Recent Search

Popular Searches

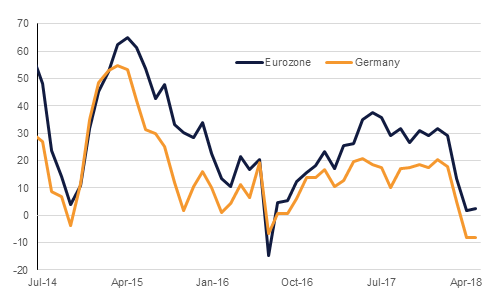

The second estimate of Eurozone first quarter growth was released yesterday, confirming the 0.4% previously cited. Growth was particularly constrained by the bloc’s largest economy, Germany, which grew just 0.3% in Q1 according to data released yesterday – compared to 0.6% the previous quarter, and expectations of 0.4%. Officials at the Bundesbank have previously laid the blame for the slow start to the year on factors such as adverse weather conditions and a flu epidemic weighing on consumption, and anticipate that growth will pick up over the remainder of 2018. Indeed, industrial production output in March exceeded expectations, suggesting the worst is past. However, Eurozone economies from Portugal to Romania also had a weak first period according to flash results, and the ZEW investor sentiment survey for the Eurozone remains fairly weak at 2.4. While up from 1.9 in April, this remains far off the 31.8 at the start of the year. Germany’s survey result was -8.2, in line with expectations. Respondents cited concerns over the US’s departure from the JCPOA, rising oil prices and potential trade wars.

Japan GDP contracted for the first time in nine quarters in Q1, falling by 0.6%, compared to expectations of -0.1%. Provided global trade wars do not escalate, the economy’s performance should improve over the rest of the year as exports are expected to perform well.

US retail sales showed growth of 0.3% m/m in April, matching analyst expectations and down from the March growth figure of 0.8% - revised up from 0.6%. Despite the more modest headline expansion, the retail control group expanded by 0.4%. Together with the March revision, it suggests that the US economy remains fairly robust. In the UK, workers got a real pay increase for the first time in over a year as wage growth expanded more rapidly than inflation.

Kuwait’s National Assembly announced yesterday that it would delay its implementation of the 5.0% GCC-wide VAT scheme until 2021. Under the initial deal, Kuwait was scheduled to implement the tax in 2019, following Saudi Arabia and the UAE, which both brought it in on January 1 this year. Higher oil prices will have diminished the urgency of introducing the tax, and many MPs have been concerned over the impact it would have on ordinary Kuwaitis.

Source: Bloomberg,Emirates NBD Research

Source: Bloomberg,Emirates NBD Research

Treasuries closed lower across the board amid stronger than expected retail sales data. However, there was no other significant catalyst behind this sharp move. Yields on 2y UST, 5y UST and 10y UST closed at 2.57% (+3 bps), 2.91% (+5 bps) and 3.07% (+7 bps).

Regional bonds closed lower following the move in benchmark yields. The YTW on the Bloomberg Barclays GCC Credit and High Yield index jumped +5 bps to 4.63% while credit spreads tightened 2 bps to 177 bps.

Qatar International Islamic Bank has hired banks for a USD 500mn sukuk. The bank said it will go to the market when pricing is attractive.

The dollar is trading slightly firmer this morning, the Dollar Index currently up 0.10% at 93.300, levels last seen in December 2017.With the 14-day Relative Strength Index showing overbought conditions at (72.9), some profit taking may hinder further gains. However, a daily close above 93.752 (the 50% one year Fibonacci retracement) is likely to cause further gains towards 94.8 in the medium term.

This afternoon, markets will be looking towards the Eurozone where revised inflation data for April is expected to show that Eurozone CPI increased 1.2% y/y, revised down from 1.3% y/y. Any greater than expected downward revisions in the data is likely to result in further pressure on the Euro, which is currently on target to have a weekly close below the 50- week moving average (1.1921) for the first time since April 2017.

Developed market equities closed lower on the back of weakness in US equities. A stronger than expected retail sales data drove treasury yields higher as investors turned wary of a faster than expected rate hikes from the Fed. The S&P 500 index dropped -0.7% while the Euro Stoxx 600 index closed flat.

Regional markets closed mixed with the DFM index adding +1.1% and the Tadawul dropping -0.4%. The strong performance on the DFM was driven by strength in Emaar Development (+1.5%) as the stock was included in the MSCI index. Similarly Qatar National Bank gained +2.4% after the weight of the stock was increased in the MSCI index.

Oil prices were up yesterday although gains were relatively muted. Brent closed up 0.26% at USD 78.43/b but had broken above USD 79.40/b at one point during the day. WTI added 0.49% to close at USD 71.31/b. There were few data points or policy developments to shift the market.

Most of the action in commodity markets occurred in gold where the yellow metal broke below USD 1,300/troy oz, its first time below that marker this year. A spike in US treasury yields and gains in the dollar helped to move markets away from gold.

Click here to Download Full article

Daniel Richards

Daniel Richards