Recent Search

Popular Searches

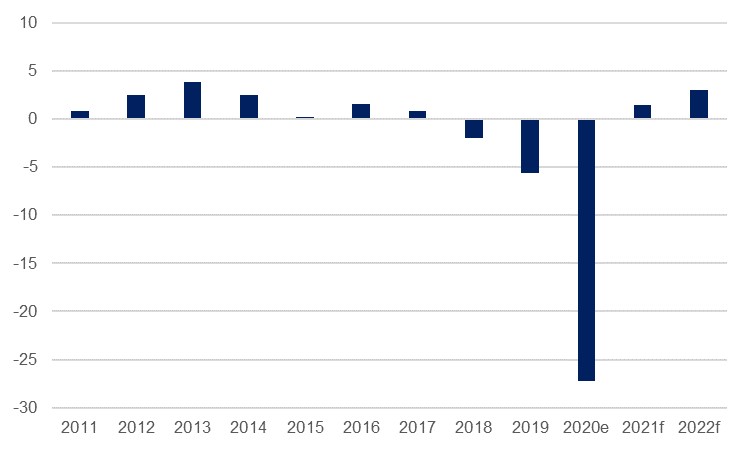

Lebanon will likely have a better year in 2021 than it had in 2020, when it was already dealing with crises on multiple fronts even before the coronavirus pandemic and then the Beirut blast in August dealt further blows. However, that is not to say that we expect a resounding rebound, and the 1.4% real GDP growth we project will do little to make up for the -27.3% contraction we estimate last year – and even then the risks are to the downside. Household spending power is being eroded by surging inflation, extended lockdowns will further curb activity, and the ongoing political impasse makes the prospect of imminent assistance from the IMF or Paris Club lenders unlikely.

A number of timely indicators demonstrate the immense pressures on the Lebanese economy in 2020, and given that we expect little improvement over the first half of 2021 at least, it is only base effects that make us more positive regarding Lebanon’s growth prospects this year. Over January to September last year, Lebanon’s coincident indicator averaged a year/year decline of -38.3%, with the third quarter the worst at an average -48.3%. Construction permits averaged a y/y decline of -29.5% over the same three-quarter period, cement deliveries -48.8%, while the PMI survey averaged just 41.0, substantially below the neutral 50.0 level which delineates expansion and contraction.

Source: UN, Emirates NBD Research

Source: UN, Emirates NBD Research

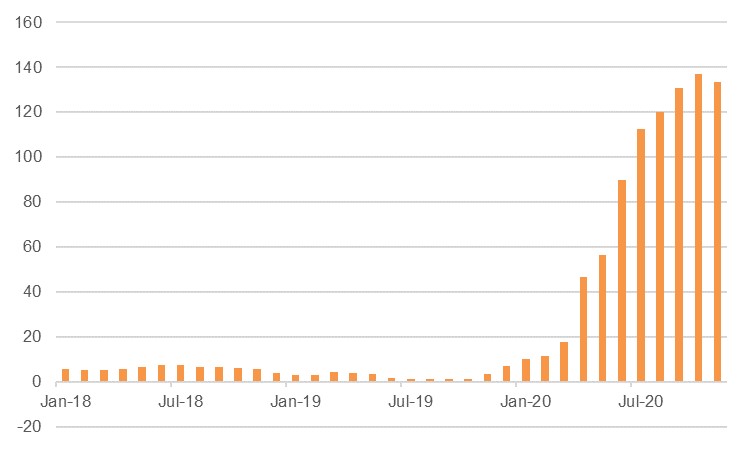

As 2020 began, Lebanon was already dealing with the fallout of its financial crisis as its financial engineering reached its limits in the face of diminishing overseas deposits, forcing the country’s first default on its international debt in March. There followed a rapid depreciation in the Lebanese pound, which fell from the LBP 1,507/USD at which it had been held for decades, to as little as LBP 8,000/USD later in the year on the parallel market. While Banque du Liban governor Riad Salameh has acknowledged that the peg’s days are finished, he maintains that it will be up to discussions between the IMF and the government as to whether it is floated. In any case, to all intents and purposes the currency is worth a fraction of what it was previously, and Lebanon’s high levels of inflation are testament to this.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Price growth in Lebanon averaged 78.7% y/y over January to November, with an average of 126.8% over H2 so far. The impact of the pound’s collapse will have been further compounded by disruptions to logistics operations caused first by the coronavirus pandemic, and then more specifically by the Beirut port blast. This has had a highly negative effect on households’ spending power as real wages have been slashed, a trend unlikely to reverse over the next several years. Meanwhile, ongoing lockdowns related to the coronavirus pandemic have further weighed on private consumption, and will continue to do so in 2021; in late January, Lebanon extended the total lockdown which began on January 14 to run for another two weeks until February 8. The hospitality and tourism sectors will continue to struggle through the year.

Given the parlous state of Lebanon’s circumstances, hope for a recovery rests on significant external support helping the country through its time of need, but the likelihood of this materialising remains a distant prospect at the start of 2021. Lebanon turned to the IMF for the first time in May, but as the Fund’s communications director acknowledged in a January press conference, there has been little to say about the progress since. Previous incumbent Saad al-Hariri was made prime minister designate in October after Mustapha Adib’s short-lived efforts to form a cabinet, but Hariri has also so far failed to form a working government, with a dispute with President Michel Aoun spilling into the public in January.

Lebanon needs a strong and stable government to implement the reforms called for by both the IMF and the Paris Club lenders as prerequisites for the billions of dollars potentially available for its support (CEDRE lending pledged in Paris in 2018 came to over USD 11bn, while Prime Minister Hassan Diab initially approached the IMF for USD 10bn). However, as things stand, the prospect of a government reforming the energy sector or government subsidies appears dim. Further, the audit of the BdL’s books demanded by countries such as France before any aid will be given has been mired in controversy. Alvarez & Marshal halted their work in November, stating that they had not been provided with all the information they needed to proceed. In January it looks possible that the firm might resume its work, but a Swiss investigation into the central bank – the charges are denied by Salameh – could further complicate matters, and push the prospect of aid for Lebanon back further.

Daniel Richards

Daniel Richards