Recent Search

Popular Searches

Reduced trade uncertainties and easing geopolitical tensions combined with good US economic data to produce a positive week for markets, with solid risk-on momentum underpinning the USD. Housing starts surged 16.9% in December to their strongest levels in 13 years, while manufacturing surveys were stronger than expected. Although headline readings for industrial production (-0.3% m/m) and retail sales (0.3% m/m) were not strong, underlying readings for both were much better (manufacturing output 0.2% and control group retail sales 0.5%). With inflation still sluggish (CPI at 2.3% but the PCE deflator steady at 1.6%), the Fed has plenty of room to maintain monetary policy where it is, which combined with easier policies elsewhere should keep risk appetite positive and help to underpin economic recoveries.

Both Turkey and South Africa’s central banks cut interest rates last week, given soft GDP growth in each country. Data from the UK also revived expectations of a January easing by the BOE, where official commentary is becoming more dovish. The case for another BOE easing this month does appear to be increasing and while we have not been expecting one, we acknowledge that it is becoming a possibility with inflation falling in December, to 1.3% on a headline basis and 1.4% at the core, and retail sales plunging (-0.8% m/m).

Central bank meetings in Japan, the Eurozone, and Canada will likely result in steady policy stances in the coming week, providing more confidence that accommodative policy settings will remain for some time. The ECB is likely to be focused on the review of the overall monetary policy framework, with a change to the inflation target likely to be under consideration. Elsewhere, Chinese GDP growth held steady at 6.0% y/y in Q4, and December activity data were stronger than expected, adding to signs of a stabilizing Chinese economy. Coming at a time when a ‘phase one’ trade deal has just been agreed this argues against the Chinese economy plunging much further for the time being, especially with the PBOC offering ongoing monetary support. All in all the backdrop should remain a supportive one for risk, and probably the USD, so long as there are no unwelcome surprises.

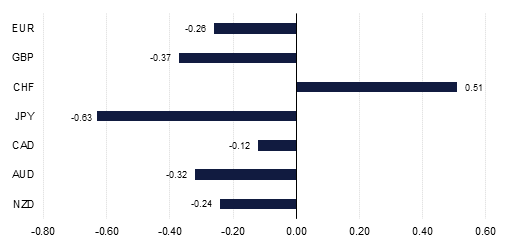

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research