Recent Search

Popular Searches

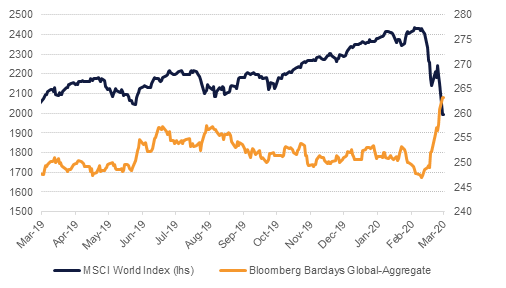

Markets remain fragile after a brutal sell-off to start the week. Equity indices globally tanked with the MSCI global index falling more than 7% while benchmark government bond yields collapsed: 10yr UST yields fell 22bps to settle at 0.54%. Fears that the coronavirus outbreak will translate into a global recession have taken hold of markets and without substantial coordinated response from governments around the world, it’s challenging to see how the demand shock caused by interruptions to normal business and consumer behavior doesn’t turn into a global slump. Oil markets, where a price war between Saudi Arabia and Russia further eroded confidence, ended the day down more than 24% in both Brent and WTI futures while gold only gained 0.4%.

Emergency relief overnight came in the form of the US Federal Reserve opening the repo taps wider, injecting USD 150bn in overnight cash to the banking system, up from USD 100bn previously. Unlike the global financial crisis which was catalyzed by severe dysfunctions in the banking system this market crash is a result of substantial demand destruction. A seizure of financing at the same time would likely guarantee a prolonged, and painful, downturn. Markets continue to price in further interest rate cuts by the Fed at their meeting next week, which would take benchmark rates essentially down to 0. With government bond yields falling to record lows—10yr gilt yields in the UK tumbled to just 0.15% while bunds fell to almost -0.9% and whole of the US yield curve is below 1%—there is ample room for governments to borrow cheaply and help inject funds into troubled economies. So far there hasn’t been a wholesale endorsement of wide-ranging fiscal stimulus: in the US, president Donald Trump was looking at a payroll tax cut to help offset the impact of the virus on the US economy while both Australia and Canada were examining targeted stimulus.

With markets driven more by panic positioning, economic data is fizzling out like spraying a water pistol on a house-fire. Germany showed some signs of positivity in January as industrial production rose by 3% in January. However, like any data from the start of the year, the positive news from Germany should be viewed with a large caveat given it pre-dates the impact of the coronavirus on Europe’s economy. Germany has not taken the extensive steps that other countries in Europe have—Italy’s government is attempting to lockdown the entire country—but its economy will not be immune to the slowdown in industrial demand.

Source: Bloomberg

Source: Bloomberg

Treasuries extended their rally as risk assets sold off extensively. Market is now pricing in a 75 bps rate cut by the Federal Reserve at its scheduled meeting next week. The curve shifted lower with yields on USTs across tenor yielding below 1%.

Regional bonds saw sharp sell-off as investors turned cautious following moves in oil and broader markets. The YTW on Bloomberg Barclays GCC Credit and High Yield index rose 33 bps to 3.12% and credit spreads widened 49 bps to 256 bps.

The USD weakened sharply yesterday as risk aversion increased and anticipation of lower Fed interest rates undermined the US currency. Risk-off sentiment intensified as coronavirus risks rose and oil prices plunged, hurting global equities and treasury yields. USDJPY hit an intraday low of 101.19 before steadily recovering over the rest of the day. EURUSD reached heights of 1.495, its highest point since February 2019, also helped by news that German industrial production m/m performed much better than expected. However, with the German 30y yields dropping, EURUSD came off the highs.

GBPUSD also saw a sharp rally, reaching highs of 1.3201. It also stalled however as UK bond yields fell. AUDUSD and NZDUSD both suffered through some dramatic losses in the early hours of Monday, due to panic surrounding the coronavirus. With markets in Asia improving slightly this morning the USD is also faring better against other major currencies with USDJPY back above 103 now, and EUR below 114.

Developed market had one of their worst trading days since the 2008 financial crisis. The immediate trigger was the collapse in oil prices. The S&P 500 index and the Euro Stoxx 600 index dropped -7.6% and -7.4% respectively.

Regional markets were no different. The KWSE PM index closed limit down for a second consecutive trading session. The DFM index and the Tadawul dropped -8.3% and -7.8% respectively. Banking and petrochemical stocks led the decline.

Oil markets recorded their single largest daily decline since 1991 with both Brent and WTI futures falling by more than 24%. The price war between Saudi Arabia and Russia has taken a toll on global financial markets, sparking a collapse in assets world wide and threatening to destroy much of the US’s shale producers. With both countries planning to increase production substantially and promoting how long they can endure low prices—Russia’s finance ministry said the country can endure low prices for six to ten years—oil markets will remain highly volatile with substantial downside risks.

Forward curves wree brutalized as markets price in an overwhelming volume of crude given poor demand conditons. Time spreads at the front of the Brent curve settled yesterday at USD 0.74/b while Dec spreads in both Brent and WTI for 2020/21 moved to more than USD 5/b in contango.

The IEA cut its expectation for oil demand growth in 2020 to a contraction of 90k b/d as the impact of the coronavirus outbreak spreads across the world. While a sharp revision from the slow pace of growth it was initially projecting in February, the IEA’s expectation is still far above some private sector forecasters. The agency did note in a downside scenario that demand could drop by 730k b/d y/y if the coronavirus entrenches in Europe and North America.

Aditya Pugalia

Aditya Pugalia