Recent Search

Popular Searches

Eurozone third-quarter real GDP growth was unchanged from Q2, coming in at 0.2% q/q and 1.7% y/y. Both readings were in line with analyst expectations. Much of the slowdown will be attributable to the slowdown in German autos production related to emissions testing – and indeed, German GDP contracted 0.2% q/q, the first negative growth since 2015. As such, there is little that is likely to cause the ECB to change course on its plan to end asset purchases by year-end.

UK Prime Minister Theresa May’s Brexit deal appears to have the qualified support of her cabinet – for now. She held a press conference yesterday evening after five hours of discussions with her ministers, telling assembled reporters that they had taken a ‘collective’ decision to press ahead with the deal she has clinched with the EU. However, while no ministers resigned immediately upon reading the text yesterday, there are rumours of potential departures in the planning. She will also have a hard time getting the deal through parliament as concerns remain that the deal could see the transition period extended past 21 months if a solution to the Irish border question is not found within that time frame. Staying in the UK, CPI inflation stayed steady at 0.1% q/q and 2.4% y/y in October, just under consensus estimates of 0.2% and 2.5%. This is despite figures released this week which showed wage growth of 3.2% y/y last month, the fastest in a decade. The slight drop in inflation will alleviate any pressure on the BoE to hike rates at its December meeting, an action it is likely reluctant to take prior to the finalisation of Brexit on March 29 next year.

Fed Chair Jerome Powell spoke in Dallas yesterday. During his appearance he credited some of the robust performance of the US economy to the policies of the Federal Reserve, and stated that he expected it to remain strong. He also reiterated the necessity of raising rates in order to prevent inflation and financial bubbles - risks they have to take ‘very seriously.’

Treasuries closed higher as weakness in risk assets continued. However, it closed off session highs after the UK Prime Minister managed to get the approval of the cabinet for the draft Brexit bill. Yields on the 2y UST, 5y UST and 10y UST closed at 2.86% (-3 bps), 2.95% (-3 bps) and 3.12% (-1 bp) respectively.

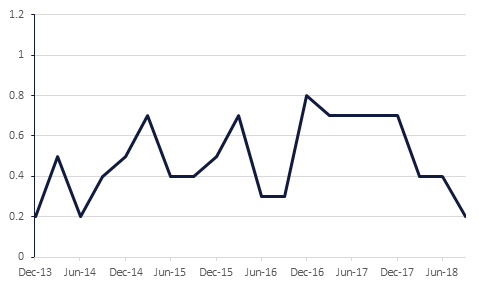

Regional bonds continued to drift lower. The YTW on the Bloomberg Barclays GCC Credit and High Yield index rose to 4.72% and credit spreads widened 5 bps to 178 bps.

AUD is outperforming this morning and has gained against all the other major G-10 currencies during the Asia session. The catalyst behind this move was a report from the Australian Bureau of Statistics which showed stronger than anticipated employment data. Compared with expectations for an increase in the unemployment rate to 5.1%, the rate remained at 5.0% in October. In addition, 42,000 full time jobs were added, an increase compared with the 24,000 created the previous month.

As we go to print, AUDUSD is trading 0.53% higher at 0.72697 and is on course to gain for a third consecutive day. Analysis of the daily candle chart shows that the price has found support earlier in the week at the 50-day moving average (0.7163) and has now broken above the 100-day moving average (0.7257). The next level to be mindful of is the 23.6% one-year Fibonacci retracement (0.7284), a daily close above this level may result in further gains towards the 0.7540 handle, not far from the 200-day moving average (0.7454) and 38.2% one-year Fibonacci retracement (0.7447).

Developed market equities closed lower as weakness in technology stocks continued. The S&P 500 index and the Euro Stoxx 600 index dropped -0.8% and -0.6% respectively.

Regional stocks closed mixed. The ADX index added +1.1% while the Tadawul dropped -1.2%. First Abu Dhabi Bank rose +2.8% after the stock weight was increased in the MSCI EM index following the semiannual review. Qatar Fuel closed limit down after the company was not included in the index. Doha Bank declined -6.0% after the stock was removed from the index.

American Petroleum Institute (API) data released yesterday showed US inventories climbing 8.8mn b last week, compared to 7.8mn the previous week, contributing to the convergence of bearish factors around the world which have pushed both benchmarks into a bear market over the past week. Brent crude closed at USD 66.12/b yesterday, up 1.0% on the previous day, but nearly a quarter off recent highs of USD 86/b seen last month. WTI closed at USD 56.25/b, also up 1.0% on the previous day, but down from a high of USD 76.41/b last month.

The rout in prices is being taken seriously by OPEC member states, and yesterday UAE energy minister and OPEC president Suhail al-Mazrouei said that the group would consider taking even more than the 1mn b/d mooted by Saudi Arabia earlier in the week off supply. The likelihood of a concerted change in policy by the bloc following the December 5 meeting in Vienna is increasing.

Daniel Richards

Daniel Richards