Recent Search

Popular Searches

With trade and geopolitics continuing to dominate the headlines the likelihood is that the USD will remain relatively underpinned, notwithstanding occasional bouts of profit-taking which were witnessed at the end of last week. President Trump is in Japan having meetings with PM Abe, and this may result in a bilateral trade deal with Japan. However, progress with China is clearly what the markets want to see and the trend of the last few days has seen this relationship deteriorate if anything as the Huawei issue has added intensity to the trade dispute. It seems likely that the Osaka G20 meeting at the end of June will be the next critical event in this saga, with Presidents Trump and Xi set to meet each other, but before then there is probably more room for the relationship to sour further first before any improvement can be expected.

Economic data over the end of last week were overshadowed by political developments, but the pattern of recent weeks has been one of renewed weakness overall casting doubt on the sustainability of recoveries seen in Q1. Durable goods orders in the US came in softer for April, declining by more than 2% month on month. Most of the decline was attributable to a drop in commercial vehicle orders as airlines defer purchases of Boeing aircraft affected by safety issues. However, vehicle sales also fell (3.4% m/m) while core orders were flat. Other PMI readings in Europe and the US have also been soft, and this week that tone is also expected to be seen in China when its PMI’s are released.

Weaker UK retail sales data were also seen, but Theresa May’s decision to resign as prime minister of the UK dominated unsurprisingly. May’s position had been tenuous for months as she had failed repeatedly to get her Brexit deal supported in parliament and she faced considerable opposition from within her own Conservative party. However, with May to step down as prime minister from June the outlook for Brexit is not any clearer, and the chances of a no deal Brexit have probably increased as the EU may rebuff further attempts to negotiate a new deal.

Given that May’s resignation had been widely expected, sterling actually rallied on the news. There may have been an element of profit taking as investors closed out short positions on GBP. However, with the outlook for Brexit until the end of October deadline still highly uncertain, more downside for the currency could be on the cards. Indeed, more uncertainty or even a further delay, if the EU accepts another extension, would push out the timing for any rate hikes by the Bank of England and see investment and growth drift. Meanwhile EU election results will be scrutinized in terms of what they might mean for key appointments as well as the long term implications of populist success for EU-wide fiscal policy.

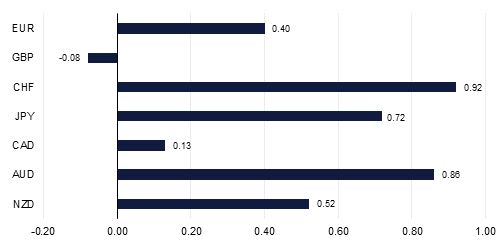

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg