Recent Search

Popular Searches

The IMF has upgraded its outlook for the global economy, forecasting a contraction of -4.4% this year from -5.2% in its June update. Global growth is expected to rebound to 5.2% in 20201, but the Fund warned that the recovery would be uneven until the coronavirus pandemic has been contained. The upgrade to 2020 figures reflects the impact of unprecedented monetary and fiscal stimulus this year, with the latter estimated at USD 6tn globally. Nevertheless the contraction in global growth expected this year will still be the worst since the Great Depression almost a century ago. The biggest upward revision was to the US, which is now expected to contract by -4.3% from -8% previously after better than expected Q2 GDP and encouraging data in Q3. China remains the only major economy likely to grow this year, with the forecast upgraded to 1.9%. Overall however, EM growth forecasts were revised slightly lower compared with June.

In the GCC, the IMF has revised its forecast for the UAE down to -6.6% from -3.5% previously, lower than our own -5.5% forecast, although we recognise that the risks to our estimate are on the downside. The Fund sees growth recovering to 1.3% in 2021, broadly in line with our 1.2% forecast. Saudi Arabia’s economy is expected to contract -5.4% this year (better than the June forecast of -6.8%) returning to growth of 3.1% in 2021. The new forecasts for KSA are broadly in line with our own view.

US inflation was in line with consensus forecasts at 0.2% m/m and 1.4% y/y in September. Core inflation eased to 0.2% m/m from 0.4% m/m in August, but the annual rate was unchanged at 1.7%. In Germany, the rise in Covid-19 cases dampened investor sentiment with the ZEW survey expectations index falling to 56.1 in October from 77.4 in September, well below the median forecast. The current situation index improved slightly to -59.5 from -66.2. In the UK, the ILO measure of unemployment rose to 4.5% in the three months to August as 153k jobs were lost, from 4.1% previously. The unemployment rate was the highest since 2017, but is likely to rise further as the furlough scheme comes to an end this month.

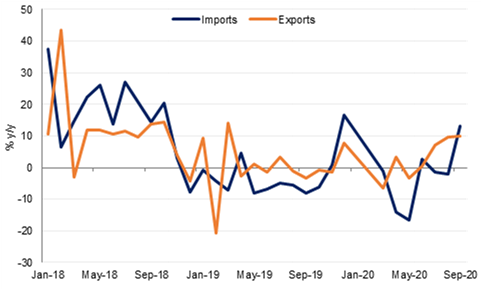

Chinese imports surged 13.2% y/y in September, from -2.1% in August and much higher than consensus forecasts. This likely reflects a recovery in domestic demand in China as well as some stockpiling of tech products as concerns about future restrictions on imports increase. Exports grew 9.9% y/y broadly in line with expectations.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries closed higher overnight as markets responded to delays in Covid-19 vaccine tests. A slowdown in US inflation also didn’t help sentiment and yields across the curve closed the day higher: yields on the 2yr UST were down by a bit more than 1bp at 0.139% while the 10yr yield fell by more than 4bps to 0.7272%. The 2s10s curve flattened back below 60bps.

High yield and emerging market bonds were higher on the day as well despite no movement on stimulus talks in the US. Bank Indonesia held policy rates unchanged at 4% yesterday and will continue to use alternative measures, such as directly buying government bonds, to support the economy. Korea’s central bank also held policy unchanged at its meeting earlier today.

The USD advanced by the most in more than two weeks on Tuesday and has held firm this morning. The DXY index surged by 0.50% to reach 93.525 as traders weighed up the fading prospect of Congress and the White House reaching a fiscal stimulus deal. This had little effect on USDJPY overall which recorded minor gains and trades at 105.40.

The EUR fell by -0.58% to reach 1.1745 following the USD's strength and a risk-averse sentiment. The GBP was amongst the biggest movers, declining by -0.97%, trading at 1.2940 following reports that there was still no progress between the UK and the EU on Brexit. The AUD also suffered from the strength of the greenback, declining by -0.67% to reach 0.7161, whilst the NZD experienced some modest gains and closed at 0.6651.

Risk-off tone returned to equity markets yesterday, as concerns over rising case numbers seemingly returned to the fore following a fairly robust start to the week on Monday, with the pause to the Johnson & Johnson vaccine trial and no real progress on further US stimulus contributing to the change in sentiment. In the US, the Dow Jones and the S&P 500 both lost -0.6% on the day, while the NASDAQ was almost flat, down just -0.1%. Meanwhile in Europe, the FTSE 100 (-0.5%, supported by a weaker pound), the CAC (-0.6%) and the DAX (-0.9%) all closed lower, and in Asia the Shanghai Composite closed flat but is down -0.6% so far in trading today.

Within the region, equities performed more positively. The DFM gained 0.1% and the Tadawul 0.7% yesterday.

Oil prices managed to gain overnight with Brent futures up 1.8% at USD 42.45/b and WTI up nearly 2% to close at USD 40.20/b. OPEC cut its 2021 demand growth expectations by 80k b/d to a recovery of 6.54m b/d. While a strong recovery, that would still leave 2021 demand well below levels seen at the end of 2019.

Suhail al Mazrouei, the UAE’s energy minister, said that OPEC+ still plans to taper its production cuts at the start of 2021. However, as the demand picture darkens we would expect there to be some push back on the timing of the output change.