Recent Search

Popular Searches

Base metals prices have had a fairly resilient start to the second half of 2023 despite the substantial uncertainty over near-term conditions in major economies like China, the US and Eurozone. Copper prices ended H1 at USD 8,315.50/tonne, down marginally since the start of the year, but they have now stabilized and managed to trend higher in July. The gains in copper prices have helped to temper losses for the broader LME base metals complex, with the LMEX index of the six non-ferrous metals shaving its year-to-date losses to less than 5% as of early August, from more than 7% as of the end of H2. But while prices have managed to hold up for now, the outlook for the rest of the year is for more sideways price moves.

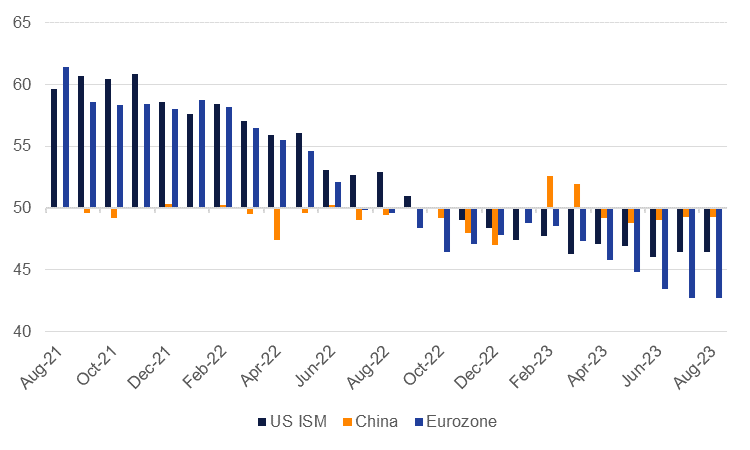

Headline macro indicators for industrial metals are poor. Manufacturing PMIs across major economies have all pushed below 50 for nearly all of 2023. The ISM manufacturing index for the US printed at 46.4 for July while the official China manufacturing PMI edged marginally higher to 49.3 last month, representing its fourth month in a row in contraction territory. Eurozone manufacturing PMIs have been negative since July 2022. Beyond the major economies, sizeable emerging economies like South Korea, Turkey and Taiwan are all recording lingering manufacturing activity. Anxiety over whether tightening from developed market central banks will prompt a recession will also act as a dampener on commodity prices.

Source: Bloomberg, S&P Global, Emirates NBD Research

Source: Bloomberg, S&P Global, Emirates NBD Research

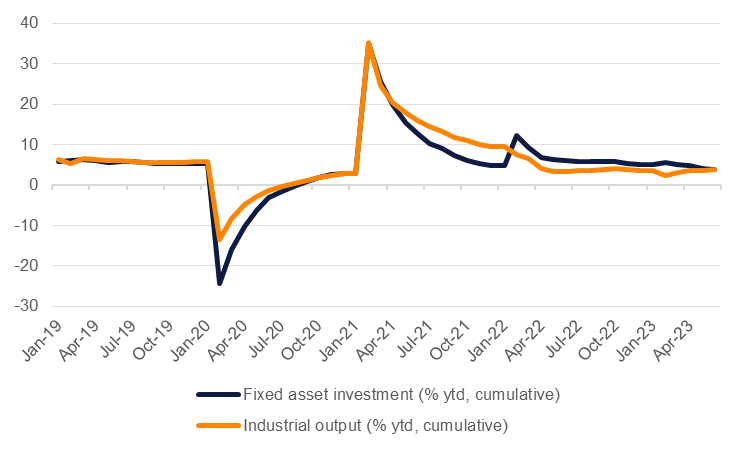

The most critical variable remains China. Headline economic activity has disappointed markets since the country ended its strict Covid-19 restrictions at the end of last year. Industrial production was up just 3.8% ytd in the first half of 2023 compared with H1 2022 while property spending has slowed substantially. Commodity imports have told a mixed story on China’s economy this year. Energy imports have so far been strong: crude oil imports are up 12.5% in the first seven months of the year compared with the same period in 2022 while refined product imports in the same period were more than 104% higher. Coal imports were almost 90% higher while total gas imports (LNG and piped gas) have risen by almost 8% in the first seven months of 2023 compared with the same period in 2022.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

But metals imports have more moderate. Imports of copper products fell nearly 11% ytd in the first seven months of the year while imports of copper ore have also slowed. Iron ore imports have managed to stay positive so far this year, up 6.8% ytd, but steel output has been lingering in recent weeks and provide only limited demand in the months to come.

China’s government has pledged to support the economy but largely through indirect means to support confidence and domestic consumption. Substantial debt burdens in the property sector will likely make the government wary of trying to invest its way out of the moderate growth through construction. That hesitancy, combined with lacklustre industrial activity globally will act as a lid on base metals price for much of the remainder of the year.

Edward Bell

Edward Bell