Recent Search

Popular Searches

China responded to the US limiting visas for officials earlier this week with a similar restriction against US nationals with “anti-China” links in the latest escalation of the trade war between the two countries. The level of rhetoric is becoming increasingly aggressive on either side, with direct targeting by Chinese consumers of cultural exchanges between the countries such as the NBA or US television programmes. Negotiations between China’s vice premier, Liu He, and US trade representative Robert Lighthizer and treasury secretary Steve Mnuchin are set to begin today but Chinese officials have downplayed expectation that a deal could be reached.

The minutes from the September FOMC meeting affirmed the division among policymakers at the US Federal Reserve when the board voted 7-3 in favour of cutting rates. The statement from the meeting showed the Fed did not expect “key uncertainties” to be resolved quickly and that trade wars, weak global economic conditions and elevated geopolitical risk would weigh on the outlook for the US economy. Markets are pricing in more than an 80% probability of another 25bps cut at the Fed’s October meeting while the odds of a hold or cut at the December meeting are closer to even.

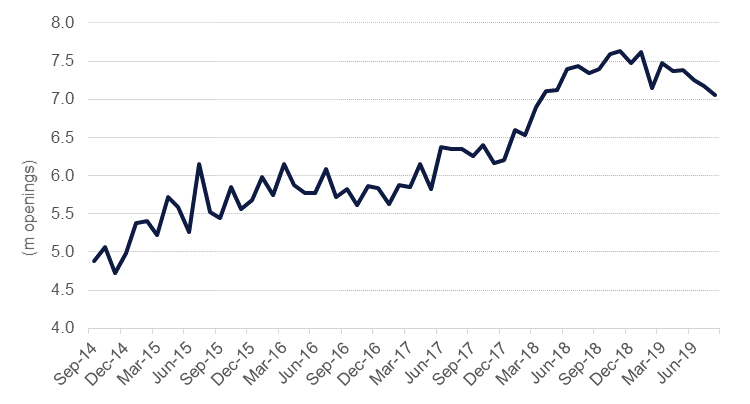

Job openings in the US fell in August, according to the JOLTS report, to 7.05m, their lowest level since March 2018. As the economy has hit more than full employment levels and the unemployment rate continues to drop a levelling off in job openings should be expected. Manufacturing, which has borne the brunt of the trade war-induced slowdown, saw the largest drop in vacancies. The quits rate also dipped as confidence in finding a new job is starting to ebb among workers in the US.

The UAE has ranked 25th globally in the World Economic Forum’s Global Competitiveness Index, an improvement of two places from its last ranking. The UAE scored particularly highly for macroeconomic stability given a modest inflation rate and what the WEF assessed as positive debt dynamics. The WEF also noted the country’s strong transport infrastructure, particularly ahead of Expo 2020. However, there is scope for improvement in human capital where the UAE ranked 92nd on health and 39th globally on skills.

Source: Eikon, Emirates NBD Research

Source: Eikon, Emirates NBD Research

Treasuries slipped as markets expected some breakthrough in trade negotiations between China and the US and thanks to a heavy amount of selling from the US treasury. However, as few signs of breakthrough are emerging, benchmark yields may reverse direction quickly. Yields on 10yr USTs gained nearly 5bps overnight while they have lost some ground in trading today. Likewise in Europe, initial optimism that a breakthrough on Brexit was pending helped push bund and gilt yields higher.

The USD was little changed after the FOMC minutes. The minutes revealed inflation as the main reason to cut rates, alongside the risks from trade tensions and global weakness, but there were also "several" who wanted the statement to have more clarity on when the easing would likely come to an end. The USD softened a little yesterday with losses stemming from the reversal of safe-haven flows following reports that China would consider a partial trade deal with the U.S. over a currency pact and a possible suspension of tariffs, with the AUD and NZD benefiting the most from such conjecture. Optimism about a Brexit deal meanwhile has seemingly evaporated bringing GBP off its recent highs above 1.23, although sentiment is coalescing around a likely Article 50 extension which would take the next deadline to January 31st, and leave GBP in limbo.

Equity markets gained overnight, snapping a few days of losses, on the hopes that a trade deal could be achieved between China and the US. The S&P 500 rose 0.9% while the Dax added more than 1%. Chinese equities are trading higher this morning although they are likely to be highly vulnerable to any negative trade headlines that emerge later in the day.

Regional equity markets were mored mixed with a sharp sell-off in the Tadawul (down almost 1.5%) but a gain on the DFM of 0.5% and a drop in the ADX of 0.3%.

As sentiment broadly is pessimistic on the chances for a US-China trade deal, commodity prices continue to suffer. Oil markets are down this morning by around 0.3% in both Brent and WTI while key base metals have been trending lower since the start of October. EIA data for the US showed inventories rose nearly 3m bbl last week although there were some decent draws in gasoline and distillates. Refinery demand continues to dip, however, well off seasonal trends.

The standout numbers from the weekly EIA numbers, however, are production which rose by 200k b/d to a record high of 12.6m b/d last week and exports, rising to more than 3.4m b/d. US production has risen 1.4m b/d since the same time last year and is up 900k b/d since the start of the year alone. Projections earlier in the week from the EIA showed they expected output of more than 13m b/d next year. The jump in crude exports has also helped push net US imports of crude to near record lows, just 2.8m b/d last week. Most of those imports are met by supplies from Canada, leaving Middle East exporters to push crude in other markets.

Nigeria has received a higher output target under the terms of the OPEC+ production cut deal. The country can now produce at 1.774m b/d, compared with 1.685m b/d previously. Nigeria has recorded very poor compliance with its target and its current production of around 1.9m b/d means it will remain non-compliant even with the new higher target.

Edward Bell

Edward Bell