Recent Search

Popular Searches

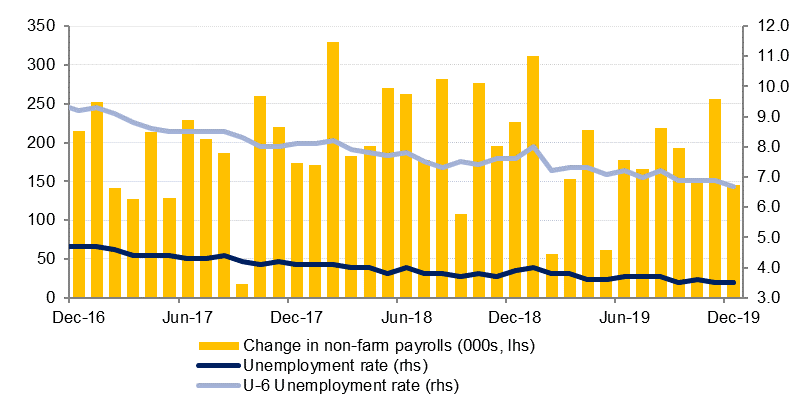

After a week dominated by geopolitics, this period is perhaps coming to an end for the time being and the coming one should be back to basics with market direction once again being set by economic fundamentals. U.S.non-farm payrolls rose by just 145,000 last month, and while the unemployment rate remained at 3.5%, wages grew by only 2.9% y/y, the slowest pace since 2018. For policy makers at the Fed, the message from the employment report was that while the labour market remains tight, it is still not tight enough to put upward pressure on earnings. This is likely to reinforce the message from the minutes from the Fed’s December meeting which displayed a dovish consensus to keep rates steady for 2020.

Oman's Sultan Qaboos passed away over the weekend, reportedly after a lengthy illness. His cousin, Haitham bin Tariq Al Said was nominated by Sultan Qaboos as his successor and has been sworn in as the new ruler. Sultan Haitham had served as minister of culture and heritage, and has indicated that we will continue Oman's policy of neutrality on foreign policy. It remains to be seen whether the new ruler will make significant changes to Oman's economic or fiscal policy.

The Dubai PMI eased further to 52.3 in December from 53.5 in November, the lowest reading since August. While output increased at a slightly faster rate in December, new order growth slowed, with the latter index falling to the lowest level since February 2016. Employment in Dubai’s private sector was also broadly unchanged at the end of last year, after increasing slightly in October and November. Firms continued to discount selling prices in December, despite rising input costs.

Egyptian CPI inflation ticked up to 7.1% y/y in December, compared to just 3.6% in November, as previously favourable base effects eased. Nevertheless, price growth remains well within the CBE’s target range (9% +/- 3 by the end of the year). On a m/m basis, inflation was -0.2%. The CBE’s monetary policy committee is set to meet this week, and while further monetary easing this year is all but guaranteed, the significant rise in inflation last month could swing the body towards adopting a wait-and-see approach for the time being – the postponement of this meeting from December 26 to January 16 may well have been implemented with this in mind. If there is a cut it is more likely to be 50bps compared to the 100bps reductions we have seen recently. In any case, we retain our outlook for around 200bps of cuts in total this year from the 12.25% the overnight deposit rate currently stands at.

Source: Emirates NBD Research

Source: Emirates NBD Research

It was a choppy week for US treasuries as geopolitical tensions at the start of the week and economic data (non-farm payrolls) at the end of the week weighed on investor sentiment. Over the course of the week, Treasuries closed lower with yields on the 2y UST and 10y UST closing at 1.57% (+5 bps w-o-w) and 1.82% (+4 bps w-o-w) respectively.

Regional bonds ended the week largely unchanged as investors remained cautious in light of hostility between the US and Iran. The YTW on Bloomberg Barclays GCC Credit and High Yield index was flat w-o-w at 3.18% and credit spreads tightened 3 bps to 144 bps.

According to reports, Lebanon Central Bank wants local holders of a USD 1.2bn Eurobond maturing in March 2020 to swap into new notes as part of a debt restructuring. The governor was also quoted as saying that no decision has been taken and will be dependent on the consent of Lebanese banks.

Last week’s decline of 0.36% resulted in EURUSD closing the week at 1.1121. This was the second week that the price declined. However, the most significant development is the failure to sustain the break above the 50-week moving average (1.1174). The price has not seen a weekly close above this level since May 2018. While the price stays below this level, downside pressures will persist. We expect the next level of support to be the 50-day moving average (1.1091), a level which prevented further declines over the previous week. Should this level falter, the 100-day moving average (1.1065) can expect to be tested in quick succession. On the other hand a break of the 50-week moving average will be bullish for the price and may result in further gains, initially towards the 50% one-year Fibonacci retracement (1.1197).

Last week, GBPUSD fell for the first time in three weeks, with a 0.21% decline taking the price to 1.3064. Of note is that while the price did close below the 200-week moving average (1.3074), it found support at the 100-week moving average (1.3011). In addition to this, analysis of the daily candle chart shows that the price has remained in an uptrend since August 2018. Therefore while the price remains above 1.3010, a level also not far from the 50-day moving average (1.3016), we expect the path of least resistance to be further gains for GBPUSD. A break above the 200-week moving average would be likely to result in a retest of the 76.4% one-year Fibonacci retracement (1.3147). Should this level also be penetrated, it could catalyze a more significant rise towards the 1.35 level.

Regional equities closed marginally higher to start the new week on a positive note. However, the trading was rather dull with most stocks closing largely unchanged.

The geopolitical spark that pushed Brent oil futures above USD 70/b snuffed itself out quickly as it became apparent that an escalation of tension had no impact on oil market fundamentals or flows of physical crude from the Middle East. Brent futures fell more than 5% last week to settle below USD 65/b while WTI dropped nearly 6.4% and closed at USD 59.04/b. The decline last week was the first weekly decline in the past six weeks and only the second weekly drop in the last 10.

As benchmark futures declined, so did market structures. The backwardation at the front of the Brent and WTI curves weakened substantially. In WTI, the front of the curve is barely holding in backwardation (just USD 0.05/b on the 1-2 month spread) while in Brent the spread closed the week at USD 0.73/b. Longer-dated spreads also shrank with Dec spreads for 20/21 in both Brent and WTI moving below USD 3/b after having started the week wider than USD 4/b.