Recent Search

Popular Searches

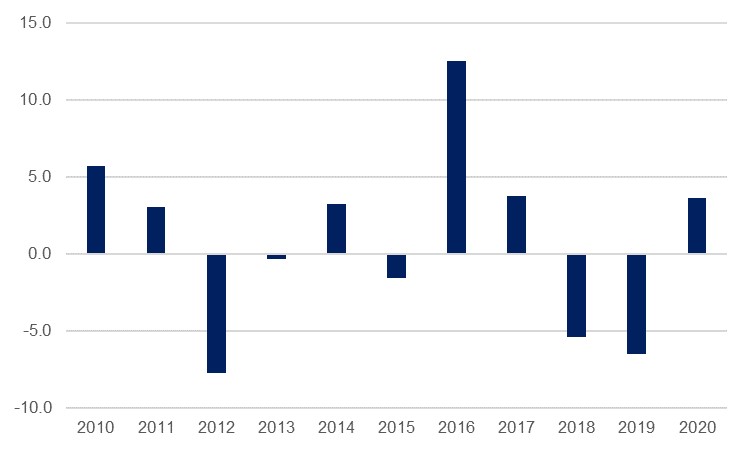

The outlook for the Iranian economy this year hinges strongly on two variables: the negotiations around reinstating the JCPOA nuclear deal, which could provide a boost to the oil economy, and the ongoing struggle against the Covid-19 pandemic. At the time of writing at the start of July the prospects for the oil economy in the second half of the year look more positive than that of the non-oil economy, but there remain salient uncertainties on both fronts. Both pillars of the economy managed to secure positive real GDP growth in the fiscal year ended in March despite the myriad challenges, leading to a headline expansion of 3.6% according to central bank data compiled by Haver Analytics. In calendar 2020 growth was a more muted 0.2%. In calendar 2021 we forecast growth of 3.9%, with the first quarter already in at 6.7%.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

The change of resident in the US White House at start of 2021 has led to the prospect of sanctions on Iranian crude oil exports being lifted as the Biden administration has re-engaged with negotiations around the JCPOA, the nuclear deal initially signed off on while Biden was vice-president under Barack Obama. President Trump had unilaterally removed the US from the deal and imposed fresh sanctions on Iran, leading the country into three consecutive years of economic contraction from 2017-2019. While there has also been a change at the top in Iran in recent weeks, incoming President Ebrahim Raisi is also ostensibly committed to renewing the agreement, although he has said that it is not at the top of his priorities.

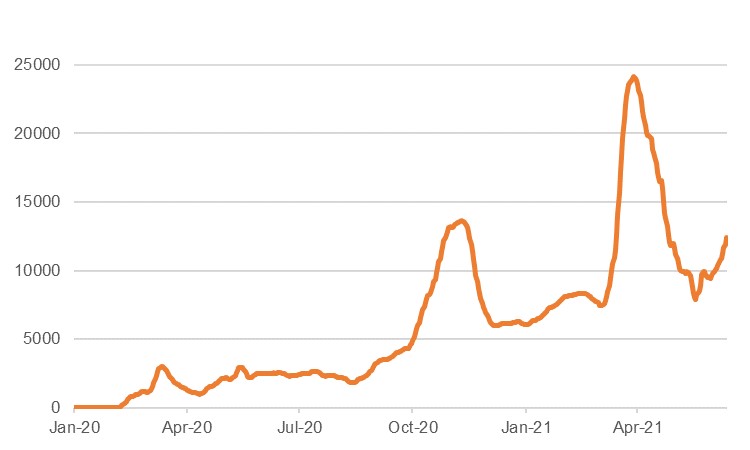

For now there has been little concrete progress on the renewed talks, and they have entered into apparent ‘final’ weeks of discussions several times. Even were oil sanctions on Iran suddenly lifted, there are several questions around how quickly exports would return. Outgoing oil minister Bijan Namdar Zanganeh has said that Iranian crude production can be ramped up quickly to as much as 6mn b/d, but this appears very unlikely given issues over OPEC+ production curbs, regaining market share amongst customers who have been burnt before, and potentially dilapidated infrastructure as IOCs have been prevented from investing in Iran for several years. Nevertheless, both sides are still at the table, and a deal either towards the end of 2021 or in 2022 still seems possible, which would pave the way for an ongoing increase in Iranian oil production, and in the oil economy. Production has already surged by around 25% to 2.49mn b/d since the end of last year, and we anticipate a gradual return to continue.

.jpg) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

While the proportion of the oil sector in Iran’s economy has shrunk considerably over recent years – to just 5.3% in 2020 – as sanctions have bit and the authorities have pursued the ‘resistance economy,’ it nevertheless retains importance given its role in FX inflows through exports and inward investment. A recovery in the sector, even if not as large as it used to be – over 20% of the total economy a decade ago – helps elevate the economy as a whole. The oil economy grew 11.2% in fiscal 2020/21 as it expanded 35.8% y/y in Q1 2021, and we expect it will continue to support growth in the current fiscal year.

The non-oil economy is facing its own challenges at present, as there has been a renewed surge in Covid-19 case numbers in recent weeks which has led to renewed restrictions on movement and activity being imposed. Outgoing President Hassan Rouhani has warned of a fifth wave as the Delta variant has spread, and at the start of July the order was given to close non-essential businesses in cities across the country. This will weigh on the recovery from the pandemic in Iran, which was one of the first countries to struggle with significant case numbers and has been one of the worst affected in the region. Private consumption fell -0.4% in 2020, with an average inflation rate of 35.9% also affecting demand – although this was less pronounced than the -7.7% contraction in 2019.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

However, while Iran was hit hard by the pandemic, several years of contraction prior to the arrival of Covid-19 meant that non-oil GDP had less far to fall in comparison to some of its regional peers, and the non-oil sector actually expanded by 2.5% last fiscal year. The collapse of the currency as sanctions were imposed led to increased competitiveness, and non-oil exports performed well. Manufacturing and mining grew 7.8% last year. With imports curtailed by diminished spending power on the other end of the equation, net exports rose by 1.7% on the GDP by expenditure side, while investment rose 2.5%.

The trajectory of the non-oil sector will depend in large part on how effectively the current virus threat is dealt with. Only around 2% of the population has been vaccinated so far meaning that a rapid surge in cases could necessitate a protracted and strict lockdown that will hamper the economic recovery. Nevertheless, with inflation set to come in lower this year as the currency has rebounded considerably, household spending power should be moderately supported compared to the erosion of wages seen over the preceding several years.

Daniel Richards

Daniel Richards