Recent Search

Popular Searches

Eurozone services and composite PMIs were revised slightly higher than their flash estimates for November, coming in at 51.9 and 50.6 respectively. However, the data still suggests there is almost no growth in the Eurozone economy in Q4. In the UK the composite PMI was also slightly higher than the flash estimate, but still below the neutral 50.0 reading. Nevertheless, GBP rose to a seven-month high against the dollar as polls show the conservative party maintaining a strong lead just a week ahead of elections.

In the US, the ISM non-manufacturing index came in below expectations at 53.9, down from the October reading and pointing to slower growth in the services sector. The Markit services PMI was unchanged at 51.6 in November. The ADP private sector employment number for November fell sharply to just 67k, down from 125k in October and well below consensus forecasts for 135k new jobs. This raises the risk of a downside surprise to tomorrow’s important US non-farm payrolls data.

The Bank of Canada kept rates on hold as expected yesterday at 1.75%, but the tone of the statement was more hawkish, suggesting that the bar for a rate cut is high. Meanwhile in Australia, third quarter GDP growth missed estimates coming in at 0.4% q/q and 1.7% y/y. Consumer spending remained soft despite tax and interest rate cuts, as households boosted savings rather than spending. The probability of another rate cut in February 2020 has increased to 70% this morning following the data release, from 50% previously.

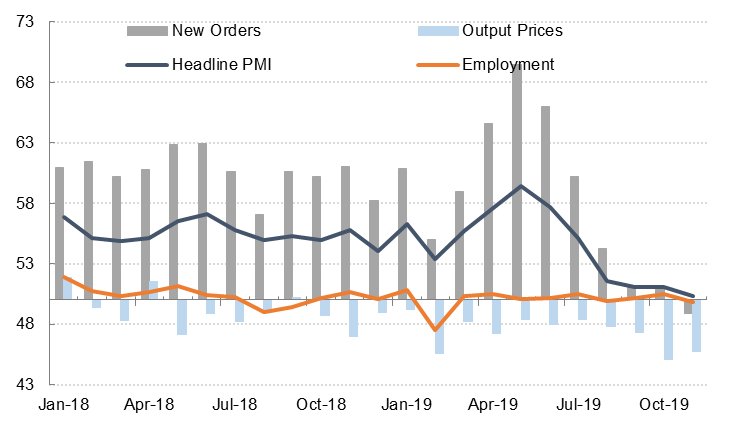

The Markit UAE PMI slipped to 50.3 in November, only fractionally above the “no change” level. The November reading was lowest reading since August 2009, and was largely due to a decline in new orders and slower growth in output last month. The weakness in new work was despite further price discounting on the part of panellists. The UAE PMI survey has been markedly softer in H2 2019 after a relatively strong performance in Q2, although that was largely due to a rise in the volume of export orders rather than domestic demand.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

Fixed Income

Treasuries moved lower following yet another report where officials negotiating the trade deal with China contradicted the comments of the US President Donald Trump and indicated that a deal is within reach and could be agreed within days. At the time of this writing, yields on 2y UST and 10y UST were at 1.57% and 1.76% respectively.

Regional bonds continued to move broadly in line with benchmark yields. The YTW on Bloomberg Barclays GCC Credit and High Yield index closed at 3.25% while credit spreads tightened to 152 bps.

FX

Sterling rose to a seven month high against the dollar yesterday as the Conservative Party has maintained its lead in the polls a week before elections.

CAD has rallied to 1.3187/USD at the time of writing following the BoC statement which was slightly more upbeat on the economic outlook than the market had expected.

NZD is also trading firmer this morning after the central bank gave banks more time to meet capital requirements, and RBNZ Governor Orr said monetary policy was in a “hold phase”, paring expectations for a rate cut.

Equities

Developed market equities closed higher following reports that comments from US President on trade deal with China were off the cuff in nature. The S&P 500 index and the Euro Stoxx 50 index rallied +0.6% and +1.4% respectively.

Most regional equities closed higher. The DFM index gained +0.6% on the back of strength in market heavyweights. Elsewhere, Egyptian equities snapped 3-day losing streak to close higher. The EGX 30 index added +1.2%.

As per latest information available, the institutional tranche of the Saudi Aramco IPO was oversubscribed nearly 3 times.

Commodities

Oil markets jumped thanks to a bullish EIA report and headlines suggesting an extension of the current OPEC+ production cuts is on the cards. Brent futures gained 3.6% to USD 63/b while WTI added more than 4% to close at USD 58.43/b.

In the US, crude oil stocks fell nearly 5m bbl last week, their biggest drop since the start of September. However, gasoline and distillate inventories rose. Production held steady at 12.9m b/d while exports slipped slightly to 3.14m b/d.

OPEC meets today for its session to decide on whether to maintain, extend, deepen or end production cuts. We expect an extension of the current scale of cuts is the most likely outcome with a possible deepening of the cuts. Oman’s oil minister, despite his country not being part of OPEC, indicated that all Gulf producers were in consensus to extend cuts. Whatever the outcome, ensuring compliance with the cuts remains a barrier to OPEC effectively balancing markets. News reports indicate that Saudi Arabia would be prepared to increase output to maintain compliance although they would also endure any lower prices as a consequence.

Aditya Pugalia

Aditya Pugalia