Recent Search

Popular Searches

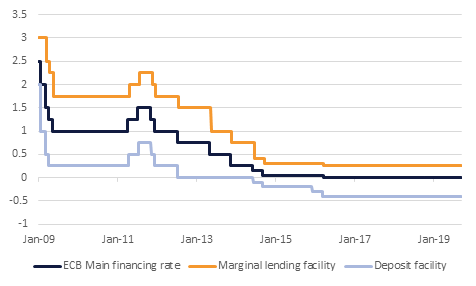

The main focus today will be the ECB policy meeting. While a rate cut from the ECB is widely expected, probably taking the deposit facility rate from -0.4% to -0.5%, the markets are split on whether the ECB will go further by extending asset purchases (QE) or taking some other measures. President Draghi had promised a comprehensive package, but there have been several ECB officials that have urged caution over the past month. Some suggestions are that there could be QE of around EUR20-30bn per month for 6 months. Other possibilities include the introduction of a tiering system for retail deposits in the banking system, to help soften the impact on banks from negative rates. Raising the issue limit from 33% to 50% is another option, but the ECB could also just announce the intention to do this without actually implementing it. Likewise, more specific forward guidance tying QE to quantifiable progress on inflation might also be seen. With Chancellor Merkel yesterday seemingly pouring cold water on the prospect of more fiscal stimulus from Germany, it is to be hoped that the ECB does move ahead with at least some of these measures. Most likely the ECB will only do one or two of them, leaving others for its next President Christine Lagarde to implement, and leaving markets in the process a little underwhelmed.

Perhaps mindful of what the ECB might do and the positive impact it may have on the dollar, Presdient Trump tweeted yesterday that the Fed should get interest rates down ‘to zero, or less’. The main apparent purpose of this idea, however, was a strange one, to reduce the financing costs of U.S. government debt. This suggestion generated scorn from a number of prominent economists given the likelihood that it would create more volatility, bubbles and may even cause long term interest rates to go up not down if it is not warranted by the economic fundamentals. On another issue however, there was more encouraging news from the U.S. Presdient with an announcement that the U.S. will postpone the imposition of some tariffs on China as a goodwill gesture to recognize the 70th anniversary of the People’s Republic of China. As its own goodwill gesture, the Chinese are also considering the purchase of US agricultural products.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Treasuries closed marginally lower as risk sentiment gathered ground. However, investors continue to remain cautious ahead of the ECB meeting later today. The expectation from the meeting continues to remain mixed in terms of the extent of policy easing. Yields on the 2y UST, 5y UST and 10y UST closed at 1.67% (flat), 1.59% (flat) and 1.73% (flat).

Regional bonds caught up with the moves in benchmark yields. The YTW on Bloomberg Barclays GCC Credit and High Yield index rose +4 bps to 3.14% and credit spreads widened +2 bps to 144 bps.

Bank of Sharjah raised USD 600mn in a 5-year issue which was priced at MS+250 bps.

The euro was Wednesday’s softest performing major currency, EURUSD finishing the day 0.30% lower at 1.1010. As we go to print, the price is almost unchanged with the cross trading at 1.1014 as the markets wait for the European Central Bank to set policy this afternoon. Should the central bank adopt a looser than expected policy, the euro is likely to find itself under pressure. However, should policy makers deliver the expected consensus, the single currency may rally.

Global markets closed higher on the back of strength in technology and banking stocks. The S&P 500 index and the Euro Stoxx 600 index added +0.7% and +0.9% respectively.

Regional markets closed mixed. It is worth noting that indices impacted by inclusion in the broader EM index still feeling the aftereffect of adjustment in fund flows. The Tadawul and the KWSE PM index lost -1.4% and -2.5% respectively.

Oil prices have been highly volatile on the back of mixed messages emanating from the Trump White House. The departure of Iran hawk John Bolton as National Security Advisor, alongside reports that President Trump is looking to meet with his Iranian counterpart Hassan Rouhani at the UN Assembly later this month, has raised fears over a glut of Iranian supply returning to market. This prompted Brent futures to close down 3.0% at USD 60.81/b yesterday, while WTI declined by a similar 2.9% to USD 55.75/b. However, news that President Trump is postponing the imposition of planned greater tariffs on China has been perceived as demand-positive, prompting both benchmarks to see gains this morning – Brent was up 0.7% at the time of writing.