Recent Search

Popular Searches

The European Central Bank kept rates unchanged at its first meeting of 2024, holding the deposit facility at 4% after 200bps of hikes in 2023. The ECB noted that the “declining trend in underlying inflation” is continuing while “tight financing conditions” are also helping to cool inflation. The bank said that risks to economic activity were “tilted to the downside” but gave a more balanced outlook on the risk to inflation in 2024. ECB president Christine Lagarde said that there was consensus in the ECB governing council that it was “premature” to begin discussing rate cuts and that she stood by comments made earlier in January that rates would move lower in the summer. Lagarde didn’t commit to a specific timing for rate cuts saying that the ECB would “continue to be data-dependent” rather than “date-dependent.”

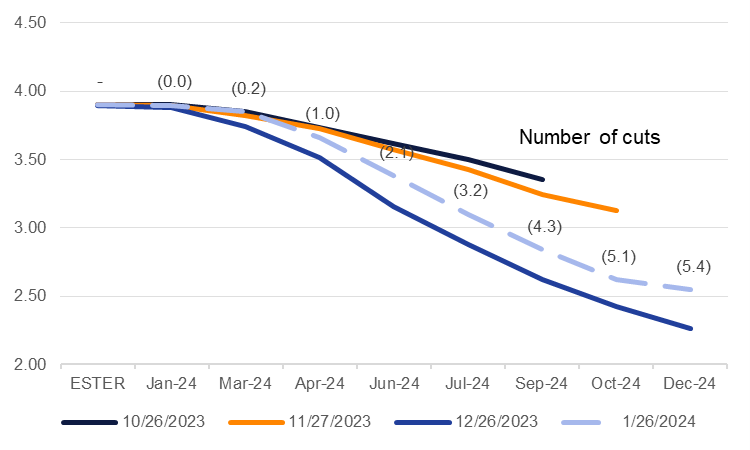

The apparent ECB timing for a cut in the summer is late compared with what markets currently expect. Market pricing for Eurozone rates have a more than 75% chance of a 25bps rate cut as early as April and more than five cuts in total for 2024, taking policy rates to roughly 2.5% by the end of the year. A cut as early as April has been consistently priced in for the last several months even as the ECB has stressed that it is waiting on wage data that will be released towards the end of Q1, leaving little time for assessment before potentially cutting rates on April 11.

Source: Bloomberg, Emirates NBD Research. Note: assumes increments of 25bps

Source: Bloomberg, Emirates NBD Research. Note: assumes increments of 25bps

Economic conditions in the Eurozone remain weak, suggesting that imminent rate cuts would be welcome. The composite PMI for the Eurozone hit 47.9 in January, actually its strongest print in the last six months, but still deeply in contraction territory. At a national level, all the large Eurozone economies are showing signs of weakness, according to near-term economic data while a preliminary estimate of Germany’s Q4 GDP showed the economy shrank by 0.3% q/q, barely missing a technical recession after Q3 GDP growth was revised up to 0%.

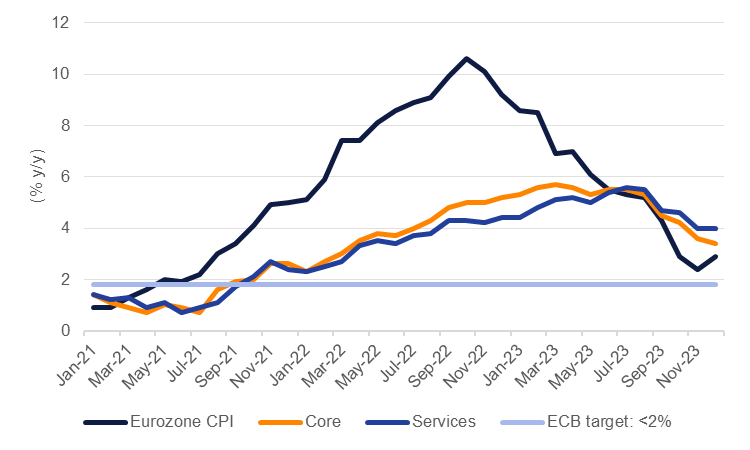

Headline inflation in the Eurozone is clearly showing a disinflationary trend, falling to 2.9% in December 2023 from more than 9% in December 2022 but while exogenous risks to inflation remain at play, such as interruptions to shipping from the Red Sea, central bankers may prefer to extend caution. Some inflation indicators from within the Eurozone also still have room to fall: headline services inflation remained steady at 4% y/y in December, showing a much smaller drop from peak levels of 5.6% in July 2023 than the drawdown in the headline index from its peak level.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The risk for a central bank like the ECB or indeed the Fed would be to cut while the risks to inflation are still balanced and then need to backtrack and have to hike rates again. We expect that central banks would prefer to maintain a steady trajectory when adjusting rates either on the way down or on the way up rather than trying to calibrate to near-term signals in the economy. That may mean a steeper trajectory when the ECB does begin to cut. As the economy does look set to drift this year we are adding in an additional cut from the ECB in H2 2024, taking rates down by 100bps starting from June.

Edward Bell

Edward Bell