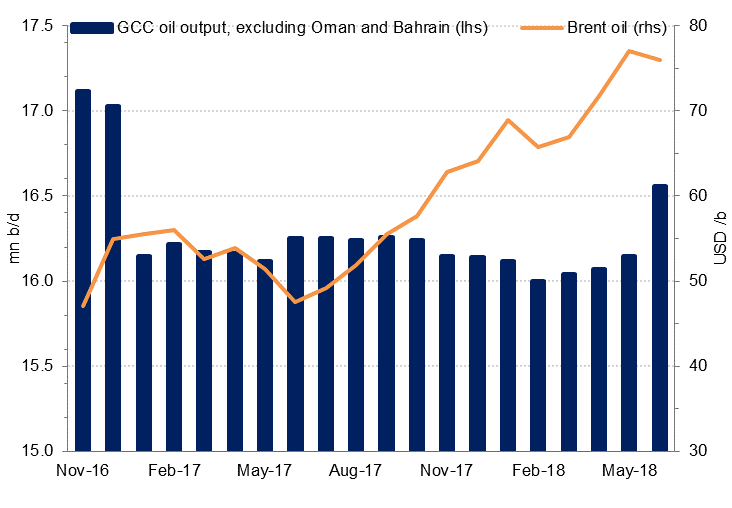

- OPEC has effectively brought its production cut deal to an end as unplanned outages have tightened markets more than anticipated. Looking toward the end of the year and into 2019 we expect oil markets will remain tight as inventories and spare capacity have been squeezed.

- After revising down our key GCC growth forecasts in May due to over-compliance with OPEC production targets, the decision by OPEC to boost output in H2 now poses an upside risk to headline GDP growth for the oil exporting countries, in particular Saudi Arabia which is the swing producer.

- Higher oil prices combined with increased output provide a double benefit to GCC budgets, reducing pressure on governments to push ahead with further expenditure reform while still allowing budget deficits (and borrowing requirements) to decline.

- Egypt’s macroeconomic stability continues to improve as the government has pursued economic reforms at the cost of more rapid real GDP growth. The twin deficits are narrowing, and while consumers and the private sector will remain under pressure from high inflation and tight monetary policy, the reforms could provide a more stable base upon which to build durable economic expansion over the next several years.

- Higher oil prices are feeding through to rising inflation in many MENA importers, compounding the squeeze on households already exerted by austerity programmes. Morocco, Jordan and Tunisia have all seen pushback on this issue in recent months.

GCC oil production starts to rise

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Daniel Richards

Daniel Richards