Recent Search

Popular Searches

Gold had its worst week since late November last week, falling 2.6% to USD 1,849/troy oz and taking the rest of the precious metals complex down with it. Prices are extending their losses in early trading this week with gold prices now flat since the start of the year. The immediate catalyst for the sell-off seems to be the pop in UST yields which have moved back above 1% in short order.

.png) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Now that the US election cycle is nearing its conclusion with the pending inauguration of Joe Biden as president and Democrats taking control of both chambers of Congress, markets are bidding up assets favoured by the “reflation trade” - essentially anything that would benefit from economic activity in the US and elsewhere going back to pre-pandemic levels of activity. Equities also seemed to barely register the disruptions at the US capitol last week, instead focusing on whether Joe Biden would face resistance from within his own party over the level of fiscal largesse he plans to introduce.

Treasury yields have been a major beneficiary of the expectation that growth will improve and 10yr UST yields gained more than 20bps last week to close above 1.11%. Inflation-adjusted yields have also turned around sharply, gaining 14bps on the 10yr inflation-indexed treasury security in the past week. Also abetting the rise in yields has been the lack of Fed commentary suggesting rates markets were running too far ahead of the recovery. Fed vice chair Richard Clarida noted last week that it would be “quite some time” before the Fed began tapering back its quantitative easing programme and that if the rise in yields reflected “optimism about the economy”, it wasn’t a worry to him

The near-term outlook for gold will be linked to how strongly UST yields continue to rise, barring any political surprise that could see a flight to safety. We believe some of the current strength in market yields is overdone as we expect that the incoming Biden administration’s spending may fall short of plans for trillions of dollars of fiscal expansion. But we nevertheless do expect yields to move upward over the course of the year in line with improvements in the economy, both in the US and elsewhere. That will weigh on gold and other precious metals, taking them lower from current levels.

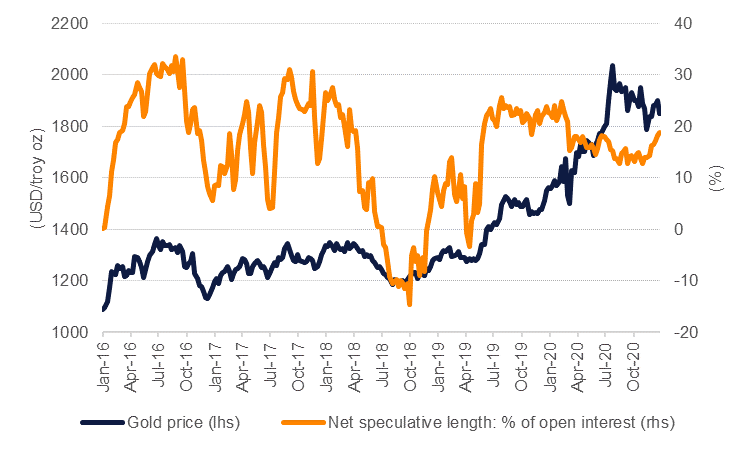

Investors are also highly concentrated in long gold positions. Speculative net length in gold futures and options has expanded recently, even as prices wavered, likely as a hedge against unknown downside risks for other asset classes. A prolonged rally in UST yields could see investors flood out of long gold positions, raising the risk of a disorderly sell-off.

Source: Bloomberg, Emirates NBD Research. Note: futures and options.

Source: Bloomberg, Emirates NBD Research. Note: futures and options.

That said, there are some still major risk events in the market that will provide a floor for gold. Most of the positive surprises surrounding politics and the Covid-19 pandemic are already known to the market. From the 20th of January onward the US will have a government ready to endorse high levels of fiscal spending, although the process is likely to face challenges along the way. The December non-farm payrolls report, while highlighting the need for additional support measures in the US, may have been a foretaste of another dip in labour activity, rather than a coda to a difficult 2020. Meanwhile, the positive shock of Covid-19 vaccines is likely already priced into risk assets. Vaccines are already being deployed across economies to help push normalization of economic activity but the path has been bumpy in major economies such as the US and Eurozone.

Indeed, the recent re-introduction of harsh lockdown measures in several European and Asian economies highlights that the path of the Covid-19 pandemic, and its economic consequences, is clearly not linear and gold will retain its allure as a haven structurally even if short-term conditions are weighed against it.

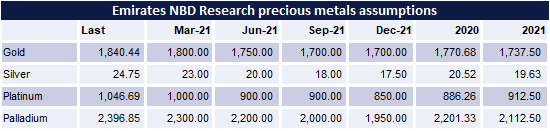

Source: Bloomberg, Emirates NBD Research. Note: USD/troy oz, quarterly/annual average.