Recent Search

Popular Searches

India has so far weathered the coronavirus outbreak with a strict nationwide lockdown which has been in place since 24 March 2020. The current phase of lockdown is scheduled to end on 3 May 2020. However, the government has indicated that restrictions may be extended in areas which are classified as ‘hotspots’ and eased in other areas. Unsurprisingly the economic cost of the lockdown has been immense. While it is still too early to put a number, the IMF has pegged India’s growth at 1.9% for FY 2021. In all likelihood, India will also see its first quarterly GDP contraction in Q1 FY 2021 since the 1980s.

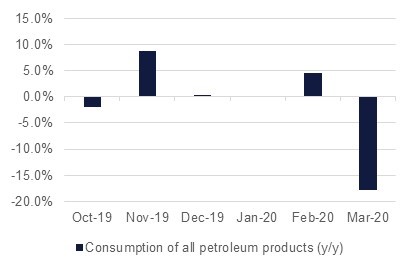

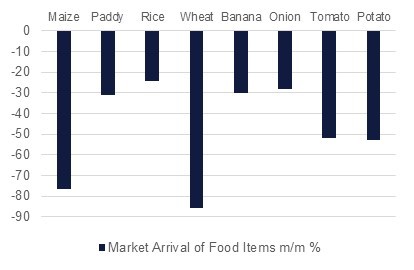

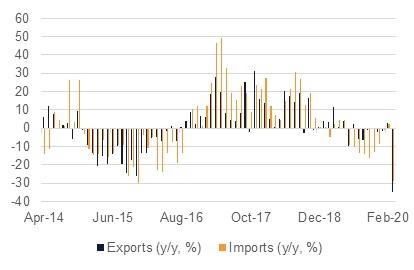

The secondary high frequency data points clearly shows the pain across sectors. While India does not officially publish the unemployment rate, the data collated by Centre for Monitoring Indian economy indicates that unemployment jumped to nearly 25% in the first week of April and since then has stayed around those levels. The power and all petroleum products consumption have simply collapsed since the lockdown. The peak demand for power has dropped nearly 26% y/y in the first two weeks of April while the consumption of petroleum products dropped -18.0% in March. It must be noted that the full lockdown came into force only in the last week of March. Cargo volumes at ports paint a similar picture. Worryingly, the rural supply chain appears to have broken ahead of the crucial harvesting season with the arrival of agricultural commodities at key markets falling substantially even though food is classified as an essential item.

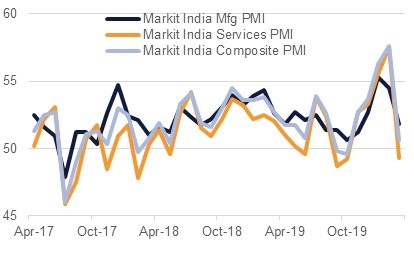

The Markit India PMI data for March corroborates some of the early pain but does not reflect the complete picture yet. While the services PMI fell below 50.0, the manufacturing and composite PMI did remain in expansion territory with readings of 51.8 and 50.6.

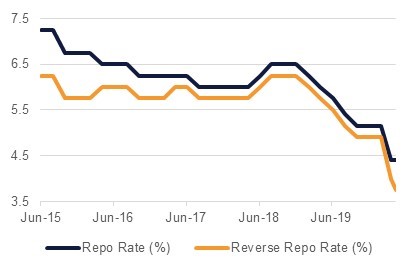

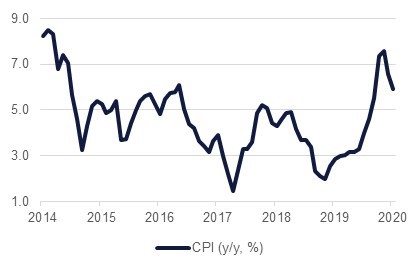

In terms of stimulus measures, the government has so far announced a minimal support package and said it is working on a more broad based fiscal stimulus which will be announced in the coming days. The Reserve Bank of India, on its part, has taken aggressive steps both in terms of lowering interest rates as well as ensuring liquidity support to various financial segments of the economy. On interest rates, the RBI has widened the policy rate corridor to encourage banks to lend more. The difference between the repo rate and reverse repo rate at 65 bps is the widest since early 2016. With inflation easing and oil prices remaining under USD 30/bbl, the RBI has further room to ease rates.

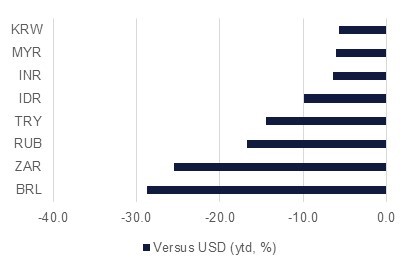

The financial markets have so far has performed in line with broad indices. Foreign Institutional Investors are net sellers to the tune of USD 7bn ytd in equity markets and USD 10.5bn in debt markets. INR has been resilient compared to other emerging market currencies with losses of -6.5% ytd.

.jpg) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

.jpg) Source: CMIE, Emirates NBD Research

Source: CMIE, Emirates NBD Research

.jpg) Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Emirates NBD Research, Bloomberg, Indian government agencies

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

.jpg) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Aditya Pugalia

Aditya Pugalia