Recent Search

Popular Searches

As the coronavirus outbreaks takes hold in more economies governments are taking drastic measures to contain its spread. Italy has put in place quarantines covering millions of people while countries in the GCC region are severly limiting cross-border travel. The collapse in confidence has eroded all risk-on market sentiment, sending equity futures and indices sharply lower in early trading and taking the UST curve to new lows. The entire US treasury curve is now sub 1% with the 10yr yield falling as much as 25bps in early trading this morning. Compounding the sense of panic in the markets was OPEC+’s failure to reach a production cut agreement last week with members now set to engage in a price war, an astonishing reversal and failure of oil market diplomacy. Brent futures are down more than 25% in opening trades today at USD 33.90/b.

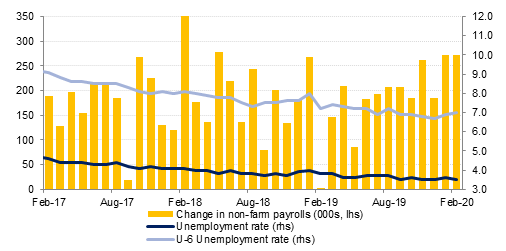

Jobs numbers in the US outperformed for February, with non-farm payrolls gaining by 273k and upward revisions to the prior two months.The unemployment report also improved, falling to 3.5% from 3.6% previously. Wage growth tempered to 3% y/y due to relatively high base effects from 2019. While the positive data was welcome and shows the US economy was in relatively good health, it reflects a period prior to Covid19 taking hold in the US and we would caution how positively markets should take the data. Data from March onward will show a much bigger impact from the coronavirus and may start to show signs of waning confidence, particularly around employment and wages.

China’s trade data weakened in January-February in line with expectations as the coronavirus ravaged the domestic economy. Exports fell by 17% in USD terms y/y and imports fell by 4% y/y. Domestic demand has plummeted in China and the drop in exports threatens supply chains globally. By all accounts given the Chinese authorities’ response to the viral outbreak, the import data could have been worse.

A statement from Lebanese Prime Minister Hassan Diab over the weekend confirmed that the USD 1.2bn Eurobond which matures today will not be repaid, as FX reserves have dropped to a ‘worrying and dangerous level.’ He also confirmed that Lebanon would be looking to restructure the rest of its debt, which has risen to around 170% of GDP. Lebanon’s already precarious financial position has come under increasing pressure from an ongoing political crisis which began in October.

Source: Bloomberg

Source: Bloomberg

Treasuries surged last week as risk assets came under renewed pressure. Further the decision of the Federal Reserve to cut interest rates by 50 bps also weighed on USTs. Investors shrugged off a strong non-farm payrolls report as market stresses and liquidity concerns took center-stage. Overall, yields on the 2y UST and 10y UST ended the week at 0.50% (-41 bps w-o-w) and 0.76% (38 bps w-o-w). Markets, at the end of last week, were pricing in an additional 50 bps cut by the Federal Reserve at its scheduled meeting on 18 March 2020.

Notwithstanding worries over impact of coronavirus on economic activity, the hunt for yield drove regional bonds higher. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped 22 bps w-o-w to 2.78% while credit spreads widened 15 bps to 207 bps.

Lebanon confirmed that it will default on the USD 1.2bn Eurobond and will seek talks with creditors to restructure its entire USD 90bn debt outstanding. Local banks hold almost USD 14bn of the debt outstanding. The formal debt restructuring talks with bondholders are expected to start in two weeks.

EURUSD rose for a third week, climbing by 2.34% to reach 1.1284. The price had managed to break the 1.13 level over the course of the week, for the first time since July 2019, before resistance at the 100-week and 200-week moving averages (1.1342 and 1.1348 respectively) halted any further gains. However, it is noteworthy that the price breached the 100-day moving average (1.10XX) and crossed the 1.12 level, which we indicated last week were crucial for further advancement. These technical developments mean that risks remain to the upside and although there may be some resistance by profit taking due to overbought positions, a daily close above the 76.4% one-year Fibonacci retracement would expose the 1.14 level to a test.

A 1.76% appreciation over the last week took GBPUSD to 1.3048, back above the 200-week moving average (1.3022) for the first time in four weeks. Over the course of the week, GBPUSD found support near the 50% one-year Fibonacci retracement (1.2736) on Monday. Following bids at this level, the price climbed for the next four days, breaching the 61.8% one-year Fibonacci retracement (1.2920) before breaking the 100-day and 50-day moving averages (1.2992 and 1.3017) in quick succession. Following these developments, technically upside risks seem the path of least resistance and we maintain our Q1 2020 forecast of 1.32.

Following a 3.13% decline the previous week, USDJPY added another 2.33% in losses over the last five days to close at 105.39. In line with our expectations, there was a daily close below 107.50, not far from the 38.2% one-year Fibonacci retracement (107.49) followed by a larger decline towards the 105 level at which support was found. Despite this, analysis of the daily candle chart shows that there is now a new level of resistance at the 23.6% one-year Fibonacci retracement (106.33) and while the price remains below this level, further losses seem the most likely fate for USDJPY.

Regional equities closed sharply lower as the inability of OPEC+ to reach an agreement on oil output cuts weighed on investor sentiment. The DFM index and the ADX index dropped -7.9% and -5.4% to close to multi-year lows. The KWSE PM index suspended trading after the index dropped -10.0%. Losses were widespread with no sector registering gains.

Oil prices are in complete free fall, falling more than 25% in both Brent and WTI futures. A retest of 2016 lows (USD 27.88/b in Brent) would seem highly likely given the start of a new price war between Russia and Saudi Arabia. Forward curves have collapsed while downside risk premiums have jumped.

Gold prices failed to capitalize on risk-off sentiment growth as investors drawdown on gold positions to cover equity and other risk asset margin calls. Further Fed action may be apparent in coming weeks that will add short-term catalysts for gold prices to move higher.