Recent Search

Popular Searches

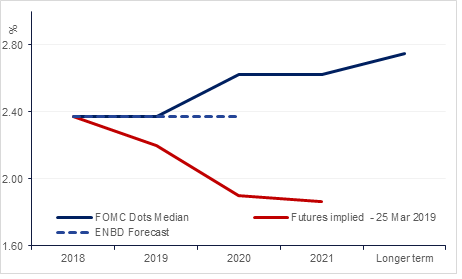

US Treasuries surged on heavy volumes last week with yields dropping by 10-15bps across the curve. Following the unexpectedly dovish statement and the revised dot plot released after the conclusion of last week’s FOMC meeting, yield on 10yr USTs dropped 15bps to 2.43% - its biggest weekly drop since mid-2016. USD swap spreads tightened into Treasuries rally, with 10- and 30-year reaching multi-month lows. The extreme dovish shift in the front-end left the OIS pricing in 20bps of cut for this year and another 30bbp cuts by 4Q 2020. The 2yr5yr curve that had spent most of this year in flat to slightly negative territory has now become decidedly inverted. Against this backdrop we take a closer look at the path of interest rates going forward.

Fed watch

As expected, the FOMC left rates unchanged at its meeting last week and revised its growth forecasts down for this year and next. The ‘dot plot’, shows the median expectation is now for no rate increases in 2019, compared with expectations for two hikes as of last December. This revised path reflects the ‘patient’ stance adopted at the January FOMC and reiterate the Fed’s data-dependent reactive rather than proactive stance.

There is a forecast of one rate hike in 2020 that we think will not happen given that the bar for further tightening is clearly high and we think unlikely to be met. We do not see any catalyst that could either provide a strong boost to economic growth or a substantial pick-up in inflation from the current levels.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Click here to Download Full article