Recent Search

Popular Searches

Following bank holidays in the UK and US yesterday markets will get back to normal today with safe havens in demand. The ongoing political chaos in Italy is the main catalyst for this as the situation there continues to deteriorate, casting doubt over Italy’s future relationship with the rest of the Eurozone. A new PM Carlo Cottarelli, a former IMF economist, has been appointed by the President and tasked with putting together a new government after the failure of the 5 Star/League coalition to provide a satisfactory cabinet. However, protests by the winners of the April election are likely which will probably mean that the new government is unlikely to get off the ground, making new elections likely with the possibility of an even more extreme anti-EU outcome further complicating matters.

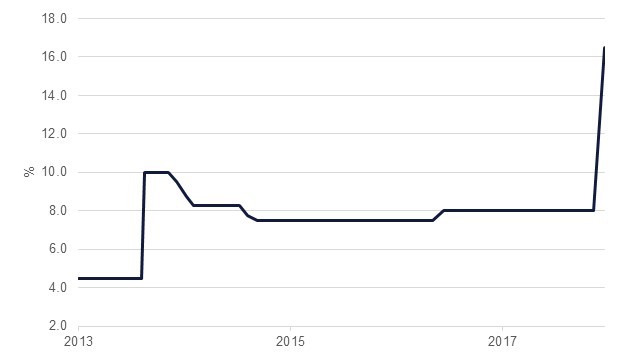

The Turkish central bank has announced a simplification of its monetary policy, implementing a symmetrical interest rate corridor with the overnight lending and borrowing rates 150 basis points either side of its one-week repo rate which will be set at 16.5%. Turkey’s complex multiple rates policy has long been criticised by investors, with the use of a wide interest rate corridor and multiple interest rates, and greater clarity could reassure markets following the sharp sell-off of the lira over the past several months. The bank’s monetary policy tool of choice of late has been the late liquidity window rate, which was hiked 300bps in an emergency meeting last week to 16.5% but will be raised to 19.5% from June 1st according to the Central bank.

Representatives from Libya’s opposing factions are due to meet in Paris today as UN special representative Ghassan Salame endeavours to bind them to holding elections this year in a bid to end the political impasse that has divided the country over the past seven years. UN-recognised Prime Minister Fayez al-Sarraj and eastern Libya commander Khalifa Haftar, along with a couple of other senior Libyan politicians, will be hosted by French President Emmanuel Macron. Agents of other countries with influence on the ground such as the UAE, Egypt, Qatar and Italy, will also attend the talks.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

With the US closed, political developments in Italy weighed on European bonds. While German bunds benefitted from flight to safety, Italian bonds continued to decline. Yields on 10y bunds dropped -6bps to 0.34% but increased +22bps on 10y Italian bonds.

Regional bonds closed largely unchanged with the YTW on Bloomberg Barclays GCC Credit and High Yield index remaining at 4.59% and credit spreads at 187bps.

Elsewhere, the Tunisian Central Bank said that the time is right to look to international markets to ease a deepening cash crush with the government deadlocked on an economic plan.

The JPY has benefited from heightened risk aversion amidst ongoing uncertainty about Italian politics. The dollar is generally firmer across the board as the EUR also loses out having failed to find support near the 1.1662 level (the 38.2% one year Fibonacci retracement), making further declines towards 1.1450 remain a risk. GBP also remains under pressure as the Scottish Nationalists are reprising their case for independence having published another blueprint about the economic benefits of such a move, and with the SNP leader having met the EU Chief Brexit negotiator Michel Barnier in Brussels yesterday.

It was a subdued day of trading as equity markets in the UK and US were closed. European equities closed lower as political developments in Italy weighed on investor sentiment. The Euro Stoxx 600 index dropped -0.3%.

Regional markets were largely dull with the exception of the Qatar Exchange (+1.5%) which rallied sharply. The gains were largely on account of MSCI rebalancing. All stocks connected with the same showed gains including Qatar National Bank (+2.9%), Industries Qatar (+2.8%) and Qatar Islamic Bank (+1.3%).

Oil prices dropped further as investors reacted to proposals from Saudi Arabia and Russia to increase output to make up for shortfall from Venezuela. Brent oil dropped -1.5% to close at USD 75.66/bbl.

It is worth noting that the spread between WTI and Brent has widened to a three-year high as record crude production in the US and surprise gain in US inventories weighed on WTI prices.

Click here to Download Full article