Recent Search

Popular Searches

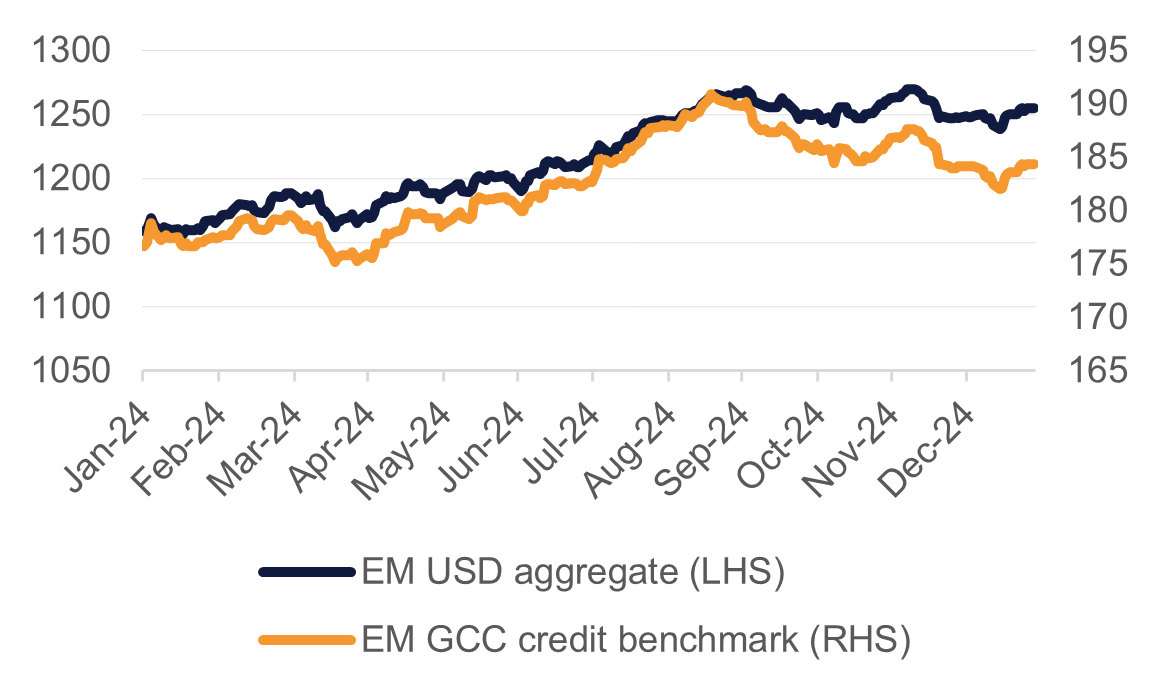

Emerging market bonds continued to gain last week with a broad index of USD-denominated debt up 0.4%, taking its year-to-date gains to 0.6%. The rally stood out as financial markets adjusted to the policies of the new Trump administration, particularly on trade and energy that could directly hit many emerging economies. US Treasuries gained last week as economic data was a little softer than expected (higher initial jobless claims, weaker services PMI).

In the week ahead markets will be focused on the first FOMC meeting of the year (Emirates NBD Research forecasts no change) and how the Federal Reserve will stand up to pressure from President Trump to cut rates.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

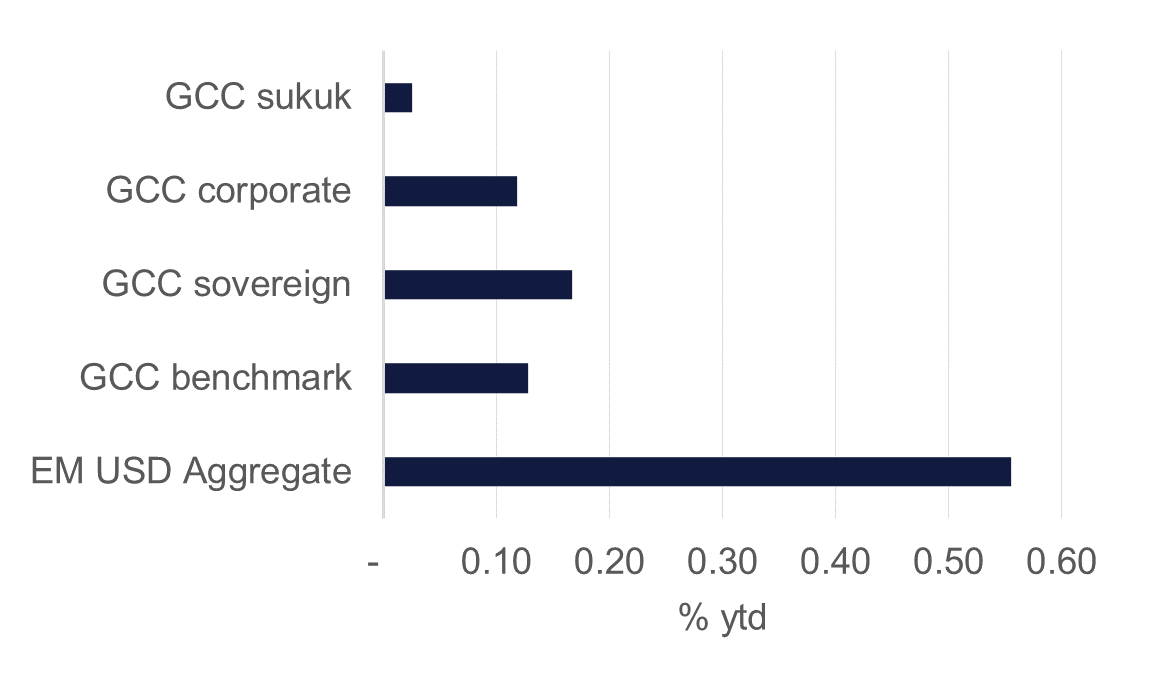

GCC bonds also rallied last week with a benchmark index provided by Bloomberg up 0.4% though prices now have only just got back to levels hit at the end of last year. Spreads across the wider-GCC index tightened by 4bps last week. At a sector breakdown the GCC sovereigns and high yield indices were both up by 0.5% while an index of sukuk was higher by 0.2%.

In regional data, the IMF expects real GDP growth of ‘around’ 4% in the UAE this year, supported by non-oil activity and growth in the oil sector. Emirates NBD Research expects a faster pace of growth at 5% with both the non-oil and oil sectors growing this year.

The UAE raised AED 550m reopening a 2027 sukuk with a yield of 4.32% and another AED 550m reopening a 2029 sukuk at a yield of 4.43%. The next auction will take place on February 25.

Elsewhere Turkey’s central bank cut the one-week repo rate by 250bps at its first meeting of 2025, taking the benchmark policy rate to 45%. This was the second cut in a row from the TCMB and further easing is expected as inflation is projected to slow.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The primary issuance last week was a new dual tranche issue from PIF in Saudi Arabia. The wealth fund raised a total of USD 4bn:

Since the start of 2025 Saudi sovereign USD borrowing (direct government and PIF) has reached USD 16bn, more than half of total sovereign USD borrowing completed in 2024.