- There was little substantive change in policy from the FOMC meeting yesterday, but the use of the word ‘substantial’, in terms of the form of the recovery needed before asset purchases would be eased, led observers to believe that the USD 120bn/month asset purchase programme would extend for longer than previously anticipated. Chair Jerome Powell warned that the next several months would be challenging for the economy, but that the outlook for the second half of 2021 was markedly brighter. Policymakers indicated that the Fed funds rate would stay at its current near-zero levels through into 2023.

- The PMI surveys for the UK showed mixed fortunes between the services and the manufacturing sectors, illustrating the differing impacts of the pandemic crisis on the two parts of the economy. The services survey missed expectations of 50.7, and came in at a contractionary (just) 49.9 for the month. Meanwhile, manufacturing exceeded projections of 56.0 to hit 57.3. However, much of these extra gains were driven by the stockpiling that has been taking place ahead of the end of the UK’s Brexit transition period. Job shedding slowed, but the composite employment indicator was still far below the neutral 50 level at 46.5.

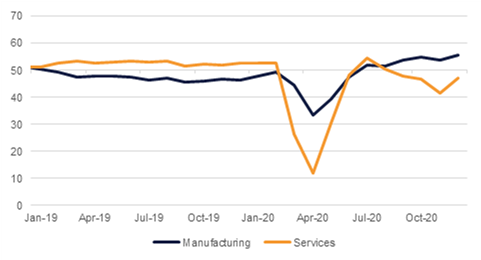

- These mixed fortunes were similarly highlighted by the composite Eurozone PMI surveys, with manufacturing at 55.5 and services at 47.3. It is worth noting that the two of these results both exceeded consensus forecasts, and were stronger than the previous month. However, the final reading could see a downward revision given the later respondents will likely have seen the coming restrictions that have now been reimposed in Germany, Netherlands and France in particular.

- The governor of the Turkish central bank, Naci Agbal, has reaffirmed the body’s commitment to curbing inflation and raising reserves. In a presentation he highlighted that ‘Upside risks to inflation require the monetary policy stance to be tight and decisive in 2021’, and that ‘Monetary policy decisions will be taken by giving priority to price stability.’

This is our last Daily Outlook publication for 2020; we will resume in January 2021 and wish all our readers well over the festive season.

Services the laggard in the Eurozone PMI surveys

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

- The outcome of the December FOMC hardly rocked US Treasury markets although it confirmed that the Federal Reserve will be in the market for treasuries for longer than previously expected. The Fed will maintain its USD 120bn/month of asset purchase until the economy reached “substantial further progress” on employment and inflation but there was no indication what levels would need to be reached to change the current QE policy, either up or down.

- After an initial sell-off, USTs rallied toward the close of trading and the curve was barely changed with the 2yr at 0.115% and the 10yr closing at 0.9163%. The Fed also revised its economic forecasts to reflect the faster than expected recovery in the US economy: the Fed now expect the economy to shrink by 2.4% in 2020 (from 3.7% previously) and to grow by 4.2% next year.

- Today markets will be looking to the Bank of England for their latest policy decision despite the uncertainty on whether the UK will secure a Brexit deal and what shape the British economy will be in next year.

FX

- After an initial spike in line with yields following the FOMC announcement the dollar sold off sharply and ended the day lower. Gains are extending on the DXY index in early trade this morning with the index holding at 90.13.

- The Euro was the major winner on the day following better than expected PMI readings for November. The single currency closed up 0.4% at 1.22 and is tentatively pushing higher in early trade today. Sterling also managed to extend gains, moving above 1.35, a gain of 0.36%.

- Elsewhere the sell-off in the dollar remains widespread with both the AUD and NZD gaining while the CAD slipped.

Equities

- Risk-on tone in equity markets continued yesterday as optimism around US fiscal stimulus, Covid-19 vaccines and a Brexit trade deal continued to boost equities. The FTSE 100 closed 0.9% higher, with the optimism extending into Europe with the CAC (0.3%) and the DAX (1.5%) also gaining.

- In the US, the NASDAQ closed up 0.5% and the S&P 500 0.2%, but the Dow Jones ended the day -0.2% lower.

Commodities

- Brent futures closed above USD 51/b overnight, a gain of 0.6% and their highest level since March. WTI settled at USD 47.82/b a gain of 0.4% but is up to more than USD 48/b this morning.

- Data from the EIA was relatively constructive with total US crude inventories drawing by 3m bbl last week although performance across the rest of the barrel was more mixed. Production in the US fell, by 100k b/d last week, to 11m b/d while product supplied (a proxy for demand) was up by 800k b/d w/w.

Click here to Download Full article

Daniel Richards

Daniel Richards