Recent Search

Popular Searches

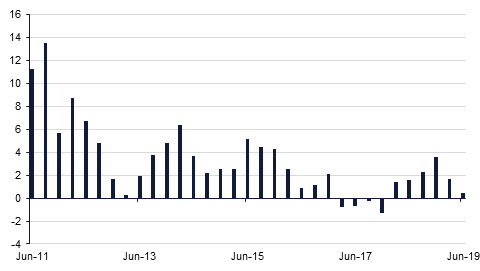

Fitch has downgraded Saudi Arabia’s sovereign credit rating to A from A+, citing rising geopolitical tensions and risks. Fitch’s rating on the kingdom is now one notch below Moody’s and one notch above Standard & Poor’s. Separately, Saudi Arabia’s economy slowed in Q219 as oil production cuts took their toll on growth. Overall the economy grew by 0.5% y/y in Q2, down from 1.7% y/y in Q1. The breakdown showed the oil sector contracting by 3% while the non-oil sector expanded by 2.9%, the fastest sincve since 2015, and consistent with firmer PMI readings in Q2. We forecast overall growth of 2.0% in 2019. Other data from SAMA showed net foreign assets rising USD 4.6bn in August to USD 502.2bn, following declines in June and July. Broad money supply growth accelerated to 4.9% y/y in August, reflecting faster growth in M1. Business & individual demand deposits grew 8.1% y/y in August, the fastest annual growth in this component since September 2015. However, private sector credit growth slowed to 2.4% y/y from 3.0 in July.

US activity data for September showed softness with both the Chicago PMI and the Dallas Fed index both faling by 3.3 points and 1.2 points respectively. Elsewhere in the world economic data reported yesterday was a mixed bag with the final release of UK Q2 GDP data showing an unexpected revision higher in y/y growth, to 1.3% from the provisional 1.2% estimate. Q1 growth was also revised higher, to 0.6% q/q and 2.1% y/y, from.5% and 1.8% respectively before. This morning the Japanese Tankan report fell to 5 from 7 In Q3, although this was better than expected.

The Eurozone also saw mixed data. There was a loss of 10,000 jobs in Germany during September, although the unemployment rate remained unchanged at 5.0% for the month. In the Eurozone as a whole, the unemployment rate unexpectedly fell to 7.4% in August down from 7.5% in July. Germany’s harmonized inflation measure also fell back to 0.9% y/y in the advance reading for September, from 1.0% y/y in the previous month. The national CPI rate also dropped to 1.2% y/y from 1.4% y/y in August. with lower energy prices being the key factor, with a price decline of -1.1% y/y in September.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

A 3bps rise has taken the yield on ten year US Treasuries to 1.7% this morning, while a similar gain has taken the five year yield to 1.57% and the two year yield has risen by 1 bps to 1.64%.

The Fitch downgrade on Saudi credit had little impact on the bonds. Presently there are unconfirmed reports that the kingdom seeks to issue a dollar-denominated sukuk as soon as early as next month, taking advantage of lower boring costs.

The Dollar ended September and is starting October with a firm bias, with the DXY reaching 28-month highs of 99.50 this morning. A soft EURUSD contributed most to overall USD strength, reaching as low as 1.0885 on the back of cool German CPI. Softer U.S. Chicago PMI and Dallas Fed index did see some USD position squaring however. Elsewhere, USDJPY traded over 108.15 on better risk taking levels, while GBPUSD dipped below 1.23.

Currently AUDUSD is almost unchanged at 0.67477 in the aftermath of the RBA cutting interest rates 25bps to 0.75%. Despite the policy makers communicating that they are willing to ease interest rates futher, the AUD has not softened as this activity was largely priced in.

Global equity indices closed higher for the most part overnight, with only the FTSE 100 down a quarter of one percent. The S&P500 posted a 0.36% gain, while the Nasdaq rose by 0.75%. In Europe, the Eurostoxx closed 0.66% higher while DAX appreciated by 0.38%. Japanese equities are higher this morning, despite a decline in the Tankan index. As we go to print, the Nikkei has risen 0.77%, in contrast to the Shangahi Composite Index with is 0.92% lower.

Regional equity indices closed largely lower yesterday, although DFMGI was broadly unchanged and Tadawul ASI was up nearly 0.5%.

Oil prices increased slightly overnight ahead of the resumption of US-China trade talks next week, and following the worst quarter so far this year. The news that Saudi Aramco has largely restored output following the attacks in September is likely to limit further upside however, along with concerns about global growth.