Recent Search

Popular Searches

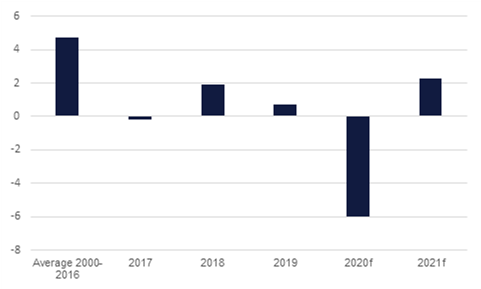

The IMF has released its outlook for the GCC region, and has actually become moderately more bullish than it had been previously. It now projects that the six-country bloc will see real GDP contract by 6% in 2020, an improvement from the 7.1% contraction it had previously anticipated in its June outlook. This is in line with its global outlook revision, where the forecast for worldwide growth was upgraded from -4.9% to -4.4% on the back of a stronger-than-anticipated economic recovery from the pandemic so far. In terms of the individual GCC forecasts, the Fund is more bearish on the prospects for the UAE than ourselves. The IMF has revised its forecast for the UAE down to -6.6% from -3.5% previously, lower than our own -5.5% forecast, although we recognise that the risks to our estimate are on the downside. The Fund sees growth recovering to 1.3% in 2021, broadly in line with our 1.2% forecast.

There was a modicum of greater optimism with regards a couple of political sticking points yesterday, although the distances between the parties on each side of both the US fiscal support package and the EU-UK trade deals remain considerable. In the US, Speaker of the House Nancy Pelosi said that the divide between the two sides was narrowing, and set a deadline of 48 hours for an agreement on a pre-election package to be agreed. While this might give some added impetus to talks, with some considerable ground to yet be made up – not least on funds for coronavirus testing – the prospect of a deal being made prior to the election remains uncertain. Federal Reserve Vice Chair Richard Clarida urged more stimulus in statements yesterday.

With regards the UK, while talks are still at an impasse, there was some mollifying language from the EU following the UK’s declaration at the end of last week that a no-deal scenario was increasingly likely. The EU’s chief negotiator, Michel Barnier, will speak with UK counterpart David Frost by telephone this week. There are a little over two months until the current trading arrangements come to an end.

Source: IMF, Emirates NBD Research

Source: IMF, Emirates NBD Research

US treasuries were lower across the curve even though there has still been little actual movement on bridging the gap between Republicans and Democrats for more stimulus measures. Yields on 2yr USTs were marginally higher at 0.145% while 10yr yields ticked up by 2bps to 0.769%.

The new issue pipeline has heated up regionally. Oman has mandated banks for a three tranche (3yr, 7yr and 12yr) USD benchmark issue only a few days after having been downgraded to ‘B+’ by S&P. Investment Corporation of Dubai has also mandated banks for a USD 5yr issue while Arab National Bank has also mandated for a new sukuk. OQ, Oman’s energy holding company, has also mandated banks for a USD bond.

The USD erased a large portion of the gains it garnered at the end of last week on Monday. The DXY index fell by -0.26%, retreating from a tough resistance line of 93.900 and trades around 93.430. Cautious optimism surrounding a US stimulus package remains intact. USDJPY was little changed but there was a slight spike this morning and trades around 105.55.

The EUR surged off the back of dollar weakness, ignoring concerns expressed by ECB President Christine Lagarde over rising Covid-19 cases in Europe. The currency advanced by 0.35% to reach 1.1770, just shy of the 1.8 handle and the 50-day moving average of 1.1795. The GBP also performed well amid hopes that Brexit talks could resume. Sterling briefly rose above the 1.3 big figure, but a credit downgrade by Moody's has weighed on the currency which currently trades around 1.2945. The AUD reached highs of 0.7115 in the afternoon but has reversed all of these gains and has declined this morning by -0.55% to reach 0.7040, whilst the NZD also dipped, trading at 0.6580.

Despite some moderately more encouraging language towards a new US fiscal support package, and a Brexit deal, yesterday than seen at the close of last week, equity markets around the world remained under pressure at the start of this week. In the US, the NASDAQ closed 1.7% lower, while the S&P 500 wasn’t far behind with a loss of 1.6%, and the Dow Jones lost 1.4% on the day. In Europe, the CAC, the DAX and the FTSE 100 closed 0.1%, 0.4% and 0.6% lower respectively.

Oil prices edged lower to begin the week as OPEC+ cautioned of a precarious outlook for oil as the Covid-19 pandemic continues and threatens demand. Saudi Arabia’s energy minister, Prince Abdulaziz bin Salman, noted that the outlook was “uncertain” and that OPEC+ had to “nip” negative measures early. However, the JMMC, the OPEC+ advisory body, still has not endorsed delaying the tapering of production cuts from the start of 2021, potentially leaving the oil market oversupplied in the coming months.

Daniel Richards

Daniel Richards