Recent Search

Popular Searches

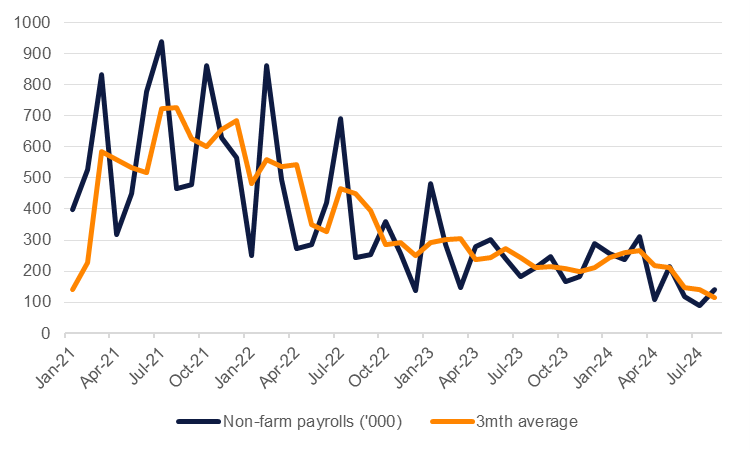

The August non-farm payrolls report from the US gave no clear sign to markets on whether the Federal Reserve will start its rate cutting cycle with a 25bps or 50bps cut at the September 17-18 FOMC meeting. A total of 142k jobs were added in August according to the data, up from the 89k that had been added in July though that figure was revised lower from its initial estimate. Headline job growth also missed market expectations of more than 150k jobs to have been added. At the same time average hourly earnings accelerated in August to 0.4% m/m, up from 0.2% a month earlier.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The unemployment rate moderated slightly, falling to 4.2% in August from 4.3% a month earlier, alleviating worries of another material increase. Unemployment is being maintained by a stable labour force participation rate—62.7% in August, unchanged m/m and up marginally from 62.5% at the start of the year—a better outcome than being caused by layoffs or workers voluntarily leaving the labour force. However, the headline unemployment rate has triggered the Sahm rule, a market observation that tracks whether the rolling three-month average of the unemployment rate is 0.5% or more higher than the lowest three-month average of the prior 12 months. The Sahm rule is used as a barometer of whether the US economy is in or on the verge of recession.

The labour market data was highly anticipated to provide markets with a clue as to whether the Fed will need to cut by 25bps or 50bps but failed to provide a strong signal in either direction. Following the release of the data, Fed governor Christopher Waller emphasized the Fed’s focus on employment data and said that the latest data “no longer requires patience, it requires action.” Governor Waller also noted that the jobs numbers continue to “soften by not deteriorate” and that he was “open-minded about the size and pace of cuts.” Market pricing for Fed cuts by the end of the year remains at slightly more than 100bps after the NFP data, essentially unchanged on where it had been ahead of the release.

Taking the US economic data in aggregate—employment, inflation, activity—it is clear the economy is slowing. The Atlanta Fed’s GDPNow forecast has growth pegged at slightly more than 2% (SAAR) as of early September, slower than 3% estimated a month earlier and down from 4% estimated for Q2. However, the series is noisy and has under- and over-estimated activity more frequently than provided accurate readings. The choices for the Fed are whether to try and get ahead of a potential recession and cut rates aggressively or to take a more gradual path and try to calibrate rates with slower growth and avoid an excessive deterioration in the labour market. The risks for further easing have increased though we still think that would come in the form of one additional 25bps cut this year (on top of the two 25bps cuts that form our baseline) rather than an emergency need for a larger move.

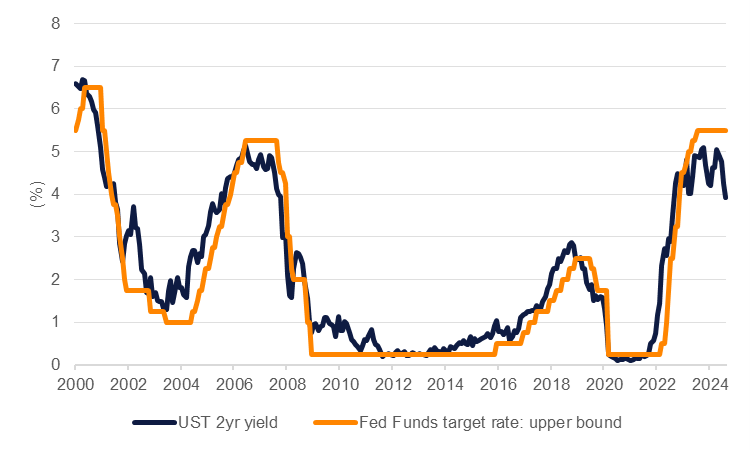

The Fed is now in a blackout period ahead of the FOMC meeting, setting markets up for more volatility around the release of the August CPI inflation report (Sept 11, forecast 2.6%). In the immediate aftermath of the jobs data the 2yr UST traded in a choppy way and ended the day lower by almost 10bps at 3.6462% while the 10yr also had wide intra-day moves but closed the day near unchanged at 3.708%. That has helped to steepen the US yield curve and allowed it to re-normalize after being inverted since the middle of 2022. The steepening has been driven by the sharp drop in 2yr UST yields since the end of Q2, down 100bps as of mid-September.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The US dollar also remains under pressure on expectations that the Fed will cut rates at a faster and steeper pace than peer central banks. The European Central Bank is expected to cut rates by another 25bps when it meets this week but market projections for the ECB are for a bit more than six 25bps cuts by mid-2025 compared with nine priced in for the Fed. The Bank of England meets after the Fed this month but cuts are only priced in at the next MPC meeting in November and just five cuts are priced in by the end of summer 2025.

Edward Bell

Edward Bell