Recent Search

Popular Searches

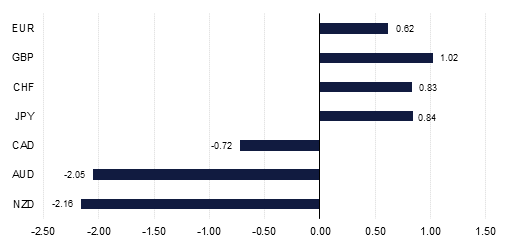

GBP was the best performing currency last week, rising by 1.02% against the USD as the Bank of England left interest rates unchanged and as the clouds surrounding Brexit finally cleared with the UK leaving the EU on the 31st January. Elsewhere currency safe havens were also in favour with the JPY and the CHF also benefiting from the uncertainty over the Coronavirus. In contrast the AUD and the NZD both fell as they were negatively impacted by the perception that Chinese growth would slow as a consequence of the virus.

On Thursday the Bank of England (BoE) kept interest rates on hold at 0.75%, which came as a surprise to many in the market who had been anticipating a small cut. A compromise did seem to be the outcome, however, with the commentary accompanying the decision still showing the Bank leaning towards a rate cut in the future. BoE governor Mark Carney commented that UK economic data were ‘good enough,’ but noted that the MPC needs to see more evidence of a pickup in activity to avoid the MPC easing in the future. Seven members voted for no rate change, and two members voted for a cut, the same as in the previous meeting. The BoE also released updated GDP and inflation forecasts, which were also a bit dovish, with the Bank expecting growth to slow to below 0.50%, while inflation is expected to tick up only slightly. The smooth passage of Brexit at the end of the week was also a relief after the uncertainty of the last few years. While much still remains to be done to secure a lasting trade deal between the UK and the EU, the markets appear overall optimistic that the two sides are heading in the right direction with UK PM Johnson apparently in favour a of striking a Canada style trade deal with the EU.

Data released last week showed US real GDP grew 2.1% on an annualized basis and up 2.3% on the y/y measure, while Eurozone GDP figures were weaker than expected, with France and Italy particularly soft. The FOMC also kept the Fed funds rate’s upper bound unchanged at 1.75%, as had been widely anticipated. The USD was mixed over the week as a whole, as different currencies were buffeted by uncertainty over the Coronavirus issue, with safe havens doing well but currencies dependent on China’s economy suffering. The coming week will see more volatility reflecting this, but markets will also focus on US jobs data which are expected to show a rise of 160k in non-farm payrolls, with the potential for weaker benchmark revisions softening the overall growth backdrop. The first Democratic party primary in Iowa will also be in focus, with success for Bernie Sanders seen as likely to make markets nervous about his chances of winning the Democratic nomination later this year.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research