Recent Search

Popular Searches

Fed chair Jerome Powell’s speech at the Jackson Hole symposium asserted that the Fed isn’t ready to sit on the sidelines as inflation is slowing. Chair Powell made it clear from the start of his commentary that inflation “remains too high” and the Fed would raise rates if needed. He showed no indication of the Fed moving away from its 2% inflation target while also acknowledging some dynamics—like a drop in job openings but no uptick in unemployment—as “historically unusual.” Powell also said the Fed “cannot identify with certainty the neutral rate of interest,” a level where rates neither stimulate or restrict the economy and a topic that where some market participants had expected the speech to focus.

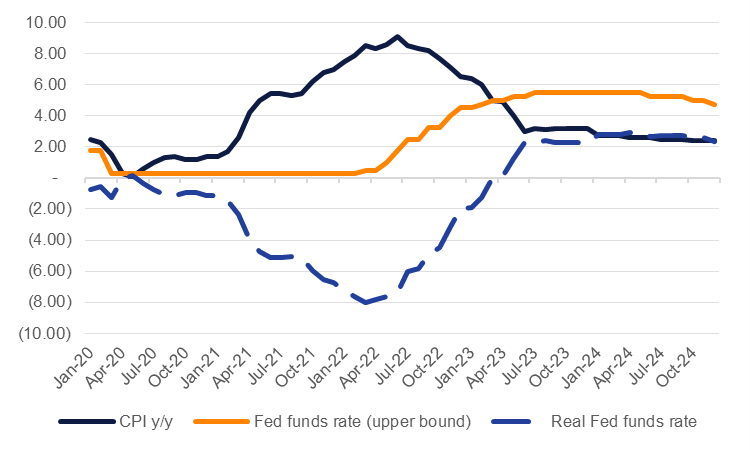

Powell described the current policy stance as restrictive and that it should put “downward pressure on economic activity.” So far, the US economy has held up relatively well with the labour market showing no substantial signs of distress and economic activity slowing but not at an alarming pace. If that reflects the degree of tightening the Fed has taken so far passing into the economy, the outlook may be for further slowing in activity as rates turn even more positive in real terms. Real rates in the US are already positive: the Fed funds rate exceeds headline CPI by 230bps and both the 2yr and 10yr UST real yields are positive for the first time since mid-way through 2019. We expect that rates will remain positive in real terms in 2024, rising to almost 3% under our assumption that the Fed hold rates unchanged until the end of H1 2024 while inflation should continue to slow.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The Jackson Hole speech committed the Fed to data dependency to drive decisions at upcoming meetings. Between now and the end of the year there are three more FOMC meetings: September, November and December. After the Jackson Hole meetings, markets are pricing in a bit more than a 60% chance of a 25bps hike by the November 1 meeting. Headline inflation should continue to trend downward through the rest of the year and the recent pullback in energy prices should help to take some of the upside volatility out of the equation. We believe the Fed wants to see prices moving lower in shelter and core services prices before it feels confident that disinflation is entrenched. With positive real rates to push higher over the next several months we would expect the economy to reflect more of the impact of tightening and offset the need for any additional tightening from the Fed. For now we are holding to our view that the Fed has completed its hiking cycle and that it will maintain rates at their current restrictive stance until June 2024.

Edward Bell

Edward Bell