Recent Search

Popular Searches

Non-resident deposits in Qatar’s commercial banks declined -5.2% m/m in August, the fourth consecutive monthly drop. Since the end of May, non-resident deposits have declined –QAR 35.6bn (-USD 9.8bn). This was largely offset by a massive QAR 95.2bn rise in public sector deposits over the same period, with QAR 28.7bn coming in August alone. This has been more than sufficient to offset the decline in non-residents’ deposits as well as private sector deposits, which have shrunk –QAR 28.2bn since sanctions we imposed by Saudi Arabia, the UAE, Bahrain and Egypt in early June. However, private sector deposits appear to have stabilized in August. Total bank deposits stood at QAR 793.6bn at the end of August, down a marginal -0.2% y/y.

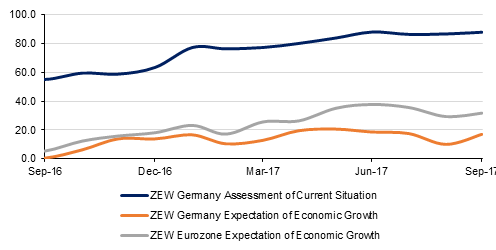

German investor sentiment improved more than expected in September, the ZEW research institute showed its economic sentiment index rose to 17.0 September from 10.0 in August. This was far stronger than the market consensus of 12.5. A separate measure of investor’s perception of current condition’s edged up to 87.9 from 86.7, this was the highest level in 88 months. The data underscore other business survey such as the Ifo which point to a continued acceleration in growth in the Eurozone’s largest economy.

Japanese exports rose at their fastest pace in 4 years, with exports rising 18.1% in August against July’s rise of 13.4%. A boom in the shipments of cars, car parts, and semiconductor manufacturing equipment boosted exports to Japan’s key markets. Exports to the United States in August by 21.8 percent versus an 11.5 percent annual increase in the previous month. China-bound exports rose 25.8 percent year-on-year in August, faster than a 17.6 percent annual increase in July underpinned by electronic screens panels and plastics exports.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasuries drifted lower ahead of the FOMC meeting scheduled for later today. With the balance sheet reduction seemingly priced in, investors will look to clues with regards to a possible rate hike in December. Currently, the market is pricing in a 53.2% probability for that to happen. Yields on the 2y USTs added 1 bps to 1.40%, on 5y USTs 1 bps to 1.83% and 2 bps on 10y USTs to 2.24%.

Regional bond market moved in lockstep with benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index rose 2 bps to 3.45% while credit spreads widened by 1 bps to 159 bps.

The impact of continued political stalemate between Qatar and other GCC countries continued to affect the country’s banking system as reliance on government deposits increased further. According to data released by the Qatar Central Bank, overall deposits grew by 5% to QAR 645bn helped by 10.5% increase in August in public sector deposits to QAR 295bn. The non-resident deposits declined from QAR 171bn in June to QAR 149bn in August. Having said that, the impact of the same was marginal on banking sector bonds with QNBK 21s closing flat even though z-spread did widen by 2 bps to 125 bps.

Further signs of primary activity picking up following the summer lull was reflected in reports that Abu Dhabi Financial Group plans to raise USD 100mn through private placement of a 3-year bond. Additionally, Islamic Development Bank priced its 5year USD 1.25bn bond issue at MS+37 bps.

The ongoing dispute between investors and Dana Gas went a step further as hearing in the London trial had to be postponed after the company said that a court in the UAE has issued orders to block the trial. The judge postponed the case to later this week and said that the hearing will start despite the order and in the absence of Dana Gas if need be.

Over the last month, we have seen USD underperform relative to the other major currencies, with only JPY and NZD softening more. Analysis of the Dollar Index shows that during this period, the index has fallen by 1.80% to 91.949, not far from the one year low of 91.011 on September 8th. These declines reinforce the daily trend that has been in effect since January 3rd 2017 and indicate that the dangers remain to the downside.

It is of note that the 200 week moving average (92.69) which previously acted as a support has now acted as a resistance for a second consecutive week with the price staying below this key level. Prior to this, the index has not traded below this key level since May 2014 and, combined with the strong daily downtrend, signals that to catalyse a reversal in price action, there needs to be significant dollar supportive news in the form of either a rate hike from the Federal Reserve or stimulus from the Trump administration. Should we see another weekly close below the 200 week MA, it could give way to more significant declines.

Developed market equities drifted higher as investors await the outcome of the Fed meeting later today. The focus will be on the dot plots. The S&P 500 index and the Euro Stoxx 600 index added +0.1% each.

It was a mixed yet sluggish day of trading for regional equities with the DFM index and the Tadawul losing -0.2% and -0.6% respectively while the ADX index added +0.3%. There was no standout performer in terms of stocks.

Oil prices drifted lower for a second consecutive day with Brent futures and WTI futures losing -0.3% and -0.4% respectively. There was increased speculation about the OPEC cuts following comments from the Iraq’s oil minister where he suggested that OPEC should cut supply by an additional 1% and extend cuts until the end of 2018.

Click here to Download Full article