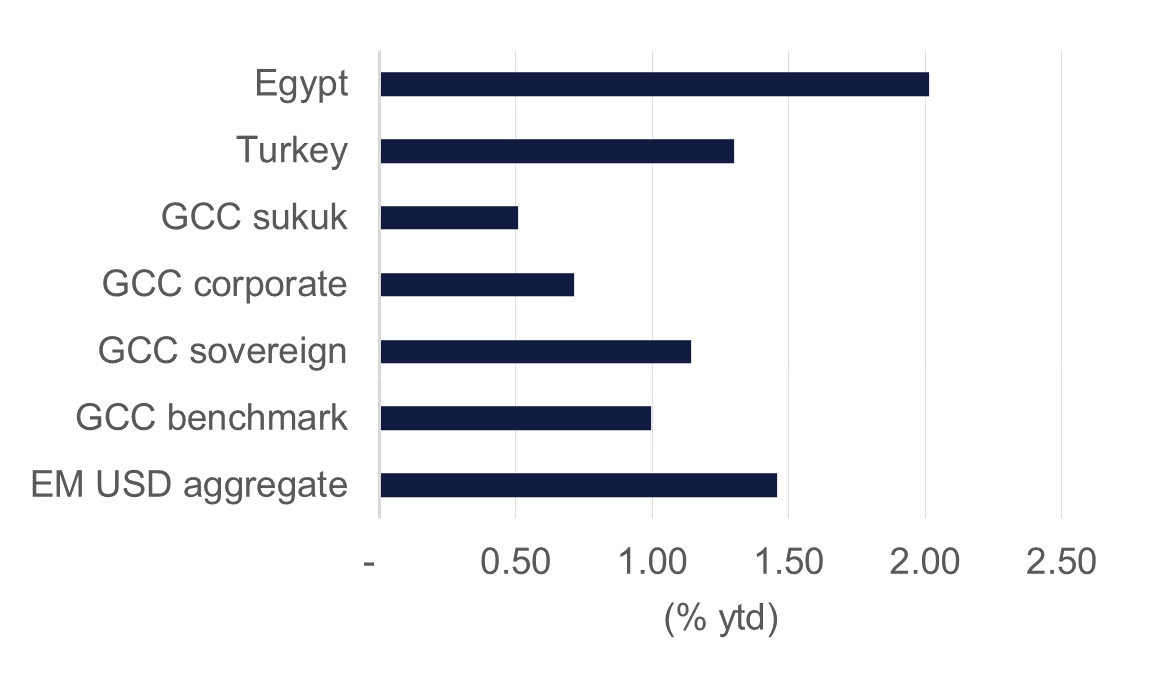

GCC bonds tracked the gain in the wider emerging market space with a 0.3% rise in GCC USD debt. At a sector breakdown, sovereigns were the strongest performer with a rise of 0.4% last week while sukuk lagged with a 0.2% gain. On a geographic basis the Qatar index was the strongest performer week/week with a gain of 0.4% while Saudi Arabia and the UAE had gains at slightly smaller levels.

Most of the gains were recorded earlier in the week as there was a broad sell-off in credit on Friday in response to the US nonfarm payrolls report. While headline job growth was slower than expected, a better unemployment and wage growth number trimmed market expectations of rate cuts from the Federal Reserve in 2025, hitting credit markets more generally.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

An index of Turkish USD bonds closed flat last week while Egyptian bonds were softer. Turkey’s central bank revised its inflation outlook higher for end of 2025 to 24% while noting that the disinflation in Turkey’s economy continues. TCMB governor Fatih Karhan said, however, that further rate cuts were not “on autopilot” following 500bps of easing since December last year.

Selected new issuances in the last week include:

Edward Bell

Edward Bell